This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Corporate finance jobs at normal companies are bad … …if you’re using them to break into a deal-based field, such as investment banking , private equity , or venture capital , or as a “Plan B” if you interview around but do not get into one of these. What Are Corporate Finance Jobs? not banks or investment firms).

In business schools, managers are taught to maximize the netpresentvalue (NPV) of future cash flows. We can broadly classify firms’ corporate behaviors into two categories: growth and value firms. Growth firms will issue equity to pay for acquisitions; value firms won’t.

Managers who anticipate these agency problems won’t invest in a moonshot even if they believe it has a positive netpresentvalue. But managers can’t properly motivate the employees by rewarding them with the company’s stock, because its price wouldn’t track the value of the moonshot alone.

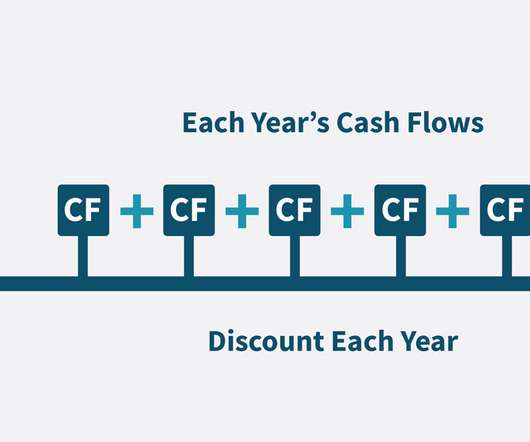

Different types of discount rates such as risk-free rate, cost of equity, or cost of debt, are used contextually in financial analysis. The Discounted Cash Flow (DCF) method uses the discount rate to consider all future cash flows of a business when calculating its current value.

This value is widely referred to as the “NetPresentValue” (NPV). . which produces a NetPresentValue of the Terminal Value of: $74 million. . So the Terminal Value here is three times as large! Ce = Cost of Equity. Rm – Rf) = Equity Market Risk Premium. B = Beta.

Analysts use financial metrics and multiples such as Price to Earnings (P/E), Price to Book (P/B), Enterprise Value to Sales (EV/Sales), Enterprise Value to EBITDA (EV/EBITDA), and Price to Book (P/B) ratios derived from trading data of similar public companies or deal pricing data of similar M&A transactions.

Balance Sheet Forecasts Balance sheet forecasts outline the expected assets, liabilities, and equity of a company at a future date. They provide insights into the financial position, capitalstructure, and overall worth of the business. The resulting netpresentvalue represents the estimated value of the business.

You may hear Asset Value used in place of Book Value, but this is not precisely correct because Book Value includes not only Asset Value, but also subtracts the value of liabilities of a company. It is typically the highest risk/highest potential return portion of a company’s capitalstructure.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content