This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

30, 2019, healthcare real estate investment trusts (REITs) have earned a trailing ten-year return of 11.6% S&P Global reported that healthcare REITs have a five-year average dividend yield of 5.2%, while office REITs hold an average dividend yield of 2.9%. From data gathered on Sept. on average.

Historical Data: 1930-2019 To see how this framework works in practice, let's start by looking at the performance of US stocks, across the decades, and look at the returns on stocks, broadly categorized based on market capitalization and price to book ratios.

Rather it is based on investors’ critical thinking, due diligence, and using methods that combine value and growth strategies such as Peter Lynch’s PEG and dividend adjusted-PEG ratios. and outperformed the S&P 500 except for two years (Chen, 2019). Lynch developed the dividend-adjusted PEG ratio for this reason. References.

I have also developed a practice in the last decade of spending much of January exploring what the data tells us, and does not tell us, about the investing, financing and dividend choices that companies made during the most recent year. Dividends and Potential Dividends (FCFE) 1. Dividend yield & payout 3. Buybacks 2.

And my performance stats are as follows: 2019: +36%. As an example of this last problem, consider two “value” funds: the Vanguard International High Dividend Yield Index Fund and the International Value Fund. So, my new approach will be: Move most of my equity holdings to dividend funds. Silver: 3% [Unchanged]. 2020: +38%.

The first is the dividends you receive, while you hold stocks, a cash flow stream that provides a measure of stability to investors who seek it. trillion on their market capitalization at the end of 2019. Actual Returns Your returns on equities come in one of two forms. During the course of 2022, US equities collectively lost $11.6

In basic terms, you value a company with two variables, (1) cash flow to the owner (dividends to the investor), and (2) a required rate of return based on the risk of that investment. The last 6 months were equal or better than the average sales for 2019. Our response is not so simple, but let me try to explain: Steve Mize, ASA.

Share repurchases and dividends. The dividend yield could return to 5% in 2022. Strong operating cash flow allows the company to pay out dividends which are in line with its pre-pandemic policy. We expect that the dividend yield over the near-term to range between 5-6% like in 2019 and 2020. Advancing ESG issues.

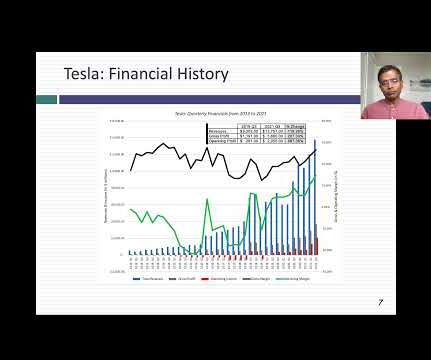

My two most recent valuations were in June 2019 and January 2020, and I am going to go back to them, not just because they are recent, but because they led to investment decisions on my part. In June 2019, Tesla had hit a rough spot, partly due to concerns about production bottlenecks and debt, and partly due to self inflicted wounds.

Strong years ahead lead to attractive dividend yields. Strong years ahead lead to attractive dividend yields. In 2019, Equinor introduced its share buyback program. I also expect a strong increase in dividends over next 3 years. The dividend yield could grow to a remarkable 4%+ in 23E. Conclusions.

broadband subscribers, which is an 85% increase compared to 2019. In 3Q21, it recorded 51m users, up 10x compared to 2019. In 2019 and 2020, Globe recognized more than PHP4bn equity loss from its investment in Mynt. Dividend payout is high which means it could continue to deliver a solid dividend yield of 3%+.

The company focus on a constant payout ratio of 30% for dividends. Enhanced profit prospects could lead to a juicy dividend yield of 3.3% LT-debt has tripled between 2019 and 2021. Attractive dividend yield adds additional return. Recovery of ROIC is one of the management’s top priority. It aims to get back to 8.5%

– Net Proceeds are expected to be used for general corporate purposes including, but not limited to, additional debt repayment and dividend payments –. EBITDA multiple on 2019 results and a $455K per key valuation –. Price implies a blended 2.9% cap rate and 27.0x PHILADELPHIA, Sept.

This is a Valuation Master Class student essay by Teeradon Piyakiattisuk from March 19, 2019. In the case of cost method, dividends are recorded separately as income in the profit and loss, whereas in the case of the equity method, dividends lower the investment value as dividends reduce the investee company’s equity.

and Swiss governments agree on types of retirement plans exempt from withholding on dividends. Switzerland Tax Treaty, are eligible for an exemption from tax withholding on dividends that they receive, provided that all other requirements of the Treaty are satisfied. and Switzerland have announced the list of U.S. State and Local News.

