This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

At the start of July, I updated my estimates of equity risk premiums for countries, in an semiannual ritual that goes back almost three decades. To estimate the cost of equity for an investment in a risky country. As with some of my other data updates, I have mixed feelings about publishing these numbers.

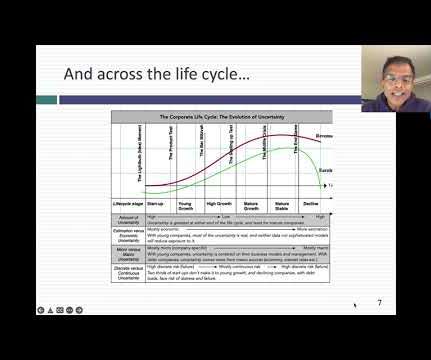

Valuation at this stage is vital for several reasons: it helps attract necessary investment, guides fair equity distribution among founders and early stakeholders, and serves as a benchmark for strategic planning and growth monitoring. Early indicators like user sign-ups, pilot programs, or letters of intent can exist even without sales.

These data tables should be accessible and downloadable (in excel), and if you find yourself stymied, when doing so, trying another browser often helps. The data is updated once a year, at the start of the year, and the 2025 data update will be available around January 10, 2025.

Your browser does not support playing this file but you can still download the MP3 file to play locally. on whatsapp (opens in a new window) Save Published July 24 2025 Jump to comments section Print this page Unlock the Editor’s Digest for free Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

So, we would like to allow anyone to download our red flags. Its going to change your equity, your retained earnings, your profits, your earnings per share, your EBIT, your EBITDAall these numbers would change. We use quarterly data, which we download from Compustat. And its incredibly difficult.

Thus, as you peruse my historical data on implied equity risk premiums or PE ratios for the S&P 500 over time, you may be tempted to compute averages and use them in your investment strategies, or use my industry averages for debt ratios and pricing multiples as the target for every company in the peer group, but you should hold back.

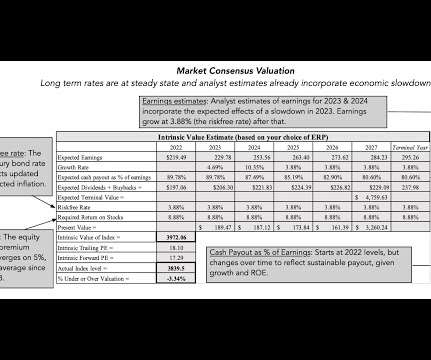

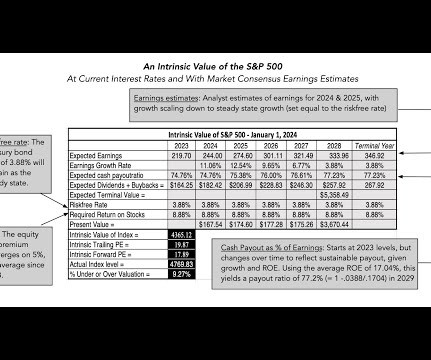

Thus, my estimates of equity risk premiums, updated every month, are not designed to make big statements about markets but more to get inputs I need to value companies. In the table below, I show my estimates of the implied equity risk premium for the S&P 500 at the start of every month, since January 2024, and on March 14, 2025.

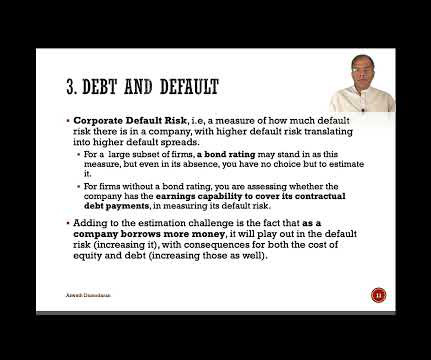

The Hurdle Rate - Intuition and Uses You don't need to complete a corporate finance or valuation class to encounter hurdle rates in practice, usually taking the form of costs of equity and capital, but taking a finance class both deepens the acquaintance and ruins it. Corporate Default Risk , i.e,

Your browser does not support playing this file but you can still download the MP3 file to play locally. On Tuesday, the American railroad giant Union Pacific announced its intention to buy Norfolk Southern, promising to fulfill Abraham Lincoln’s dream of a transcontinental railroad.

