This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

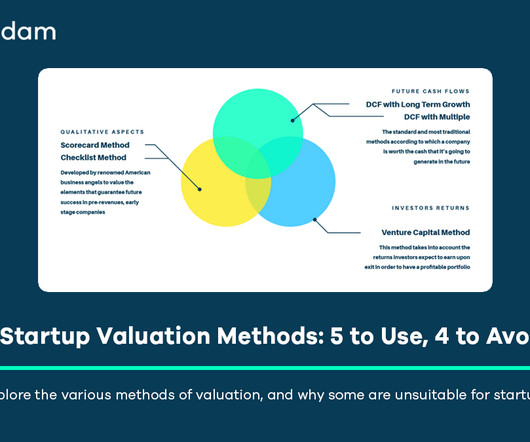

Critiquing Unsuitable Methods for High-Growth Startups Several traditional or overly simplistic methods fail to adequately capture the unique characteristics of technology startups. butcher, barber) where assets are tangible and customer acquisition straightforward, it breaks down for technology startups.

So let's get started and discover the keys to accurate valuation! By identifying earnings manipulation and guaranteeing more accurate firm values, this clever little technology is here to save the day. It's like a financial health check-up, examining everything from sales patterns to asset quality.

I pointed to the flaw in the logic, but the comments thereafter suggested such deep confusion about what returns on equity or capital measure, and what comprises an efficient market, that I think it does make sense to go back to basics and see if some of the confusion can be cleared up.

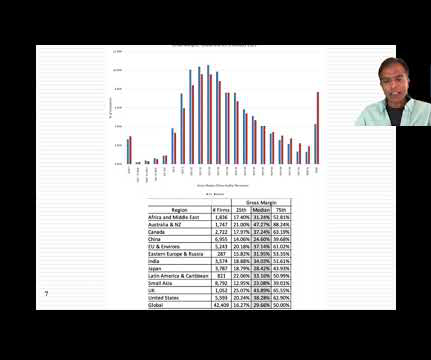

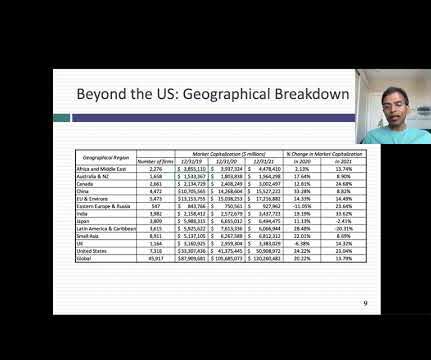

It is the end of the first full week in 2025, and my data update for the year is now up and running, and I plan to use this post to describe my data sample, my processes for computing industry statistics and the links to finding them. In the table below, we compare the changes in regional market capitalizations (in $ millions) over time.

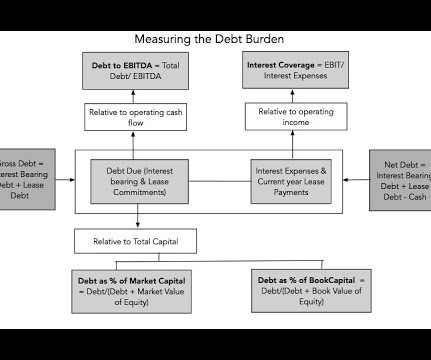

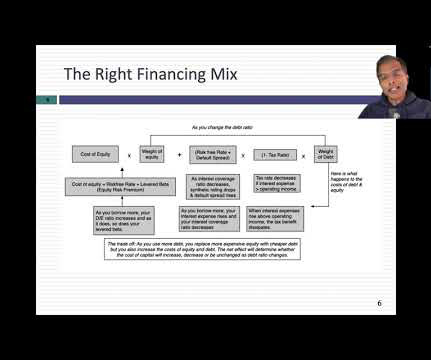

When the debt is within reasonable bounds (scaling up with the company), a company can borrow money, and not lower its ratings. Even if bond ratings drop, a business may be worth more, at that lower rating, if the tax benefits from the debt offset the higher default risk.

In the first five posts, I have looked at the macro numbers that drive global markets, from interest rates to riskpremiums, but it is not my preferred habitat. The second set of inputs are prices of risk, in both the equity and debt markets, with the former measured by equity riskpremiums , and the latter by default spreads.

I will start with a couple of confessions. Thus, my estimates of equity riskpremiums, updated every month, are not designed to make big statements about markets but more to get inputs I need to value companies.

