This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

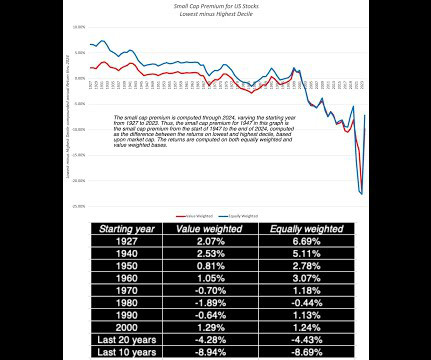

In my last post , I discussed how inflation's return has changed the calculus for investors, looking at how inflation affects returns on different asset classes, and tracing out the consequences for equity values, in the aggregate. The former is short hand for the small cap premium and the latter is the proxy for the value factor in returns.

This ratio offers insight into a companys profitability and relative value by comparing its total worth (Enterprise Value, encompassing debt and equity) to its operational earnings (EBITDA). EV typically includes MarketCapitalization, Debt, Minority Interest, and Preferred Equity, minus Cash & Cash Equivalents.

While this may seem perverse, the first step in understanding and assessing where we are in markets now is to go back and examine where things stood then. trillion in market value in the first six months in the year , but the severity of last year's decline has still left them $14.4 US Equities in 2023: Into the Weeds!

Corporate Bonds: No Shortage of Risk Capital In my last post, I chronicled the movement in the equity risk premium, i.e. the price of risk in the equitymarket, during 2021, but the bond market has its own, and more measurable, price of risk in the form of corporate default spreads.

This evaluation is pivotal because it dictates the terms of investment, directly influencing how much equity (ownership) a founder must relinquish in exchange for funding from the Sharks. Conversely, a lower valuation may require founders to give up more equity.

The second was that, starting mid-year in 2020, equitymarkets and the real economy moved in different directions, with the former rising on the expectations a post-virus future, and the latter languishing, as most of the world continued to operate with significant constraints.

Data universe : In my sample, I include all publicly traded firms with marketcapitalizations that exceed zero, traded anywhere in the world. I do report on a few market-wide data items especially on risk premiums for both equity and debt. Cost of Equity 1. Standard deviation in stock price 2.

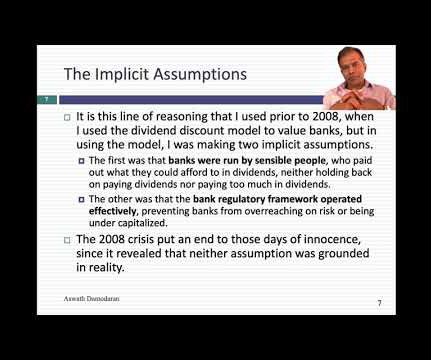

In this post, I will begin by looking at how to value banks and follow up with an examination of investor views of banking have changed, by looking at pricing, before examining divergences in how banks are priced in the market today. All Equity, All the time!

The Market Reaction As the rhetoric of war has heated up in the last few months, markets were wary about the possibility of war, but as Russian troops have advanced into the Ukraine, that wariness has turned to sell off across markets. As Russian equities have imploded, the ripple effects again are being felt across the globe.

The first quarter of 2021 has been, for the most part, a good time for equitymarkets, but there have been surprises. The arrival of the COVID in February 2020, and the ensuing market meltdown, causing treasury rates to plummet across the spectrum, with three-month T.bill rates dropping from 1.5%

In this post, I will begin with a historical assessment of stock returns in the recent past, then move on to evaluate the returns that investors can expect to make, given how they are priced at the start of 2022, and end with a do-it-yourself valuation of the index right now. The year that was.

In an earlier episode, Nike also lost billions in marketcapitalizations, when Michael Jordan, an NBA superstar whose name-branded footwear (Air Jordan) had become a game changer for Nike, unexpectedly announced in 1993 , that he would be retiring from basketball, to play baseball.

Given the historical roots of the biggest Indian family groups, the Adani Group has been a recent entrant, not making the top ten list (in terms of either operating metrics like revenues or market-based numbers like marketcapitalization or enterprise value) as recently as ten years ago, and barely making the top ten list five or six years ago.

For the market, it is often built on papers (or books) that look at the historical data on what equitymarkets have delivered as returns over long periods, relative to what you would have made investing elsewhere.

In my first two data posts for 2025, I looked at the strong year that US equities had in 2024, but a very good year for the overall market does not always translate into equivalent returns across segments of the market. trillion, almost of the entire market's gain for the year. The Value Premium?

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content