This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Asset write-downs or impairments: A reduction in the bookvalue of assets or goodwill when they are deemed overvalued. Conversely, sectors commanding higher multiples, like Software, Biotechnology, and Healthcare, frequently benefit from strong growth prospects, higher margins, or scalable, technology-driven business models.

Breaking down companies by (S&P) sector, again both in numbers and market cap, here is what I get: While industrials the most listed stocks, technology accounts for 21% of the market cap of all listed stocks, globally, making it the most valuable sector. Dividends and Potential Dividends (FCFE) 1. BookValue Multiples 3.

Equity is cheaper than debt: There are businesspeople (including some CFOs) who argue that debt is cheaper than equity, basing that conclusion on a comparison of the explicit costs associated with each interest payments on debt and dividends on equity.

The first is the role that cash holdings play in a business , an extension of the dividend policy question, with an examination of why businesses often should not pay out what they have available to shareholders. In this post, I will bring together two disparate and very different topics that I have written about in the past.

Net Interest and Dividend Income Tax equivalent net interest income of $11.3 See SUPPLEMENTAL INFORMATION – Net Interest and Dividend Income on page 9 of this release for additional details. million, were partially offset by common stock dividends paid of $0.9 Bookvalue per common share of $22.79

With the success of the first quarter, the Board announced a quarterly cash dividend of $0.20 Bookvalue per common share was $32.15 for the fourth quarter of 2022, while tangible bookvalue per share (1) was $24.52 million in dividends during the first quarter of 2023. million, or 0.26%, from $512.1

Traditionally, the sector was viewed as a defensive play for investors who wanted stable dividends and no drama. That is still true for the average company in the industry: it is more defensive than something like technology or financial institutions. ” Different banks classify their power & utilities groups differently.

Additionally, Territorial shareholders will benefit from the considerable upside value of the stronger combined company as well as $10.5 million of incremental value from annual merger enabled cost savings and synergies, and Hope Bancorp's dividend, which is more than 1,000% higher than Territorial's standalone quarterly dividend.

The income-based approach determines a company’s value by assessing its anticipated future income-generating potential, employing methodologies such as Discounted Cash Flow (DCF) Analysis, Capitalization of Earnings, the Income Multiplier Method, Dividend Discount Model (DDM), and Earnings-Based Valuation.

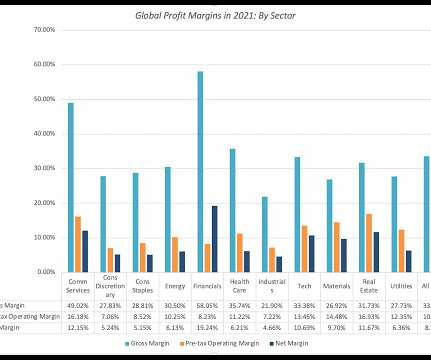

Real estate and utilities are the two sectors that have not come back fully from the COVID effect, but materials, technology and communication services are now reporting significantly higher earnings that before the shut down.

Your answer to that question will determine not just how you approach running the business, but also the details of how you pick investments, choose a financing mix and decide how much to return to shareholders, as dividend or buybacks. That said, global (US) companies collectively generated $5.3 trillion ($1.8

Uncover the intricacies of financial modeling, from understanding fundamental concepts like Free Cash Flow to Firm and Dividend Discount Model, to navigating advanced methodologies such as LBO and DCF. Candidates should highlight their commitment to staying updated on industry trends, regulations, and emerging technologies.

For example, I have seen it asserted that a stock that trades at less than bookvalue is cheap or that a stock that trades at more than twenty times EBITDA is expensive. Financing Flows Accounting Returns Dividends & Ownership Risk Premiums 1. Dividend Payout & Yield 1. EBITDA, EBIT and EBITDAR&D Margins 3.

In my second data update post from the start of this year , I looked at US equities in 2022, with the S&P 500 down almost 20% during the year and the NASDAQ, overweighted in technology, feeling even more pain, down about a third, during the year.

Common bookvalue per share decreased $0.71 Tangible common bookvalue per share decreased $0.69 at March 31, 2022 as this quarter's earnings, net of dividends paid, were outpaced by the increase in accumulated other comprehensive loss. Tangible common bookvalue per share decreased $0.69

Key Provisions The ruling outlines the principles and factors that should be considered when valuing a business, including the nature of the business, the economic outlook, the bookvalue of the stock, the company’s earning capacity, and the dividend-paying capacity.

Thus, an analyst who follows young technology companies may decide that paying ten times revenues for a company is a bargain, if all of the companies that he tracks trade at multiples greater than ten times revenues. buy stocks that trade at less than bookvalue or trade at PEG ratios less than one) for individual stocks.

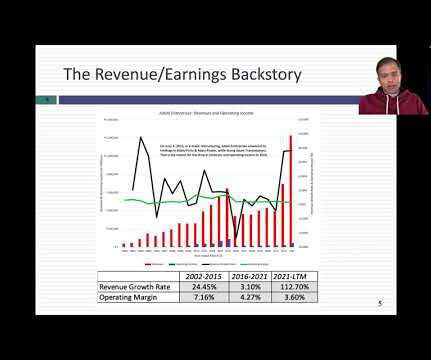

The PE ratio for the stock has gone from a modest 15 times earnings in the 2016-21 time period to 214 times earnings in the most recent two years, and the enterprise value has jumped from about 12 times EBITDA during 2016-21 to 53 times EBITDA in the most recent two years. times revenues in the most recent two years.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content