This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Thus, as you peruse my historical data on implied equityriskpremiums or PE ratios for the S&P 500 over time, you may be tempted to compute averages and use them in your investment strategies, or use my industry averages for debt ratios and pricing multiples as the target for every company in the peer group, but you should hold back.

The first was the response that I received to my last data update , where I looked at the profitability of businesses, and specifically at how a comparison of accounting returns on equity (capital) to costs of equity (capital) can yield a measure of excess returns.

Not surprisingly, the markets opened down on Thursday and spent the next two days in that mode, with US equity indices declining almost 10% by close of trading on Friday. US equities had the biggest decline in dollar value terms, losing $5.3 Other Markets As equity markets reacted to the tariff announcement, other markets followed.

In the first five posts, I have looked at the macro numbers that drive global markets, from interest rates to riskpremiums, but it is not my preferred habitat. In this role, the cost of capital is an opportunity cost, measuring returns you can earn on investments on equivalent risk.

Relative Risk Measures Before we embark on how to measure relative risk, where there can be substantial disagreement, let me start with a statement on which there should be agreement. Technology and cyclical companies dominate raw highest risk rankings.

In my second data update post from the start of this year , I looked at US equities in 2022, with the S&P 500 down almost 20% during the year and the NASDAQ, overweighted in technology, feeling even more pain, down about a third, during the year. US Equities in 2023: Into the Weeds! that was lost last year.

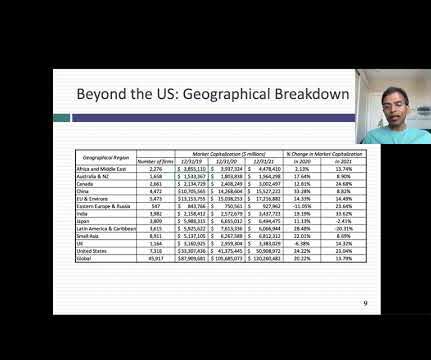

I looked at global equities, broken down by region of the world, and in US dollars, to allow for direct comparison: India is the only region of the world to post positive returns, in US dollar terms, in the third quarter, and is the best performing market of the year, running just ahead of the US; note again that of the $5.2

Heading into 2023, US equities looked like they were heading into a sea of troubles, with inflation out of control and a recession on the horizon. Breaking equities down by sub-region, and looking across the globe, I computed the change in aggregate market capitalization, by region: While US stocks accounted for about $9.5

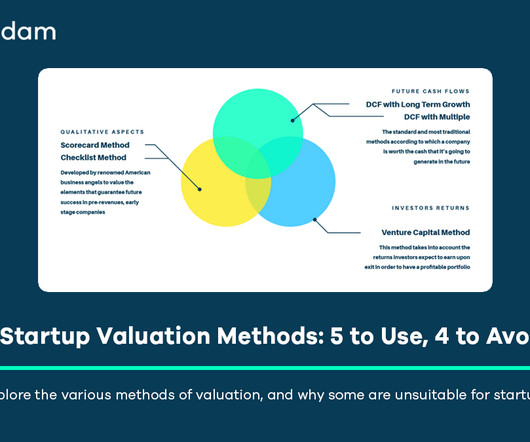

Critiquing Unsuitable Methods for High-Growth Startups Several traditional or overly simplistic methods fail to adequately capture the unique characteristics of technology startups. butcher, barber) where assets are tangible and customer acquisition straightforward, it breaks down for technology startups.

In my last three posts, I looked at the macro (equityriskpremiums, default spreads, risk free rates) and micro (company risk measures) that feed into the expected returns we demand on investments, and argued that these expected returns become hurdle rates for businesses, in the form of costs of equity and capital.

When valuing or analyzing a company, I find myself looking for and using macro data (riskpremiums, default spreads, tax rates) and industry-level data on profitability, risk and leverage. I do report on a few market-wide data items especially on riskpremiums for both equity and debt. Cost of Equity 1.

The second was that, starting mid-year in 2020, equity markets and the real economy moved in different directions, with the former rising on the expectations a post-virus future, and the latter languishing, as most of the world continued to operate with significant constraints.

