This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

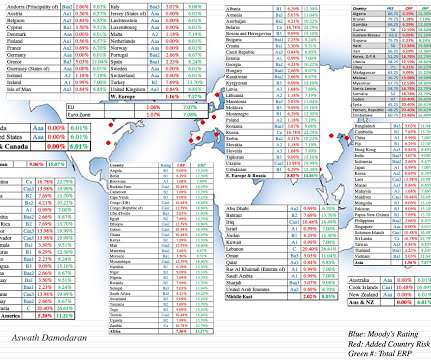

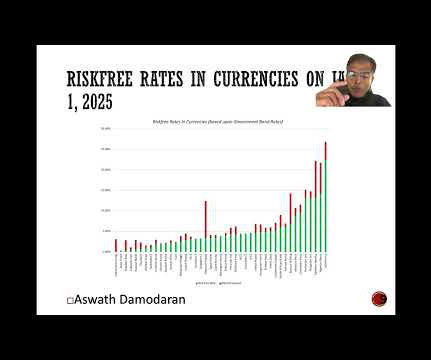

At the start of July, I updated my estimates of equity riskpremiums for countries, in an semiannual ritual that goes back almost three decades. If default risk seems like to provide too narrow a focus on countr risk, you can consider using country risk scores , which at least in principle, incorporate other components of country risk.

Since the ratings downgrade happened after close of trading on a Friday, there was concern that markets would wake up on the following Monday (May 19) to a wave of selling, and while that did not materialize, the rest of the week was a down week for both stocks and US treasury bonds, especially at the longest end of the maturity spectrum.

Thus, as you peruse my historical data on implied equity riskpremiums or PE ratios for the S&P 500 over time, you may be tempted to compute averages and use them in your investment strategies, or use my industry averages for debt ratios and pricing multiples as the target for every company in the peer group, but you should hold back.

In the first five posts, I have looked at the macro numbers that drive global markets, from interest rates to riskpremiums, but it is not my preferred habitat. The second set of inputs are prices of risk, in both the equity and debt markets, with the former measured by equity riskpremiums , and the latter by default spreads.

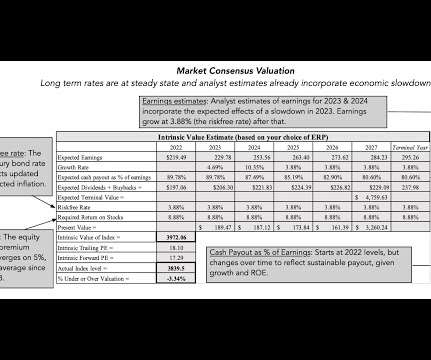

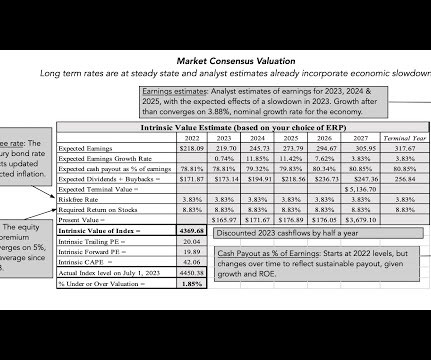

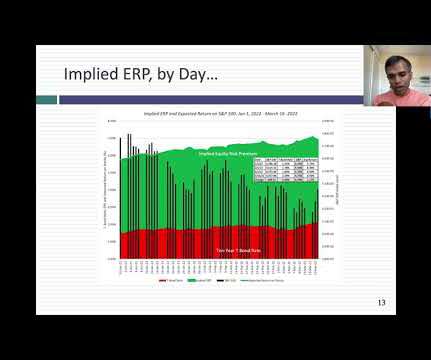

Thus, my estimates of equity riskpremiums, updated every month, are not designed to make big statements about markets but more to get inputs I need to value companies. In the table below, I show my estimates of the implied equity riskpremium for the S&P 500 at the start of every month, since January 2024, and on March 14, 2025.

There was undoubtedly some panic selling on Friday, but the flight to safety, whether it be in moving into treasuries or high dividend paying stocks, was muted. In the language of risk, they are demanding higher prices for risk, translating into higher riskpremiums.

By the start of 2022, the window for early action had closed and for much of this year, inflation has been the elephant in the room, driving markets and forcing central banks to be reactive, and its presence has already induced me to write three posts on its impact.

There are three possible explanations for the divergence: Short term versus Long term : The consumer survey extracts an expectation of inflation in the near term, whereas the treasury markets are providing a longer term perspective, since I am using ten-year rates to derive the market-implied inflation.

The premium that investors demand over and above the risk free rate is the equity riskpremium , and practitioners in finance have wrestled with how best to estimate that number, since it is not easily observable (unlike the expected return on a bond which manifests as a current market interest rate).

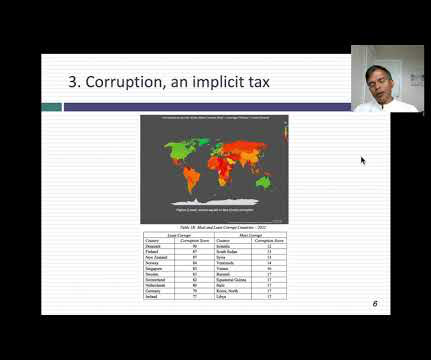

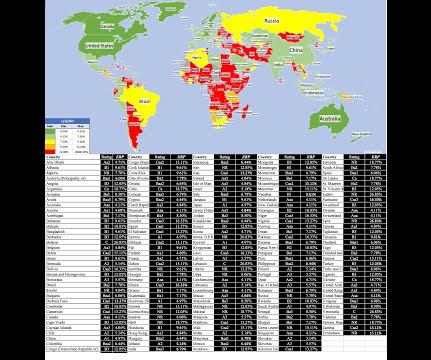

Country Risk: Equity Risk For equity investors, the price of risk is captured by the equity riskpremium, and equity riskpremiums will vary across countries. Please do not attach any political significance to my country groupings, or take them personally.