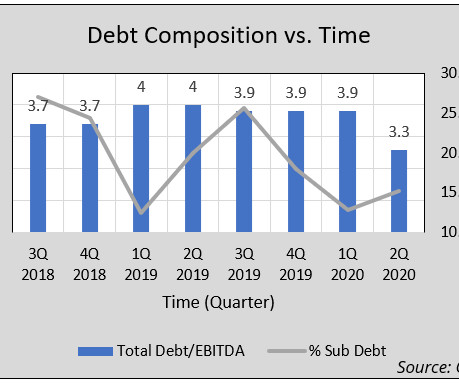

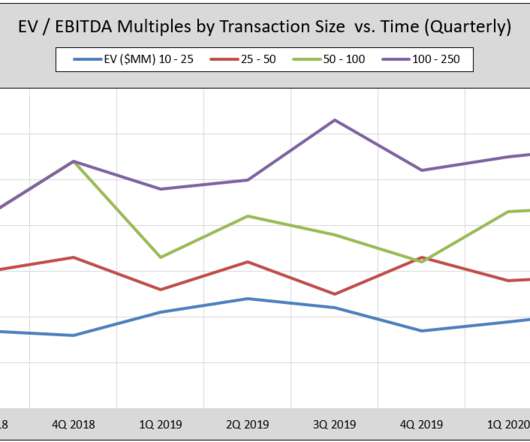

Click to Download: Middle Market Private Equity M&A Activity – Q2 2020 Executive Summary Transaction Volume Shrinks Only 31 transactions were reported in Q2 2020, bringing the total reported transactions in 2020 to 113. If you liked this blog you may enjoy reading some of our other blogs here.

Click to Download: Middle Market Private Equity M&A Activity – Q2 2020. The post Middle Market Private Equity M&A Activity – Q2 2020 appeared first on ValueScope. Executive Summary. Transaction Volume Shrinks. Size Premium. If you liked this blog you may enjoy reading some of our other blogs here.

In this post, I will begin by chronicling the damage done to equities during 2022, before putting the year in historical context, and then examine how developments during the year have affected expectations for the future. Actual Returns Your returns on equities come in one of two forms. Stocks: The What?

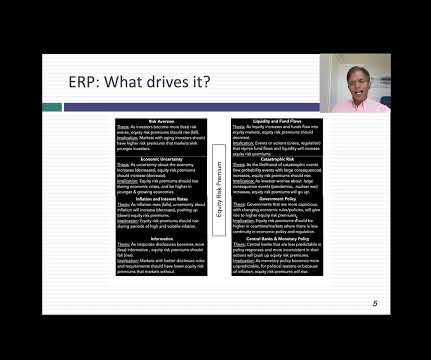

If you have been reading my posts, you know that I have an obsession with equity risk premiums, which I believe lie at the center of almost every substantive debate in markets and investing. How, you may ask, can equity risk premiums be that divergent, and does that imply that anything goes?

Our new Deal Lawyers Download podcast features my interview with Lippes Mathias’ John Koeppel about current trends in private equity deals. – How are private equity buyers approaching deal financing in the current market?

In the magazine: CFOs offer their advice on what you need to look out for in the new era of inflation; Private equity compensation survey findings; The future of ESG-linked loans; What CFOs can learn from chipmakers; Plus much more….

Previously, Erica was Chief Financial Officer of Carlyle’s Global Credit segment and before that she was responsible for the Fund Management Operations of Carlyle’s Europe based private equity funds, based in Luxembourg and London. Prior to this role Erica led the Real Assets Partnership Accounting team in Washington D.C.

Heading into 2023, US equities looked like they were heading into a sea of troubles, with inflation out of control and a recession on the horizon. Breaking equities down by sub-region, and looking across the globe, I computed the change in aggregate market capitalization, by region: While US stocks accounted for about $9.5

To gain perspective on how the Fed Funds rate has been changed over time, consider the following graph, where the effective fed funds rate is shown from 1954 to 2024: Download data In addition to revealing how much the Fed Funds rate has varied over time, there are two periods that stand out.

