This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Definition of Risk-FreeRate. The risk-freerate is the minimum rate of return on an investment with theoretically no risk. Government bonds are considered risk-free because technically, a government can always print money to pay its bondholders. Anticipated rate of inflation.

Looking ahead to 2023, with risk-freerates and credit spreads still elevated and the credit, deal making, regulatory and geopolitical environments uncertain, corporate borrowers and sponsors will need to plan rigorously to succeed on levered acquisitions and spin-offs and important refinancings. over the same period.

In every introductory finance class, you begin with the notion of a risk-free investment, and the rate on that investment becomes the base on which you build, to get to expected returns on risky assets and investments. What is a riskfree investment? Why does the risk-freerate matter?

In principle, the riskfree rate is what you will earn on a guaranteed investment in a currency, and any risk premiums, either for investing in equity (equity risk premium) or in fixed income securities (default spreads), are added to the riskfree rate.

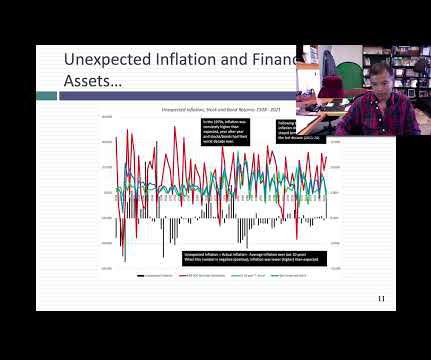

Not only has the intrinsic riskfreerate moved in sync with the ten-year bond rate for most of the last seven decades, but you can also see that the main reason why rates have been low for the last decade is not the Fed, with all of its quantitative easing machinations, but a combination of low growth and low inflation.

Risk-freerate: The risk-freerate is the government bonds yield; therefore, it is strongly influenced by the inflation rate. Additional factors that influence the risk-freerate are macroeconomic factors, monetary policies, external and structural factors. Dividends .

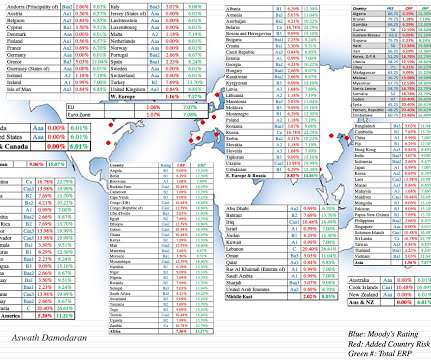

Country Risk: Currency and Cost of Capital As a final part to this post, to see the shifts in country risk that we have seen in 2022, let’s start with an assessment of riskfreerates.

It helps an investor understand what to expect to earn in relation to the risk-freerate and the market return. CAPM assumes that the minimum a rational investor would earn is the risk-freerate by buying the risk-free asset. How Do You Calculate the Capital Asset Pricing Model? E(r) = Rf + ??(Rm

The RiskFreeRate – Part 1 of 5 One of the most important inputs surrounding the valuation of the business is the discount rate that is used in the analysis. This discount rate is the expected rate of return on the subject interest which in most cases is the equity in the value of […].

Weve enhanced the standalone Cost of Capital step with updated chartsnow including visuals for the Cost of Equity premium, Spread over Risk-FreeRate, and Debt/Equity ratio, among others. Youll also find new options for setting the Risk-FreeRate, Spread over Risk-FreeRate, and Tax Rate.

She was also a contributing author to the chapter "Risk-FreeRate" in the fifth edition. She has authored a chapter titled, "Cost of Capital for Divisions and Reporting Units," which is included in the fourth and fifth editions of the textbook: Cost of Capital: Applications and Examples, by Shannon Pratt and Roger Grabowski.

In other words, the cost of equity is the rate of returns a firm pays to its shareholders. Risk-freerate . The systematic risk of the security (Beta). The growth rate of dividends . Where R(e) = expected return on investment, Rf = risk-freerate, Rm = expected return of the market, and ??

The expected return on an asset is determined by the risk-freerate of return with the addition of the asset’s beta to each macroeconomic factor that impacts the return on the asset multiplied by the risk premium of those factors. Inflation rate: ß = 0.6, The risk-freerate is 5%. 1 + RP1 + ??2+

The risk-freerate is higher – because investors benefit from “delaying” their eventual purchase of the underlying shares when they earn higher interest elsewhere. The risk-freerate and time to maturity also affect the Liability component (and other factors, such as the company’s credit quality, play a role).

The Codification often provides guidance on how to select a discount rate for a particular area of accounting. The Codification may require the use of a risk-freerate in some places and a risk-adjusted rate in others. Recent events have also impacted the components of the discount rate.

The discount rate effectively encapsulates the risk associated with an investment; riskier investments attract a higher discount rate. Different types of discount rates such as risk-freerate, cost of equity, or cost of debt, are used contextually in financial analysis.

If, on the other hand, investors are risk neutral, the price of risk will be zero, and investors will buy risky business, stocks and other investments, and settle for the riskfreerate as the expected return. It is only fair that I go first.

Monetary policy across major markets, including the pace and timing of interest rate cuts by major central banks will have a material impact on risk-freerates, a key input for valuations across multiple asset classes.

Going back to the start of this section, a company (say Ford) would require a higher cost of equity for a Nigerian project than for an equivalent German project (using a US $ riskfreerate of 1% and a beta of 1.1 Cost of equity in US $ for German project = 1% + 1.1

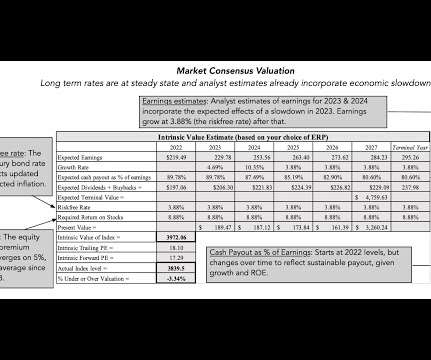

Thus, the equity risk premium of 4.84% on October 1, 2023, when added to the ten-year T.Bond rate of 4.58% on that day yields an expected return on equity of 9.42%, up from 8.81% on July 1, 2023. below the index value of 4288, confirming my base case conclusion.