The US treasury market, considered by some still as a safe haven, was anything but safe or a haven, especially at the long maturities, as long term rates soared, with inflation (not the Fed) being the key driver. That is good advice in most years, but 2022 was not one of those years.

With this investment, you face price risk , since even though you know what you will receive as a coupon or cash flow in future periods, since the present value of these cash flows, will change as rates change. For an investment to be risk free then, it has to meet two conditions.

In my third post at the start of 2023, I looked at US treasuries, the long-touted haven of safety for investors. In 2022, they were in the eye on the storm, with the ten-year US treasury bond depreciating in price by more than 19% during the year, the worst year for US treasury returns in a century.

While we have increasingly given central banks primacy in discussions of interest rates, it remains my view that markets set rates, and while central banks can nudge market expectations, they cannot alter them.

Discounted cash flow approaches are also utilized within other functions of an organization, such as treasury, budgeting, financial planning and analysis, and tax planning. For instance, assume a bank is performing a discounted cash flow analysis for a mortgage.

Interest rates : To understand the link between expected inflation and interest rates, consider the Fisher equation, where a nominal riskfree interest rate (which is what treasury bond rates) can be broken down into expected inflation and expected real interest rate components. Louis estimates for inflation rates exceeding 2.5%

The idea is not new to encourage companies to increase their capitalization and reduce their bank debt (partly through more recourse to the capital market - CMU project). The rate would be calculated based on a 10-year "risk-free interest" rate depending on the currency, increased by a 1% riskpremium (1.5%

The second is that there are great (and free) sources for macro economic data, ranging from the Federal Reserve (FRED) to the World Bank and I don’t see the point of replicating something that they already do well. Micro Data The focus of my data collection is understanding how companies are operating and how investors are pricing them.

In my last post , I described the wild ride that the price of risk took in 2020, with equity riskpremiums and default spreads initially sky rocketing, as the virus led to global economic shutdowns, and then just as abruptly dropping back to pre-crisis levels over the course of the year. against developed market currencies.

In a post at the start of 2021 , I argued that while stocks entered the year at elevated levels, especially on historic metrics (such as PE ratios), they were priced to deliver reasonable returns, relative to very low risk free rates (with the treasury bond rate at 0.93% at the start of 2021).

The first is the return that can be earned on guaranteed investments , i.e., US treasury bills and bonds, for instance, if you are a investor in US dollar, since it is a measure of what someone who takes no or very low risk can expect to earn. That pullback has had its consequences, with equity riskpremiums rising around the world.

The overriding message in all of this data is that Russia/Ukraine war has unleashed fears in the bond market, and once unleashed that fear has pushed up worries about default and default risk premia across the board.

Investors in Saudi Arabia are still exposed to significant risks from political upheaval or unrest, and may prefer a more comprehensive measure of country risk. For three decades, I have wrestled with measuring this additional risk exposure and converting that measurement into an equity riskpremium, but it remains a work in progress.

The first has been the steep rise in treasury rates in the last twelve weeks, as investors reassess expected economic growth over the rest of the year and worry about inflation. The Stocks Story As treasury rates have risen in 2021, equity markets have been surprisingly resilient, with stocks up during the first three months.

After the 2008 market crisis, I resolved that I would be far more organized in my assessments and updating of equity riskpremiums, in the United States and abroad, as I looked at the damage that can be inflicted on intrinsic value by significant shifts in riskpremiums, i.e., my definition of a crisis.

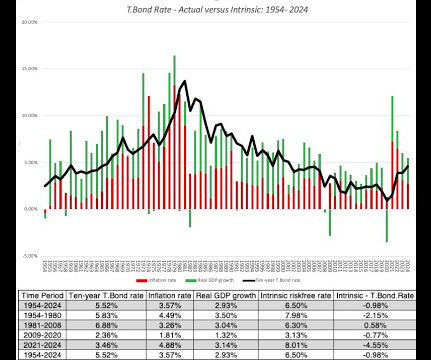

It was an interesting year for interest rates in the United States, one in which we got more evidence on the limited power that central banks have to alter the trajectory of market interest rates. In this post, I will begin by looking at movements in treasury rates, across maturities, during 2024, and the resultant shifts in yield curves.

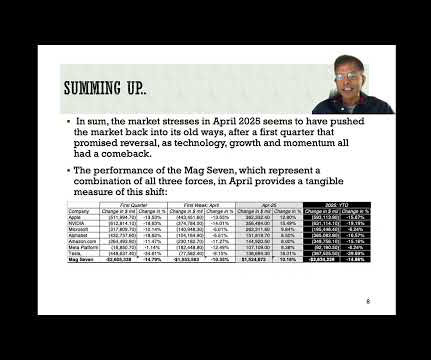

As equities careened through April 2025 between panic and delirium, the other asset classes were surprisingly staid, at least on the surface, starting with the US treasuries.

10] , [23] , [2] Discount Rate: The rate used to discount future cash flows is typically the cost of equity, calculated via the Capital Asset Pricing Model (CAPM): Cost of Equity = Risk-Free Rate + Beta * Market RiskPremium. [23] 23] Risk-Free Rate: Tied to government bond yields (e.g.,

Thus, if the US treasury bond rate (4.5%) is the riskfree rate in US dollars, and the expected inflation rates in US dollars and Brazilian reals are 2.5% Thus, if the US treasury bond rate (4.5%) is the riskfree rate in US dollars, and the expected inflation rates in US dollars and Brazilian reals are 2.5%

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content