Given its losses over the past years, it did not pay out any dividends since 2016. We assume that there will be no dividends at least for the next 3 years. CAPEX is likely to stay much lower than 2017 to 2019 level. No dividend policy requires return generation from price. Cash flow – Tata Motors. Ratios – Tata Motors.

Dividend payout is high which means it could continue to deliver a solid dividend yield of 4%+. Negative FCFF in 2019 likely to be an exemption. High ROE and dividend yield make it an attractive play. Operating cash flows are not sufficient to fund growth internally yet. Ratios – PLDT. Free cash flow – PLDT.

It’s a decision that paid big dividends. Thomson Reuters achieved SAP’s Partner of the Year Award in 2025, is a two-time winner of the SAP Pinnacle Award (2010, 2019) and was the winner of the 2020 SAP Ariba and SAP Fieldglass Apex Award.

Within equities , I started the year with many value-oriented, international, and high-dividend stocks. Cash now earns 4 – 5%, but that’s barely above the dividend yield on many stock indices. This result is disappointing because it ends my 4-year streak of matching or beating the market, and it’s all because of my bad decisions.

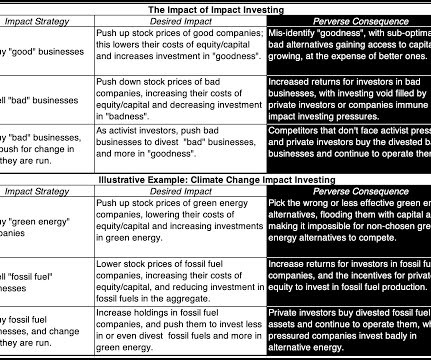

Even when you are successful in dissuading these companies from "bad" investments, but may not be able to stop them from returning the cash to shareholders as dividends and buybacks, rather than making "good" investments. Over the last decade, some of private equity’s biggest players have invested well over $1.1

Furthermore, the company increased dividends by 10% and announced that it will buy back GBP 2.3 (USD In 2019, the company announced that it plans to reduce its oil and gas output by 40% by 2030. Since publishing these figures, BP’s share price has risen by more than 15%. billion worth of shares.

This strong share price performance was further bolstered by an average gross annual dividend yield of roughly 6% over the past 10 years. This strong financial performance is also reflected in the stock market as TotalEnergies is currently trading at €57 per share, which is a year-on-year increase of roughly 30%.

This strong share price performance was further bolstered by an average gross annual dividend yield of roughly 6% over the past 10 years. This strong financial performance is also reflected in the stock market as TotalEnergies is currently trading at €57 per share, which is a year-on-year increase of roughly 30%.

2019) , for example, strong ESG performance correlates positively with higher equity returns and a reduction in downside risk. energy intensity classification) We first measure COE using an implied COE estimate that relies on residual income and dividend-discounting valuation models. Sussman (2019). Nuttall (2019).

trillion to buy back their shares, which is significantly more than these firms spent on dividend payments to their shareholders (Lazonick, Sakinç, and Hopkins, 2020). 2019) confirm this finding using more recent international data. Stock repurchases are popular. Between January 2009 and 2018, S&P 500 firms spent $4.3 Lazonick, W.,

Similarly, if a 10% US shareholder sells stock in a CFC, gain that would be treated as a dividend under Section 1248 of the Code may benefit from the 100% dividends received deduction. Comment: The pre-CAMT FSNOL carryover applies only to FSNOLs arising in taxable years ending after December 31, 2019. trade or business.

For one, stock dilution impairs the minority owner’s ability to influence company action by voting his shares, and it lessens the owner’s right to participate pari passu in the distributions or dividends of the company.

John was physically present in the United States for 120 days in each of the years 2019, 2020, and 2021. To determine if he meet s the substantial presence test for 2021, count the full 120 days of presence in 2021, 40 days in 2020 (1/3 of 120), and 20 days in 2019 (1/6 of 120). It is taxed at the same graduated rates as for a U.S.

