This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Posted by Paul Washington, The Conference Board and Broadridge, on Monday, March 18, 2024 Editor's Note: Paul Washington is Executive Director of the ESG Center at the Conference Board and Chair of the Independent Steering Committee of Broadridge. This post is based on his Broadridge memorandum.

We employ our novel catalog of 83 board gender diversity interventions to examine the effect of BGD on a first-order firm outcome: investment efficiency. The effect of BGD on investment efficiency is an open question. more…)

Posted by Jillian Grennan (UC Berkeley), on Wednesday, March 13, 2024 Editor's Note: Jillian Grennan is an Associate Adjunct Professor of Finance and Sustainability at the University of California, Berkeley Haas School of Business.

Standard Deviation in Equity/FirmValue 2. Book Value Multiples 3. Thus, when computing my accounting return on equity in January 2024, I will be dividing the earnings from the four quarters ending in September 2023 (trailing twelve month) by the book value of equity at the end of September 2022. Profit Margins 1.

Posted by Lily Fang (INSEAD) and Sterling Huang (SMU), on Monday, May 20, 2024 Editor's Note: Lily Fang is a Professor of Finance at INSEAD and Sterling Huang is an Associate Professor of Accounting at Singapore Management University. This post is based on their recent article forthcoming in the Journal of Financial Economics.

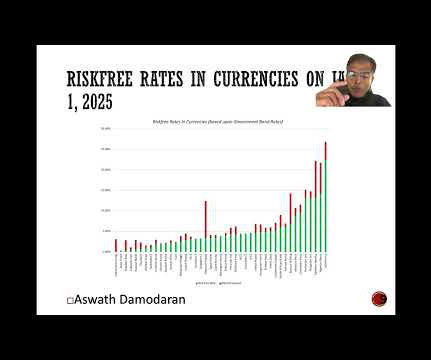

Not surprisingly, the company listings are across the world, and I look at the breakdown of companies, by number and market cap, by geography: As you can see, the market cap of US companies at the start of 2025 accounted for roughly 49% of the market cap of global stocks, up from 44% at the start of 2024 and 42% at the start of 2023.

Will firmvalue increase by appointing directors with mild non-financial concerns or with severe ones? This explains why fine-tuning the level of liability protection is not trivial: Changes in the board characteristics may have different implications on board compensation and liability protection. Available at SSRN: [link] or [link].

The revolutionary potential of artificial intelligence (AI) creates substantial uncertainty about its impact on firmvalue. In light of increasing pressure for transparency, firms may face growing scrutiny over the quality and credibility of their AI disclosures.

At the end of the first quarter of 2024, BlackRock’s assets under management (AUM)accounted for $10.5 This has led to the formation of a “latent network” of firms, connected by a few large investors. At the same time, managing systematic risk becomes more crucial for them than for investors in a single firm. trillion and $4.3

ENDNOTES [1] Hitchhike , Collins, [link] (last visited June 25, 2024). [2] 2024, at 4, [link]. (“One 1, 2024), [link] (“Invesco on Friday became the fifth major U.S. 24, 2024) , [link]. 6, 2024), [link]. That is down from 43% in a similar survey a year earlier, the investment bank said[.]”). [4] Institute for Econ.

Standard deviations in equity and firmvalue 4. Staleness : I update my data once a year, and I will not return to do an update until January 2024; the equity risk premiums for the US will get updated every month and the equity risk premiums for other countries will get a mid-year update. Cost of Debt 2. Price to Book 3.

Yet, in 2024, women earned, on average, 84 cents for every dollar a man earned, and Blacks and Hispanics/Latinos earned, on average, 77 cents and 73 cents, respectively, for every dollar a white worker was paid. Pay gaps lower labor costs, thus increasing net income and potentially firmvalue.

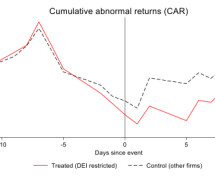

While many companies have embraced these efforts, investors have started to question whether DEI initiatives are truly valuable or merely a costly distraction from core business activities, as Elon Musk argued in several viral social media posts in 2024. This raises a critical question: Do investors collectively value corporate DEI efforts?

Posted by the Harvard Law School Forum on Corporate Governance, on Friday, May 24, 2024 Editor's Note: This roundup contains a collection of the posts published on the Forum during the week of May 17-23, 2024 Statement by Chair Gensler on Amendments to Regulation S-P Posted by Gary Gensler, U.S. Parker and Amanda L.

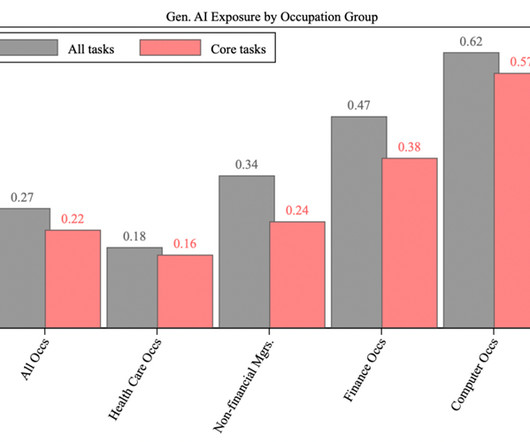

Eisfeldt (UCLA) and Gregor Schubert (UCLA), on Thursday, December 5, 2024 Editor's Note: Andrea L. In this post, which is based on our working paper, AI and Finance , we summarize research exploring how Generative AI tools influence firmvalue, firm decisions, and financial research. Posted by Andrea L. and Lori W.

By Dr. Aaron Mahl, EVP Business Development, iTValuations As the year winds down, we recently hosted our final webinar of 2024: M&A in 2024: A Year in Review. A Year of Contrasts in M&A Reed Warren highlighted some key takeaways from 2024. Click here to continue the conversation.

In companies with a controller that is, say, a majority owner, the controllers ownership stake forces her to bear the majority of the economic effect of her choices on firmvalue. These substantially distorted choices are expected to produce considerable agency costs (see, e.g., Cremers, Lauterbach,and Pajuste (2024) ).

I then fit this model to the data to estimate the underlying model parameters that describe the preferences of the board (with respect to compensation, CEO entrenchment, and efforts to maximize shareholder value) and shareholders (with respect to compensation, firmvalue, and their preferred vote outcome). percent, on average.

These investments are difficult to quantify and often underreported in traditional financial filings, creating uncertainty about the actual extent of firms AI investments. Despite these challenges, investor interest in AI has grown, and firms that make these investments in AI often benefit from premium valuations (Babina et al.,

billion in 2024, accounting for 86.3 A substantial share of this activity is directed toward regulatory agencies during the rulemaking process, where firms seek to influence policy through the submission of comment letters on proposed regulations. percent of total lobbying spending.

Principal Costs in the Solo-Owned, Owner-Managed Firm We trace principal costs to Jensen and Meckling’s seminal 1976 article. Their Figure 1 plots principal costs as a reduction of firmvalue related to the non-pecuniary consumption of the solo owner – consumption that maximizes the utility of the owner but also reduces the value of the firm.

In this post, I will expand my analysis of data in 2024, which has a been mostly US-centric in the first four of my posts, and use that data to take you on my version of the Disney ride, but on this trip, I have no choice but to face the world as is, with all of the chaos it includes, with tariffs and trade wars looming.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content