This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

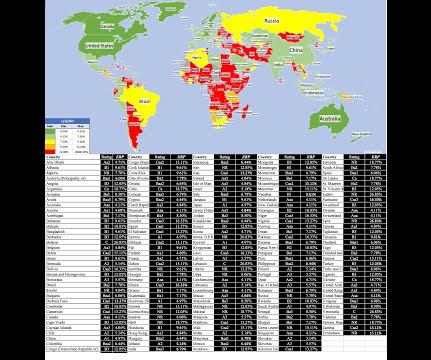

At the start of July, I updated my estimates of equity riskpremiums for countries, in an semiannual ritual that goes back almost three decades. If default risk seems like to provide too narrow a focus on countr risk, you can consider using country risk scores , which at least in principle, incorporate other components of country risk.

From 2008 until 2022, most central banks lowered interest rates to 1% or below, creating what economists call the Zero Interest Rate Policy (ZIRP). Strategy 2: Bridge to Better Times When down rounds seem inevitable but you believe the market correction is temporary, bridge financing can provide an alternative path.

Sovereign Defaults: A History Through time, governments have often been dependent on debt to finance themselves, some in the local currency and much in a foreign currency. Sovereign default can make banking systems more fragil e. Sovereign default also increases the likelihood of political chang e.

During his campaign, Argentine President Javier Milei promised to close the countrys central bank and adopt the dollar as the countrys currency. The main attraction of full dollarization is the elimination of the risk of a sudden, sharp devaluation of the countrys exchange rate, the IMF writers point out. from 2004-2007.

In corporate finance and investing, which are areas that I work in, I find myself doing double takes as I listen to politicians, market experts and economists making statements about company and market behavior that are fairy tales, and data is often my weapon for discerning the truth. Beta & Risk 1. Equity RiskPremiums 2.

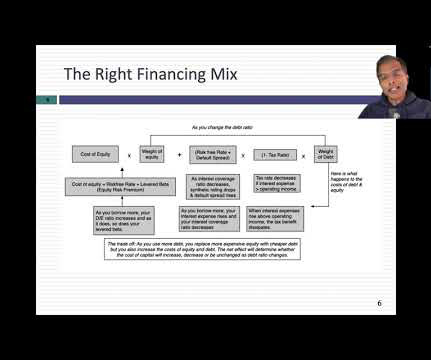

That is where the cost of capital, the Swiss Army Knife of finance that I wrote about in my sixth data update update , comes into play as a debt optimizing tool. Debt Design There was a time when businesses did not have much choice, when it came to borrowing, and had to take whatever limited choices that banks offered.

In the first five posts, I have looked at the macro numbers that drive global markets, from interest rates to riskpremiums, but it is not my preferred habitat. A few years ago, I wrote a paper for practitioners on the cost of capital , where I described the cost of capital as the Swiss Army knife of finance, because of its many uses.

Thus, my estimates of equity riskpremiums, updated every month, are not designed to make big statements about markets but more to get inputs I need to value companies. In the table below, I show my estimates of the implied equity riskpremium for the S&P 500 at the start of every month, since January 2024, and on March 14, 2025.

The first is that, as I noted in my post on country equity riskpremiums last week , there much of what I know or write about is pedestrian, and holding it in secret seems silly. Books : I have written eleven books and co-edited one, spread out across corporate finance, valuation and investing, and you can find them all listed here.

That said, when investors buy equities, it would be both irrational and illogical to settle for expected returns that are less than what you can earn on risk free or guaranteed investments, though behavioral finance suggests that both irrationality and illogic are persistent human traits.

In every introductory finance class, you begin with the notion of a risk-free investment, and the rate on that investment becomes the base on which you build, to get to expected returns on risky assets and investments. What is a risk free investment? Why does the risk-free rate matter?

Just as rising equity riskpremiums push up the cost of equity, rising default spreads push up the cost of debt of companies, with the added complication of higher default risk for those companies that had pushed to the limits of their borrowing capacity in a low interest-rate environment.