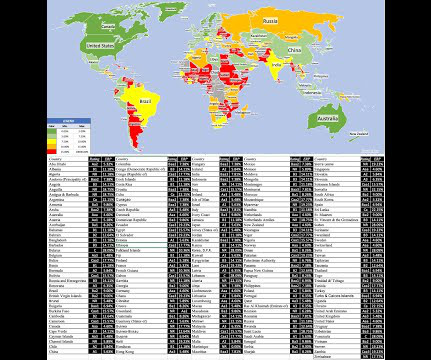

Note that while Canada and Mexico were not on the Wednesday list of tariff targets that was released on Wednesday, they have been targeted separately, and that the remaining countries that do not show up on this map (Russia and North Korea, for instance) are under sanctions that prevent them from trading in the first place.

Investors all talk about risk, but there seems to be little consensus on what it is, how it should be measured, and how it plays out in the short and long term. In closing, I will talk about some of the more dangerous delusions that undercut good risk taking. What is risk?

We started the year with significant uncertainty about whether the surge in inflation seen in 2022 would persist as well as about whether the economy was headed into a recession. The NASDAQ also gave back gains in the third quarter, but is up 27.27% for the year, but those gaudy numbers obscure a sobering reality.

At the start of the year, the consensus of market experts was that this would be a difficult year for markets, given the macro worries about inflation and an impending recession, and adding in the fear of the Fed raising rates to this mix made bullishness a rare commodity on Wall Street.

While stocks had their ups and downs during the year, they ended the year strong, and recouped, at least in the aggregate, most of the losses from 2022. Stocks ended the year well, with November and December both delivering strong up movements, and while this left investors feeling good about the year, it was a rocky year.

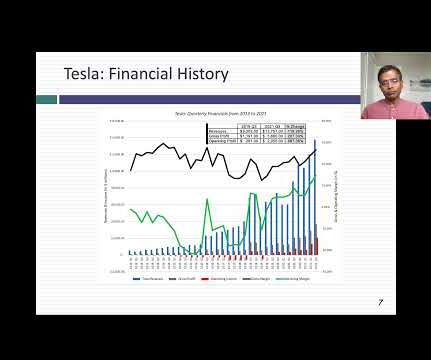

Thus, almost everything I know and practice, when valuing young and start-up companies, I learned in the process of valuing Amazon in the 1990s. Just as impressively, the company finally started delivering on its promise of profitability, going from barely making money in 2019 to an operating margin of 16.57% in 2022.

In my last post, I talked about the ritual that I go through every year ahead of my teaching each spring, and in this one, I will start on the first of a series of posts that I make at the start of each year, where I look at data, both macro and company-level. That is not true!

I would be lying if I said that I have had clarity about Tesla's story over the last decade, because it has so many tangents, distractions and shifts along the way, flirting with narratives about being a battery company, an energy company and a technology company.

In my last three posts, I looked at the macro (equity riskpremiums, default spreads, risk free rates) and micro (company risk measures) that feed into the expected returns we demand on investments, and argued that these expected returns become hurdle rates for businesses, in the form of costs of equity and capital.

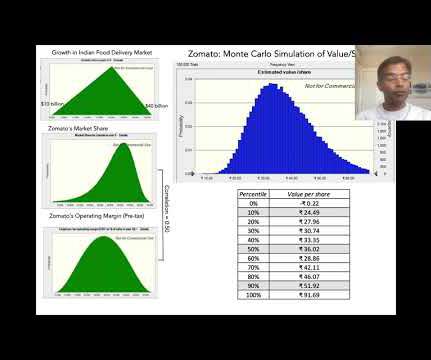

Zomato, an Indian online food-delivery company, was opened up to public market investors on July 14, 2021, and its market debut is being watched for clues by a number of other online ventures in India, waiting in the wings to go public. The Zomato IPO clocks in at 420 pages , much of it designed to bore readers into submission.

The second was that, starting mid-year in 2020, equity markets and the real economy moved in different directions, with the former rising on the expectations a post-virus future, and the latter languishing, as most of the world continued to operate with significant constraints.

To set the stage, I will start by laying out the differences measure of earnings that reported on an income statement: At the top of the profit ladder is gross income , the earnings left over after a company has covered the direct cost of producing whatever it sells.

Looking at US equities, the S&P 500 is up about 11% and the NASDAQ about 5%, from start of the year levels, and the underperformance of the latter has led to a wave of stories about whether this is start of the long awaited comeback of value stocks, after a decade of lagging growth stocks.