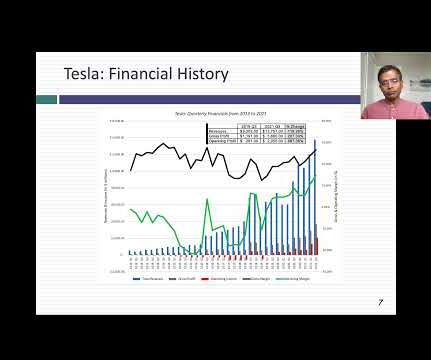

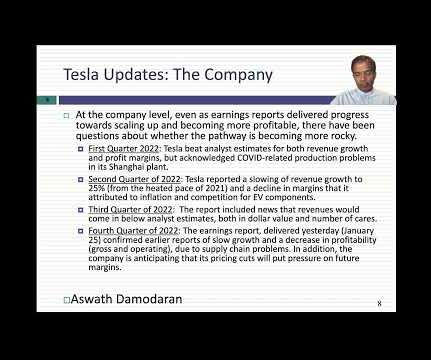

I would be lying if I said that I have had clarity about Tesla's story over the last decade, because it has so many tangents, distractions and shifts along the way, flirting with narratives about being a battery company, an energy company and a technology company. for mature markets. What’s your story?

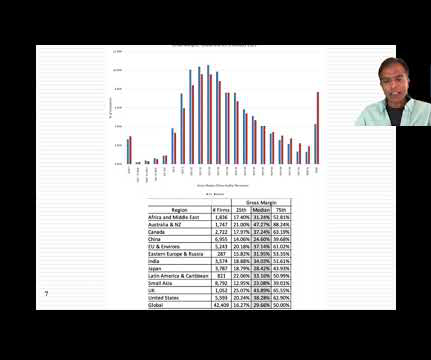

Some of that variation can be attributed to different mixes of businesses in different regions, since unit economics will result in higher gross margins for technology companies and commodity companies, in years when commodity prices are high, and lower gross margins for heavy manufacturing and retail businesses.

In its early years, Tesla was dependent on equity issuances for funding growth investments, and its liberal use of options to reward management (and especially Elon Musk) opened it up to criticism. The Market : The US equity market in January 2023 looks very different from the market at the start of 2022. per share in 2022.

Looking at US equities, the S&P 500 is up about 11% and the NASDAQ about 5%, from start of the year levels, and the underperformance of the latter has led to a wave of stories about whether this is start of the long awaited comeback of value stocks, after a decade of lagging growth stocks.

The various problems facing the company led the court to embrace the respondents’ theory that SWS would continue to face an uphill climb given its relatively small size, which prevented it from scaling its substantial regulatory, technological, and back-office costs. Hilltop’s Influence on the Sale Process Rendered Merger Price Unreliable.

Changes in tax regulations, technology advancements, and shifts in customer preferences can impact the future prospects and growth potential of the business. Technology and Infrastructure In today's digital age, the technology and infrastructure employed by a tax preparation business can greatly influence its value.

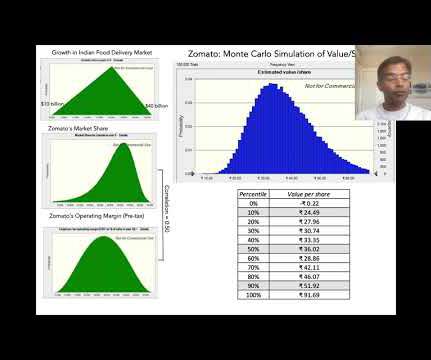

Uber's ownership in Zomato is a result of Zomato's acquisition of Uber Eats India, where Uber received a share of Zomato's equity in exchange. That said, reinvestment takes a different form for companies like Zomato, with investments in technology and in acquisitions, driving future growth.

Equipment, Technology, and Infrastructure The quality and condition of equipment, technology, and infrastructure directly influence the value of a disaster restoration business. Stay updated on the latest advancements, changes in regulations, and emerging technologies that can impact the business's value.

In my last post , I described the wild ride that the price of risk took in 2020, with equityriskpremiums and default spreads initially sky rocketing, as the virus led to global economic shutdowns, and then just as abruptly dropping back to pre-crisis levels over the course of the year.

The last decade, with it influx of user based companies and technology platforms forced me to think seriously about how to value a user, subscriber or rider and extrapolate from there to company value. Discount rates in intrinsic valaution have to change to reflect current market conditions, and can be expected to change over time.

Kevin holds an MBA in finance from Georgia State University and a Bachelors in Chemical Engineering from the Georgia Institute of Technology. Amanda holds a PhD, dual master’s degrees from Stanford University and dual bachelor’s degrees from the California Institute of Technology.

If equity markets surprised us with their resilience in 2020, not just weathering a pandemic for the ages, but prospering in its midst, US equity markets, in particular, managed to find light even in the darkest news stories, and continued their rise through 2021. The year that was.

In my last data updates for this year, I looked first at how equity markets rebounded in 2023 , driven by a stronger-than-expected economy and inflation coming down, and then at how interest rates mirrored this rebound.