For central banks like the Federal Reserve, it helps control the economy. They set this rate to affect how much money moves through banks and influences short-term interest rates. We are going to focus on how discount rates are used in the context of investment, rather than in the context of central banks.

The cash flows from an entire business include inflows and outflows from investing, financing, and operating activities (such as sales, collections on receivables, expenditures, and settling accounts payable). For instance, assume a bank is performing a discounted cash flow analysis for a mortgage.

The idea is not new to encourage companies to increase their capitalization and reduce their bank debt (partly through more recourse to the capital market - CMU project). The rate would be calculated based on a 10-year "risk-free interest" rate depending on the currency, increased by a 1% riskpremium (1.5%

In my last three posts, I looked at the macro (equity riskpremiums, default spreads, risk free rates) and micro (company risk measures) that feed into the expected returns we demand on investments, and argued that these expected returns become hurdle rates for businesses, in the form of costs of equity and capital.

The first is that I do not have a macro focus, and my interests in macro variables occur only in the context of corporate finance or valuation issues. In the same dataset where I compute historical equity riskpremiums, I report historical returns on corporate bonds in two ratings classes (Moody’s Aaa and Baa ratings).

They give a vision of the company, which must be supplemented by other approaches to address the "true" price, which will result from the negotiation, i.e., the amount accepted by the assignor and financed by the buyer. . . Thus two companies with the same level of results but different future performance risks will have different values.

Kevin holds an MBA in finance from Georgia State University and a Bachelors in Chemical Engineering from the Georgia Institute of Technology. Finance Professor | Pepperdine Graziadio Business School Craig R. Everett is a finance professor at the Pepperdine Graziadio Business School. a Software as a Service company.

In my last post , I described the wild ride that the price of risk took in 2020, with equity riskpremiums and default spreads initially sky rocketing, as the virus led to global economic shutdowns, and then just as abruptly dropping back to pre-crisis levels over the course of the year. against developed market currencies.

In computing this implied equity riskpremium for the S&P 500, I start with the dividends and buybacks on the stocks in the index in the most recent year (which is known) and assume that they grow at the rate that analysts who follow the index are projecting for the next five years.

And Consequences If you are wondering why you should care about risk capital's ebbs and flows, it is because you will feel its effects in almost everything you do in investing and business. The 2008 banking and market crisis caused a drop of almost 50% in 2009, and it took the market almost five years to return to pre-crisis levels.

Note that this framework applies for all businesses, from the smallest, privately owned businesses, where debt takes the form of bank loans and even credit card borrowing and equity is owner savings, the largest publicly traded companies, where debt can be in the form of corporate bonds and equity is shares held by public market investors.

After the 2008 market crisis, I resolved that I would be far more organized in my assessments and updating of equity riskpremiums, in the United States and abroad, as I looked at the damage that can be inflicted on intrinsic value by significant shifts in riskpremiums, i.e., my definition of a crisis.

There are strands of research in both behavioral finance and empirical studies that back up contrarian strategies, but as with everything to do with investing, it comes with caveats and constraints. Contrarian Investing: The Psychological Tests! In the abstract, it is easy to understand the appeal of contrarian investing.

Healy before the Subcommittee on Banking and Currency on Wagner-Lea Act, S. Healy before the Subcommittee on Banking and Currency on Wagner-Lea Act, S. Investment companies have been compelled to financebanking clients of the insiders and companies in which they were personally interested. internal citations omitted). [4]

2] Startups typically lack significant historical financial data, often operate with negative profits initially, rely heavily on private equity or venture capital rather than traditional bank loans, and face a much higher risk of failure. [1] This premium rises when perceived market risk increases. [27] 2] [15] [17].

Venture Capital (VC) Financing: This is perhaps the most common context. 3] , [7] , [6] It sets a benchmark against which future fundraising rounds will be measured and helps investors assess whether the potential upside justifies the significant risks associated with early-stage ventures. [8]

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content