I also start thinking about my passion, which is teaching, the spring semester to come, and the classes that I will be teaching, repeating a process that I have gone through every year since 1984, my first year as a teacher. Face up to uncertainty, rather than avoid or deny it : Uncertainty is a feature of investing/ business, not a bug.

In my last post , I described the wild ride that the price of risk took in 2020, with equity riskpremiums and default spreads initially sky rocketing, as the virus led to global economic shutdowns, and then just as abruptly dropping back to pre-crisis levels over the course of the year.

Third, by making investing a choice between good (higher returns) and bad (higher risk), a message is sent, perhaps unwittingly, that risk is something to be avoided or hedged. micro uncertainties, into discount rates, and in the process, they end up incorporating risk that investors can eliminate, often at no cost.

In a post at the start of 2021 , I argued that while stocks entered the year at elevated levels, especially on historic metrics (such as PE ratios), they were priced to deliver reasonable returns, relative to very low risk free rates (with the treasury bond rate at 0.93% at the start of 2021). The year that was.

The Lead In To understand the market effects of the Russia-Ukraine conflict, we need to start with an assessment of the two countries, and their places in the global political, economic and market landscape, leading in. Ukraine, a part of the Soviet Union, has had its shares of ups and downs, and its economic footprint is even smaller.

To start the year, I returned to a ritual that I have practiced for thirty years, and that is to take a look at not just market changes over the last year, but also to get measures of the financial standing and practices of companies around the world. Happy New Year, and I hope that 2022 brings you good tidings! Sometimes, less is more!

That may reflect the concern that once a person or entity starts borrowing to fund its needs, it is easy to overuse debt, and risk its wellbeing in the process. An Optimizing Tool In my second and third data posts for this year, I chronicled the effects of rising interest rates and riskpremiums on costs of equity and capital.

for the year are at war with its concurrent promise to keep rates low; after all, adding those numbers up yields a intrinsic risk free rate of 8.7%. While I understand that much of the real growth in 2021 is a bounce back from 2020, even using a 2-3% real growth yields risk free rates that are much, much higher than today's numbers.

I started the month on a trip to Latin America, just as the tariff story hit my newsfeed and the market reacted with a sell off that knocked more than $9 trillion in market cap for global equities in the next two days. Equities: Storm Clouds gather (and dissipate)!

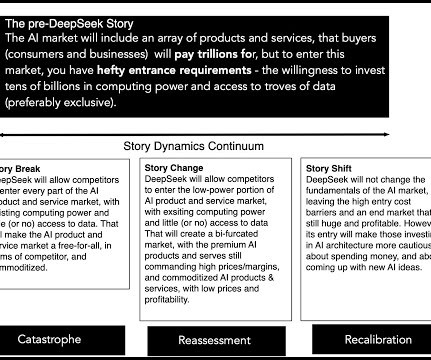

I am going to start this post with a confession that my knowledge of the architecture and mechanics of AI are pedestrian and that there will be things that I don't get right in this post. Along the way, the the AI story picked up supercomputing companies, as passengers, again on the belief that Ai systems would find a use for them.

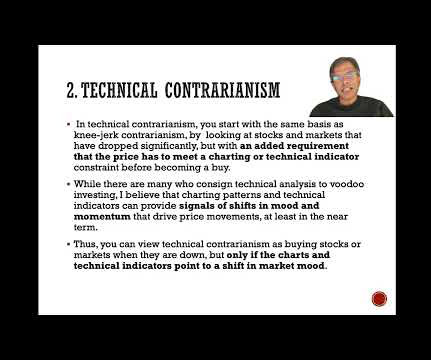

There are strands of research in both behavioral finance and empirical studies that back up contrarian strategies, but as with everything to do with investing, it comes with caveats and constraints. In the third, constrained contrarianism , you buy the stocks that are down, but only if they pass your screens for qualify and safety.

2] Startups typically lack significant historical financial data, often operate with negative profits initially, rely heavily on private equity or venture capital rather than traditional bank loans, and face a much higher risk of failure. [1] This de-risks the execution aspect of the future plan. 1] [4] [6] [14] [18]. 14] [18].

23] , [24] , [25] This average serves as a starting point, which is then adjusted upwards or downwards based on the specific startup’s relative strengths and weaknesses across several key criteria. [21] 23] Equidam uses country-specific risk-free rates (10-year government bonds) and market riskpremiums (sourced from Damodaran). [23]

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content