In this section, I will begin by looking at the bond market effects and then move on to equities and other asset classes, starting by looking at the localized reaction (for Ukranian and Russian securities) and then the global ripple effects. As Russian equities have imploded, the ripple effects again are being felt across the globe.

The first quarter of 2021 has been, for the most part, a good time for equity markets, but there have been surprises. Those rates stayed low through the rest of 2020, even as equity markets recovered and corporate bond spreads fell back to pre-crisis levels. to close to zero, and the ten-year T.Bond rate declining to close to 0.70%.

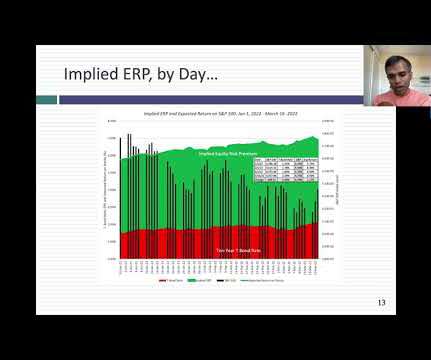

RiskPremiums : You cannot make informed financial decisions, without having measures of the price of risk in markets, and I report my estimates for these values for both debt and equity markets.

To fund the business, you can either use borrowed money (debt) or owner's funds (equity), and while both are sources of capital, they represent different claims on the business. Even government-owned businesses fall under its umbrella, with the key difference being that equity is provided by the taxpayers.

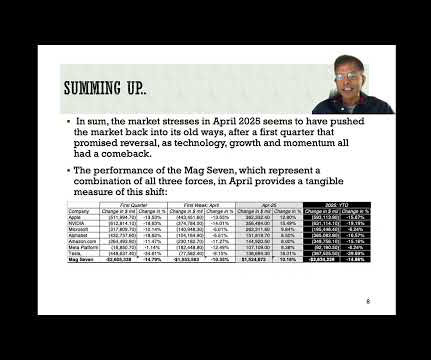

I started the month on a trip to Latin America, just as the tariff story hit my newsfeed and the market reacted with a sell off that knocked more than $9 trillion in market cap for global equities in the next two days. Equities: Storm Clouds gather (and dissipate)! trillion that they lost in the first week of the month.

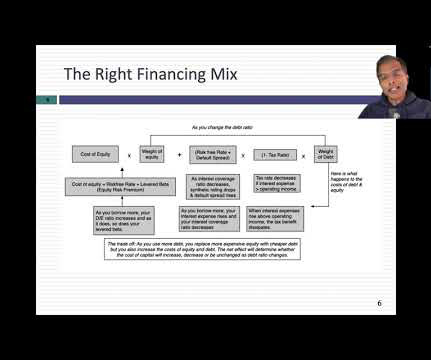

The Debt Trade off As a prelude to examining the debt and equity tradeoff, it is best to first nail down what distinguishes the two sources of capital. To me, the key distinction between debt and equity lies in the nature of the claims that its holders have on cash flows from the business.

For the market, it is often built on papers (or books) that look at the historical data on what equity markets have delivered as returns over long periods, relative to what you would have made investing elsewhere. Contrarian Investing: The Psychological Tests! In the abstract, it is easy to understand the appeal of contrarian investing.

Thus, my estimates of equityriskpremiums, updated every month, are not designed to make big statements about markets but more to get inputs I need to value companies. That said, to value companies today, I have no choice but to bring in the economics and politics of the world that these companies inhabit.

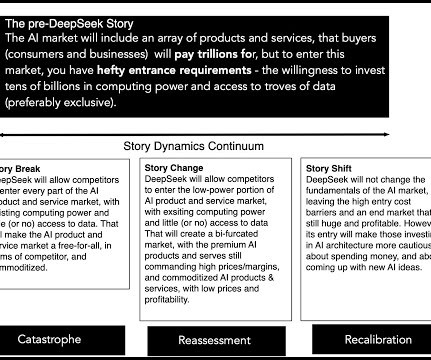

The AI story, before DeepSeek The AI story has been building for a while, reflecting the convergence of two forces in technology - more computing power, often in smaller and smaller packages, and the accumulation of data, on technology platforms and elsewhere. What is it that makes the DeepSeek story so compelling?

2] Startups typically lack significant historical financial data, often operate with negative profits initially, rely heavily on private equity or venture capital rather than traditional bank loans, and face a much higher risk of failure. [1] This de-risks the execution aspect of the future plan. 1] [4] [6] [14] [18].

It determines the price per share, dictating how much equity founders concede in exchange for the capital raised. [3] 3] , [7] , [6] It sets a benchmark against which future fundraising rounds will be measured and helps investors assess whether the potential upside justifies the significant risks associated with early-stage ventures. [8]

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content