This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

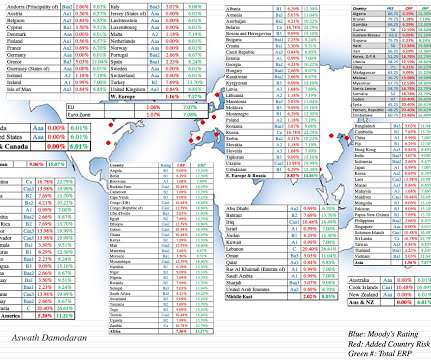

At the start of July, I updated my estimates of equity risk premiums for countries, in an semiannual ritual that goes back almost three decades. As with some of my other data updates, I have mixed feelings about publishing these numbers. On the second dimension, exposure to violence , the effects on business are manifold.

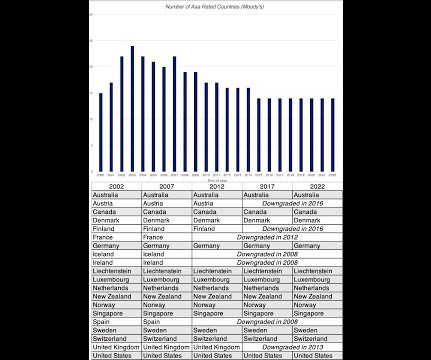

I was on a family vacation in August 2011 when I received an email from a journalist asking me what I thought about the S&P ratings downgrade for the US. Moodys has been rating corporate bonds since 1919 and startedrating government bonds in the 1920s, when that market was an active one.

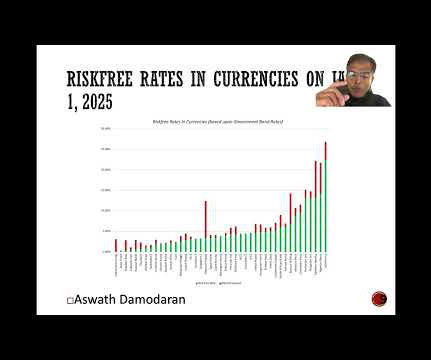

In fact, the standard practice that most analysts and investors follow to estimate the riskfreerate is to use the government bond rate, with the only variants being whether they use a short term or a long term rate. where I looked at the possibility that we live in a world where nothing is truly riskfree.

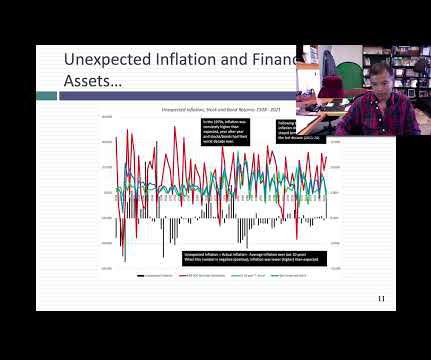

Inflation: Measurement and Determinants As the inflation debate was heating up in the middle of last year, I wrote a comprehensive post on how inflation is measured, what causes it and how it affects returns on different asset classes. Rather than repeat much of that post, let me summarize my key points.

The US treasury market, considered by some still as a safe haven, was anything but safe or a haven, especially at the long maturities, as long term rates soared, with inflation (not the Fed) being the key driver. That is good advice in most years, but 2022 was not one of those years.

We started the year with significant uncertainty about whether the surge in inflation seen in 2022 would persist as well as about whether the economy was headed into a recession. The NASDAQ also gave back gains in the third quarter, but is up 27.27% for the year, but those gaudy numbers obscure a sobering reality.

It has been my practice for the last two decades to take a detailed look at how risk varies across countries, once at the start of the year and once mid-year. Country Risk: Default Risk and Ratings For investors, the most direct measures of country risk come from measures of their capacity to default on their borrowings.

In most time periods, those recalibrations and resets tend to be small and in both directions, resulting in the ups and downs that pass for normal volatility. Clearly, we are not in one of those time periods, as markets approach bipolar territory, with big moves up and down.

The truth, though, is that the Fed sets only one interest rate, the Fed Funds rate, and that none of the rates that we face in our lives, either as consumers (on mortgages, credit cards or fixed deposits) or businesses (business loans and bonds), are set by or even indexed to the Fed Funds Rate.

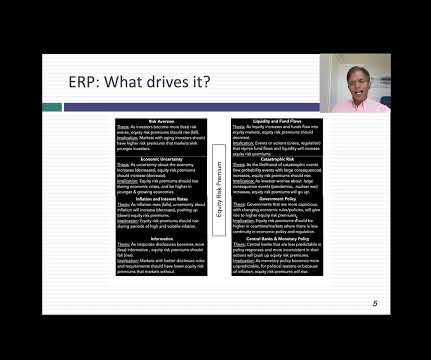

As part of that obsession, since September 2008, I have estimated an equity risk premium for the S&P 500 at the start of each month, and not only used that premium, when valuing companies during that month, but shared my estimate on my webpage and on social media.