If 2022 was an unsettling year for equities, as I noted in my second data post, it was an even more tumultuous year for the bond market. Download data US Treasury rates rose across all maturities, but more so at the short end of the term structure (3 months, 1 year and 2 year) than at the long end (10 year or 30 year).

Equity funding has its downsides, too — for many founders, it’s , not worth diluting equity and ceding control of the business for a few million dollars of runway. Convertible debt is relatively low-interest and converts into equity at a specified date (generally after a round of equity financing). Download it here ➔

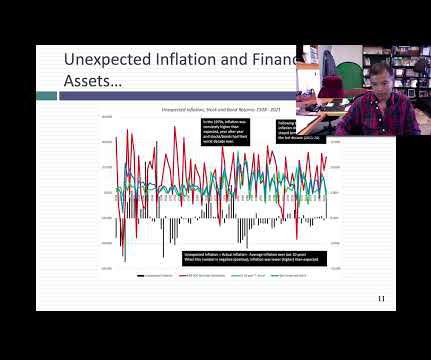

That said, the three primary inflation indices in the US, the CPI, the PPI and the GDP deflator all told the same story in 2021: Download historical inflation numbers The inflation rate during the course of the year reached levels not seen in close to 40 years, with every price index registering a surge.

I looked at global equities, broken down by region of the world, and in US dollars, to allow for direct comparison: India is the only region of the world to post positive returns, in US dollar terms, in the third quarter, and is the best performing market of the year, running just ahead of the US; note again that of the $5.2

Return on Equity 1. Equity Risk Premiums 2. Costs of equity & capital 4. Costs of equity & capital 1. Fundamental Growth in Equity Earnings 2. Return on Equity 2. Standard Deviation in Equity/Firm Value 2. Beta & Risk 1. Debt Ratios & Fundamentals 1. Debt Details 1. Buybacks 2.

In my second data update post from the start of this year , I looked at US equities in 2022, with the S&P 500 down almost 20% during the year and the NASDAQ, overweighted in technology, feeling even more pain, down about a third, during the year. US Equities in 2023: Into the Weeds! that was lost last year.

Download sector average betas ( US , Global ) Note the preponderance of financial service firms on the lowest risk ranks, but note also that almost all of them are substantial borrowers, and end up with levered risk levels close to average (one) or above.

Download Carla's slides Srividya Gopal Managing Director and Southeast Asia Valuation Leader, Kroll Srividya is Managing Director & Southeast Asia Leader, Valuation Advisory Services at Kroll. She is also a frequent guest speaker in top business schools' MBA courses.

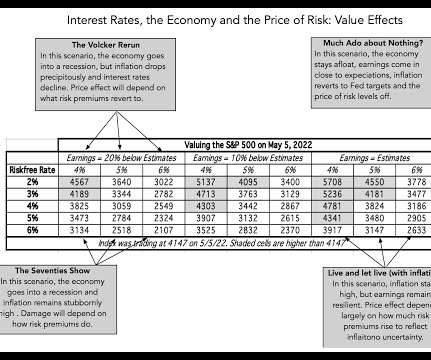

Investment Consequences As the storm clouds of higher inflation and interest rates, in conjunction with slower or even negative economic growth, gather, it should come as no surprise that equity markets are struggling to find their footing. At the close of trading on May 5, 2022, the S&P 500 stood at 4147, down 13.3%

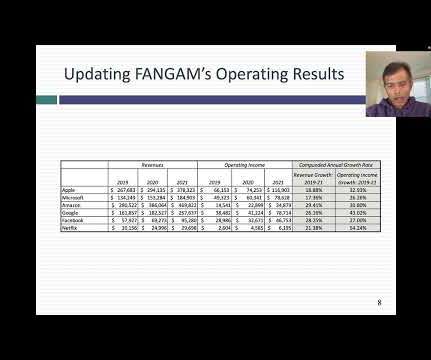

In the midst of all the action, to no one's surprise, have been six stocks (Facebook, Amazon, Netflix, Google, Apple and Microsoft or FANGAM) that have largely driven US equities for the last decade, roiling the market with their most recent earnings reports.

With a strong focus on start-ups, technology, and private equity, Peter is a frequent presenter and writer on valuation and accounting topics. Download The post IVS Accepted by the Australian Taxation Office (ATO) appeared first on International Valuation Standards Council. The date the report is issued.