The formula implies the return an investor expects from a risk-free investment plus the return from the stock in relation to market volatility. The market risk premium is calculated from a market rate of return less a risk-freerate. Suitability and limitation.

Returns in 2022 In my first classes in finance, as a student, I was taught that the US treasury rate was a riskfreerate, with the logic being that since the US treasury could always print money, it would not default.

That said, when investors buy equities, it would be both irrational and illogical to settle for expected returns that are less than what you can earn on riskfree or guaranteed investments, though behavioral finance suggests that both irrationality and illogic are persistent human traits. Stocks: The What Next?

Next, we need to estimate the risk-freerate and the risk premium for each risk factor. Let's say the risk-freerate is 3%, the risk premium for market risk is 5%, the risk premium for industry risk is 4%, and the risk premium for country risk is 2%.

We’ve added a ‘date picker’ across key resources sections, allowing you to examine risk-freerates, corporate tax rates, market risk premium, and country ratings across any historic date you select. Resources Section Date Improvement: What? Explore this feature in the Resources section.

In my last two posts, I noted that the prices of risk have drifted down in markets, with both equity risk premiums and default spreads decreasing through 2021.

In short, the expected return on a risky investment can be constructed as the sum of the returns you can expect on a guaranteed investment, i.e., a riskfree rate, and a risk premium, which will scale up as risk increases. The risk premium that you demand has different names in different markets.

Market Risk-FreeRate: Beta calculations often involve comparing the asset’s returns to a risk-freerate, such as the yield on a government bond with a similar maturity. Ensure that you have access to accurate and up-to-date data for the chosen benchmark index.

The WACC formula derives the current cost of each form of finance, starting with the risk-freerate, the expected return on equity, and the costs associated with debt financing. The required rate of return for equity (Re) is generally calculated using the Capital Asset Pricing Model (CAPM).

The WACC formula derives the current cost of each form of finance, starting with the risk-freerate, the expected return on equity, and the costs associated with debt financing. The required rate of return for equity (Re) is generally calculated using the Capital Asset Pricing Model (CAPM).

The WACC formula derives the current cost of each form of finance, starting with the risk-freerate, the expected return on equity, and the costs associated with debt financing. The required rate of return for equity (Re) is generally calculated using the Capital Asset Pricing Model (CAPM).

The Court concluded its opinion by walking through its several reasons for finding that the trial record in this case did not support the 29% increase in the perpetuity growth rate that the chancery court had made upon reargument. The Supreme Court Rejected the Cross-Appeal and Refused to Disregard the Comparable Companies Analysis.

Historically, Japan has a very low risk-freerate. However, my long-term outlook is a bit more optimistic. Idemitsu should be able to focus on its other segments to diversify away from oil. World Class Benchmarking Scorecard – Idemitsu Kosan. Identifies a company’s competitive position relative to global peers.

According to the CAPM model - the return required by the shareholders can be described using the following equation: Cost of Equity = Risk-FreeRate + Beta x Risk Premium. It is customary to calculate the weighted average capital price using a financial model formula known as the CAPM (Capital Asset Pricing Model). .

Russia has a massively high risk-freerate of 10%. FCFF likely to remain volatile given abrupt changes in working capital. Value estimate – Gazprom. My revenue and margin forecast is roughly in line with analyst’s consensus. World Class Benchmarking Scorecard – Gazprom.

The answer is recognizing that market-set rates ultimately are composed of two elements: an expected inflation rate and an expected real interest rate , reflecting real economic growth.

Discount Rate (Cost of Equity): The rate used to discount future cash flows reflects the riskiness of the investment. This incorporates the risk-freerate, a market risk premium specific to the company’s country, and Beta ($beta$). Beta measures the volatility of the company relative to the market.

Note also that during 2022 and 2023, the movements in these government bond rates mimic the US treasuries, rising strongly in 2022 and declining or staying stable in 2023.

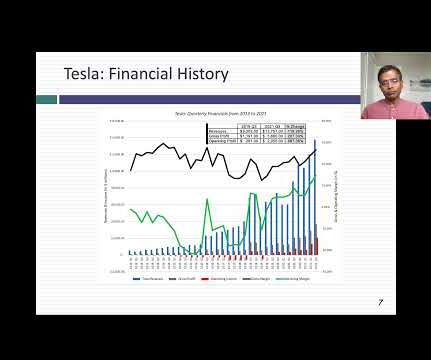

Risk : When I valued Tesla last in early 2020, I used a cost of capital of 7%, reflecting a riskfreerate of 1.75% and an equity risk premium of 5.2% for mature markets.

This is a large dataset and can take a while to download) Data Timing & Currency Effects In computing the statistics for each of the variables, I have one overriding objective, which is to make sure that they reflect the most updated data that I have at the time that I compute them, which is usually the first week of January.

In the equity market, I capture the price of risk with a forward-looking estimate of expected returns on stocks, computed from the level of stock prices and expected future cash flows, and I graph both the expected return and the implied equity risk premium (from netting out the riskfreerate) in the graph below: Implied ERP spreadsheet In equity (..)

In my last three posts, I looked at the macro (equity risk premiums, default spreads, riskfreerates) and micro (company risk measures) that feed into the expected returns we demand on investments, and argued that these expected returns become hurdle rates for businesses, in the form of costs of equity and capital.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content