Nonetheless, SWW increased its dividend by 3.8% shortly after the incident despite a recent warning to water utility companies from the UK’s water regulator, Ofwat, against paying significant dividends to investors while failing to address consumer safety and environmental concerns.

million ounces of Proven and Probable Reserves, which was discovered by Osino in 2019 and fast-tracked to the pre-construction stage within four years. 8 Financial capacity to fund development of Twin Hills and other growth initiatives from existing cash balances and future operating cash flows, while sustaining quarterly dividend.

compared to 1x in 2019. Future cash flow proceeds serve debt repayments; don’t expect any dividends in near term. Refinery companies face high working cap requirements and fluctuating inventories. The company heavily increased its leverage during the pandemic. Debt-to-equity ratio in 2020 stood at 2.9x Ratios – PBF Energy.

That would have left you lagging the 181% price appreciation that you would have earned on the S&P 500 during the period, and even more so, if you consider the fact that you would have earned no dividends on Facebook, while generating about a 2% dividend yield, every year on the index.

million shares for 14 cents per share in addition to interest and dividends. According to data published by Dealogic in Institutional Investor , “Deals involving public companies being taken private by private equity sponsors in 2019 were valued at $69.6 GE Credit Corporation purchased 2.3 billion, compared to $54.3

Earnings Estimates : The strength of the economy has been a big contributor to boosting actual and expected earnings on companies in the last two years, and these higher earnings have translated into more cash returned in dividends and buybacks.

The company and myself will work towards figuring out the most efficient method for repayment of the above, either through consultancy, and or dividend payments. If the company feels It does not need the second $50,000, the company has the right to do so and my equity will be diluted accordingly.

This was primarily based on revenue growth, which registered a heady 30% rise, allowing the bank to distribute its highest full-year dividend since 2008. Still, shareholders had reason to smile: In August, it announced an AU$1 billion share buyback and paid a final dividend of AU$2.40 billion after-tax profit versus $8.3

The second is art , ranging from paintings from the masters to digital art (non-fungible tokens or NFTs), that presumably offers owners not just financial returns but emotional dividends. With hedge funds, the fading of excess returns over time has been chronicled. in the 1990s to 0.87 in the last decade.

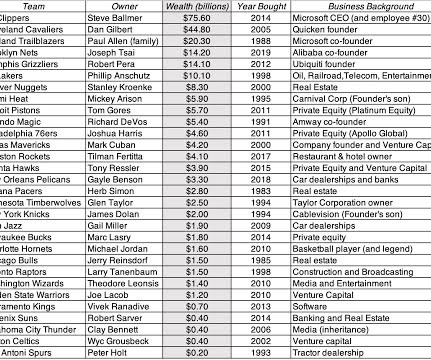

Brooklyn Nets NBA 2019 $2.40 That appeal may be only to a subset of individuals, but these buyers want to own the asset more for the emotional dividends, not the cashflows. Chelsea Premier League 2022 $5.30 Denver Broncos NFL 2022 $4.70 Phoenix Suns NBA 2023 $4.00 Milwaukee Bucks NBA 2023 $3.50 New York Mets MLB 2020 $2.40

In 2021, companies recovered entirely from the damage done in 2021, at least in the aggregate, with earnings in 2021 higher than 2019 earnings, by almost 33%. Not surprisingly, then, the net effect of growth will depend on how much is reinvested back, relative to what the company can harvest as future growth.

private and publicly listed firms (over 68,000 firm-year observations; 4,775 private and 5,040 public firms) from 1995 to 2019 using data from the Capital IQ database. Empirical Evidence To test the above three theories, we construct a comprehensive sample of U.S. Using a parametric approach following prior literature (e.g., Biddle et al.,

Foundational cases involved company information like its determination to cut its dividend [27] and information about a company’s major mineral discovery. [28] 451 (2019), and January 2021 legislation concerning SEC disgorgement that is now codified at Section 21(d)(3)(A)(ii) of the Securities Exchange Act, 15 U.S.C.A. ENDNOTES. [1]

Until TikTok recently supplanted it at the top, Facebook had the most intense user base of any social media platform, with users staying on the platform roughly an hour a day in 2019. Amazon has also invested tens of billions in its other businesses, with its biggest payoff coming in the cloud business (notice a pattern here).

For instance, I have always computed the present value of lease commitments in future years and treated that value as debt, a practice that IFRS and GAAP have adopted in 2019, but that computation requires explicit disclosures of lease commitments in future years.

A nice benefit of going to T+1 is in the area of corporate actions, in that ex-dividend dates and record dates now are aligned on the same day. Family Finances from 2019 to 2022” (October 2023), Page 19, available at [link]. [2] Gilt markets settle in one day. [15] similar benefits. 12, 2001), Pages 9-10, available at [link]. [4]

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content