In a third post on July 1, 2022 , I pointed to inflation as a key culprit in the retreat of risk capital, i.e., capital invested in the riskiest segments of every market, and presented evidence of the impact on risk premiums (bond default spreads and equity risk premiums) in markets.

With equities, the metric that has been in use the longest is the PE ratio, modified in recent years to the CAPE, where earnings are normalized (by averaging over time) and sometimes adjusted for inflation. Estimation Approaches Why is it so difficult to estimate an equity risk premium?

In the month since, I have added two more data updates, one on US equities and one on interest rates , but my attention was drawn away by other interesting stories. In fact, there are about a dozen countries that are unrated, where I have used their PRS scores to make estimates of their equity risk premiums.

You can download and adjust these templates to align with your message and your firm’s unique value proposition. To help you maximize the impact of the prospecting tool, we’ve created phone call and email templates to guide your outreach to each business owner.

Click to Download: ESG Valuation Considerations – Top Down or Bottom Up? ESG in Equity Analysis and Credit Analysis” was published in 2018 by the PRI, the Principles of Responsible Investment arm of the UN, and the CFA Institute. Executive Summary. More and more work is being done on the valuation aspect of ESG.

This is especially true for firms eyeing a capital infusion from private equity investor s. Today, a growing number of private equity investors are entering the accounting market as they’ve discovered that investing in accounting firms can yield great returns. Why is an accounting firm’s tech stack important to private equity?

(NASDAQ: DECA , the "SPAC")) announce the signing of an agreement and plan of merger for a proposed business combination (the "Business Combination Agreement"), which provides for a pre-transaction equity value of Semnur of $2.5 Download the presentation by clicking here. Download the publication by clicking here.

This enables them to deliver insightful valuations aligned to the international standards.” This publication supports valuation professionals when they initiate conversations with their clients on ESG factors that might impact the valuation of a business.

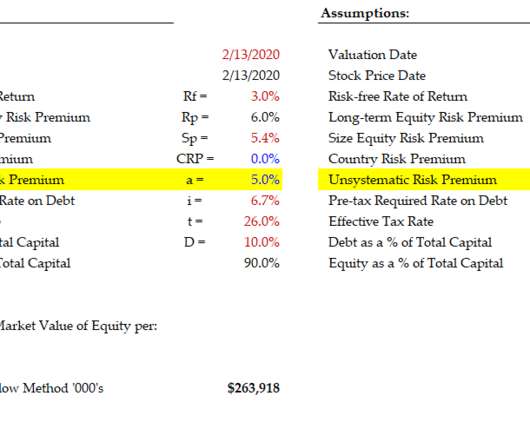

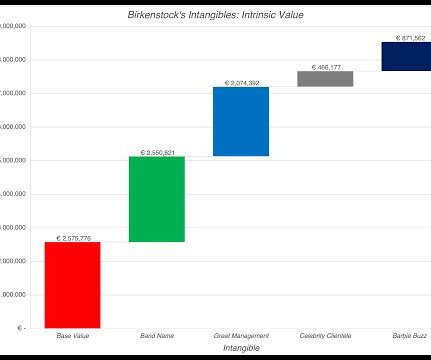

In this post, I will look at another initial public offering, Birkenstock, that is likely to get more attention in the next few weeks, given that it is targeting to go public at a pricing of about €8 billion, for its equity, in a few weeks. So, how far has accounting come in bringing intangible assets on to balance sheets?

This is due, in part, to a growing number of private equity firms entering the accounting market. As Allan D. Koltin, CEO of Koltin Consulting Group, explained, private equity firms perceive accounting firms as being low risk, high reward. M&A market heats up The M&A market is seeing an increase in activity.

In my last post, I looked at equities in 2023, and argued that while they did well during 2023, the bounce back were uneven, with a few big winning companies and sectors, and a significant number of companies not partaking in the recovery.

A debt warrant is an agreement in which a lender has a right to buy equity in the future at a price established when the warrant was issued or in the next round. The lender paid $9.17340 for each of the 400,000 Roku shares on which it wanted to exercise the equity warrant, paying a total of $3,669,360. Let's dive in.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content