I will follow up by looking at the mechanics that connect stock prices to inflation, and examine why the damage from higher inflation can vary across companies and sectors. The Year in Review At the start of 2022, the S&P 500 was at 4766.18, up from 3756.07 at the start of that year. Stocks: The What?

As we start 2024, the interest rate prognosticators who misread the bond markets so badly in 2023 are back to making their 2024 forecasts, and they show no evidence of having learned any lessons from the last year. The Fed Effect: Where's the beef?

In this post, I offer an alternative, albeit a more complicated, metric that I believe offers not only a more comprehensive measure of pricing, but also operates as a barometer of the ups and downs in the market. Note that nothing that I have said so far is premised on modern portfolio theory, or any academic view of risk premiums.

Looking at US equities, the S&P 500 is up about 11% and the NASDAQ about 5%, from start of the year levels, and the underperformance of the latter has led to a wave of stories about whether this is start of the long awaited comeback of value stocks, after a decade of lagging growth stocks.

As I have argued in all four of my posts, so far, about 2022, it was year when we saw a return to normalcy on many fronts, as treasuryrates reverted back to pre-2008 levels, and risk capital discovered that risk has a downside.

As with equity research and hedge fund roles, there are two main options for breaking in: Complete the CFA , get fixed income-related internships, and start working directly in FI research, either at a bank or a buy-side firm. Treasury yield at? Rates: Is the “risk-freerate” truly risk-free ?

In a post at the start of 2021 , I argued that while stocks entered the year at elevated levels, especially on historic metrics (such as PE ratios), they were priced to deliver reasonable returns, relative to very low riskfreerates (with the treasury bond rate at 0.93% at the start of 2021).

The first has been the steep rise in treasuryrates in the last twelve weeks, as investors reassess expected economic growth over the rest of the year and worry about inflation. Coming in 2020, the ten-year T.Bond rate at 1.92% was already close to historic lows. In particular, the Fed's own assessments of real growth of 6.5%

To start the year, I returned to a ritual that I have practiced for thirty years, and that is to take a look at not just market changes over the last year, but also to get measures of the financial standing and practices of companies around the world. Happy New Year, and I hope that 2022 brings you good tidings! Sometimes, less is more!

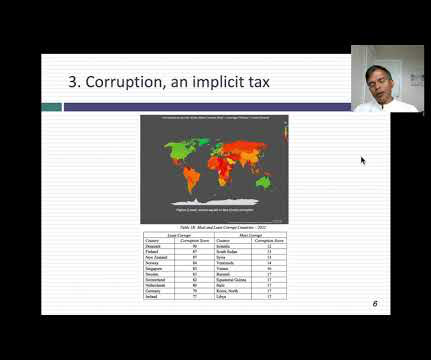

Since country risk is multidimensional and dynamic, my annual country risk update runs to more than a hundred (boring) pages , but I will try to summarize what the last year has brought in this post. Drivers of Country Risk What makes some countries riskier than others to operate a business in?

In my last post , I noted that the US has extended its dominance of global equities in recent years, increasing its share of market capitalization from 42% in at the start of 2023 to 44% at the start of 2024 to 49% at the start of 2025.

It was an interesting year for interest rates in the United States, one in which we got more evidence on the limited power that central banks have to alter the trajectory of market interest rates. We started 2024 with the consensus wisdom that rates would drop during the year, driven by expectations of rate cuts from the Fed.

23] , [24] , [25] This average serves as a starting point, which is then adjusted upwards or downwards based on the specific startup’s relative strengths and weaknesses across several key criteria. [21] 23] Equidam uses country-specific risk-freerates (10-year government bonds) and market risk premiums (sourced from Damodaran). [23]

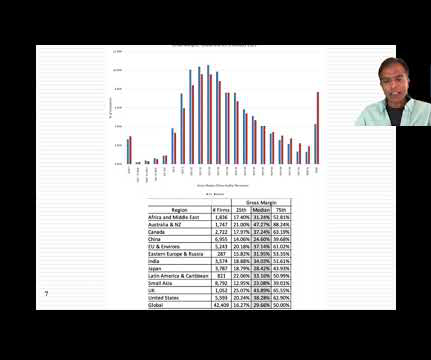

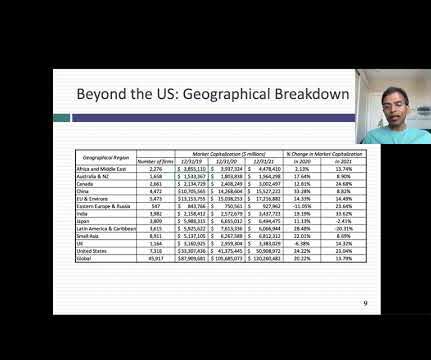

The results, broken down broadly by geography are in the table below: As you can see, the aggregate market cap globally was up 12.17%, but much of that was the result of a strong US equity market. I am no expert on exchange rates, but learning to deal with different currencies in valuation is a prerequisite to valuing companies.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content