This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

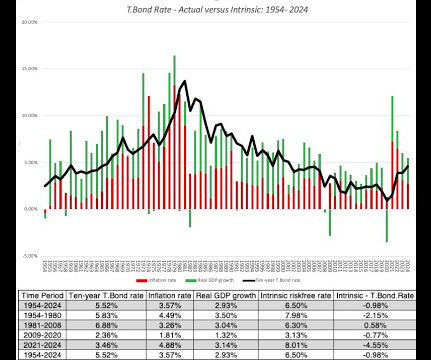

In every introductory finance class, you begin with the notion of a risk-free investment, and the rate on that investment becomes the base on which you build, to get to expected returns on risky assets and investments. What is a riskfree investment? Why does the risk-freerate matter?

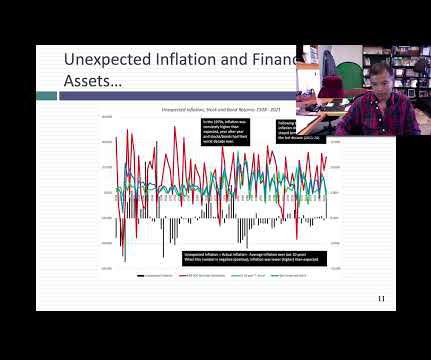

Inflation numbers have been coming in high now, for more than a year, but for much of the early part of 2021, bankers, investors and politicians seemed to be either in denial or casually dismissive of its potential for damage.

If, on the other hand, investors are risk neutral, the price of risk will be zero, and investors will buy risky business, stocks and other investments, and settle for the riskfreerate as the expected return. If you buy into this measure of equity risk premiums, consider its limitations.

The US treasury market, considered by some still as a safe haven, was anything but safe or a haven, especially at the long maturities, as long term rates soared, with inflation (not the Fed) being the key driver. Since inflation was 6.42% in 2022, the real return on a US 10-year treasury bond was -22.79%.

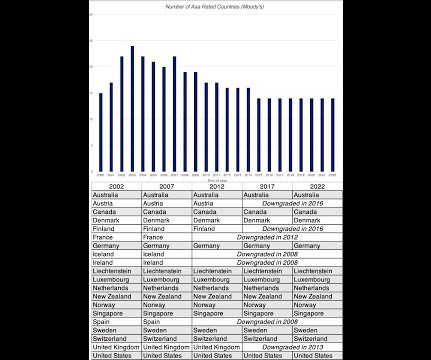

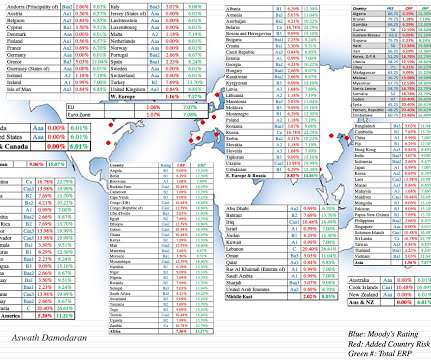

lived under full democracy, in 2021, with large differences across regions. Country Risk: Currency and Cost of Capital As a final part to this post, to see the shifts in country risk that we have seen in 2022, let’s start with an assessment of riskfreerates.

It is precisely because we have been spoiled by a decade of low and stable inflation that the inflation numbers in 2021 and 2022 came as such a surprise to economists, investors and even the Fed. As treasuryrates have risen, markets also seem to have been more wary about risk, and how it is being priced.

It is the nature of stocks that you have good years and bad ones, and much as we like to forget about the latter during market booms, they recur at regular intervals, if for no other reason than to remind us that risk is not an abstraction, and that stocks don't always win, even in the long term.

As we approach the mid point of 2021, financial markets, for the most part, have had a good year so far. Put simply, if you expect the annual inflation rate to be 2% in the future, you would need to set the interest rate on a bond above 2% to earn a real return. Louis estimates for inflation rates exceeding 2.5%

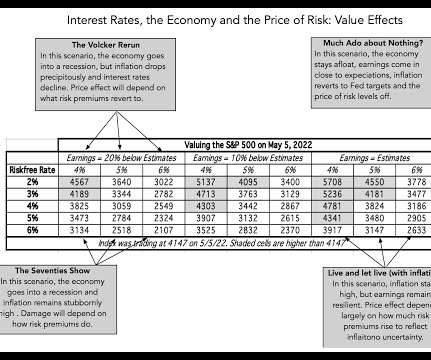

As I have argued in all four of my posts, so far, about 2022, it was year when we saw a return to normalcy on many fronts, as treasuryrates reverted back to pre-2008 levels, and risk capital discovered that risk has a downside.

Leading into 2021, the big questions facing investors were about how quickly economies would recover from COVID, with the assumption that the virus would fade during the year, and the pressures that the resulting growth would put on inflation.

The first quarter of 2021 has been, for the most part, a good time for equity markets, but there have been surprises. The first has been the steep rise in treasuryrates in the last twelve weeks, as investors reassess expected economic growth over the rest of the year and worry about inflation. for 2021 and inflation of 2.2%

Those measures took a beating in 2020, as COVID decimated the earnings of companies in many sectors and regions of the world, and while 2021 was a return to some degree of normalcy, there is still damage that has to be worked through.

Your choice of currency will affect your cash flows and your discount rates, but only because each currency brings it's own expectations of inflation, with higher inflation currencies leading to higher growth rates for cash flows and higher discount rates. the riskfree rate in Egyptian pounds is 14.38%.

In this post, I will begin by looking at movements in treasuryrates, across maturities, during 2024, and the resultant shifts in yield curves. I will follow up by examining changes in corporate bond rates, across the default ratings spectrum, trying to get a measure of how the price of risk in bond markets changed during 2024.

10] , [23] , [2] Discount Rate: The rate used to discount future cash flows is typically the cost of equity, calculated via the Capital Asset Pricing Model (CAPM): Cost of Equity = Risk-FreeRate + Beta * Market Risk Premium. [23] 23] Risk-FreeRate: Tied to government bond yields (e.g.,

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content