The Dividend Discount Model (DDM): The Black Sheep of Valuation?

Brian DeChesare

MAY 3, 2023

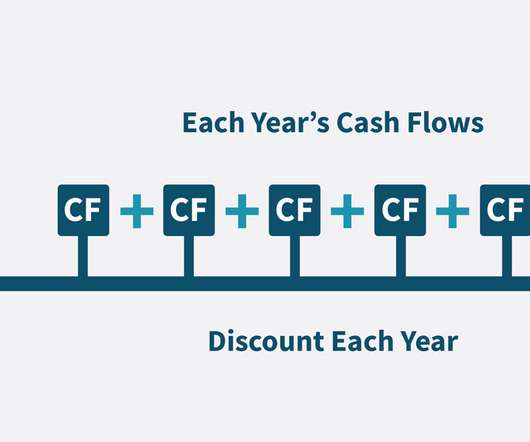

The DDM is more grounded because it’s based on the company’s actual distributions and potential future value. And it values the company today based on the present value of its dividends and that potential future value (either the stock price or the Equity Value via the Terminal Value calculation).

Let's personalize your content