This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The Debt Trade off As a prelude to examining the debt and equity tradeoff, it is best to first nail down what distinguishes the two sources of capital. To me, the key distinction between debt and equity lies in the nature of the claims that its holders have on cash flows from the business.

For more established private businesses, some of which need capital to grow and some of which have owners who want to cash out, the capital has come from private equity investors.

In this post, I will begin by chronicling the damage done to equities during 2022, before putting the year in historical context, and then examine how developments during the year have affected expectations for the future. Actual Returns Your returns on equities come in one of two forms. Stocks: The What? at the start of that year.

In my last post , I discussed how inflation's return has changed the calculus for investors, looking at how inflation affects returns on different asset classes, and tracing out the consequences for equity values, in the aggregate.

I have also developed a practice in the last decade of spending much of January exploring what the data tells us, and does not tell us, about the investing, financing and dividend choices that companies made during the most recent year. Return on Equity 1. Dividends and Potential Dividends (FCFE) 1. Return on Equity 2.

Just look at the handy chart the Financial Times put together to see the horrifically bad numbers: In January 2022, everything seemed quite frothy, with mega-deals happening left and right and crypto and equity prices still at high levels. Real Estate (Equity Funds + Owned Properties): 15% [Up 5%]. Short-Term U.S. 2020: +38%.

2019) , for example, strong ESG performance correlates positively with higher equity returns and a reduction in downside risk. In a new paper, we address the impact of ESG ratings on a firm’s financial performance by studying how those ratings affect the cost of equity (COE). Sussman (2019). Nuttall (2019).

This is a Valuation Master Class student essay by Teeradon Piyakiattisuk from March 19, 2019. A firm uses a mix of equity and debt to minimize the cost of capital. A firm uses a mix of equity and debt to minimize the cost of capital. The popular method to find the cost of equity is the Capital Asset Pricing Model (CAPM).

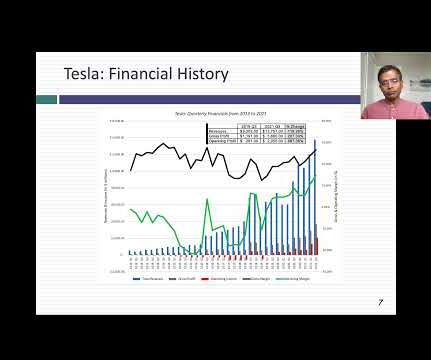

My two most recent valuations were in June 2019 and January 2020, and I am going to go back to them, not just because they are recent, but because they led to investment decisions on my part. In June 2019, Tesla had hit a rough spot, partly due to concerns about production bottlenecks and debt, and partly due to self inflicted wounds.

and far too little in equities. When the markets rallied after the initial COVID sell-off in March 2020, I put more cash into equities and real estate. And I reallocated these proceeds into crypto and equities and put in some excess cash. But my real estate investment funds were down ~10% , which hurt. I sold most of my U.S.

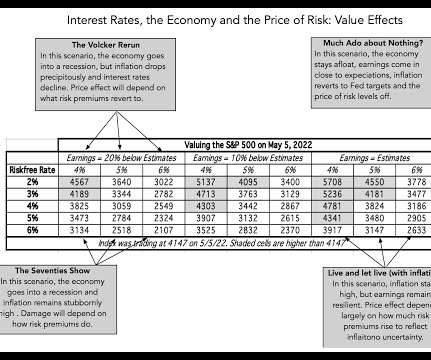

Investment Consequences As the storm clouds of higher inflation and interest rates, in conjunction with slower or even negative economic growth, gather, it should come as no surprise that equity markets are struggling to find their footing. At the close of trading on May 5, 2022, the S&P 500 stood at 4147, down 13.3%

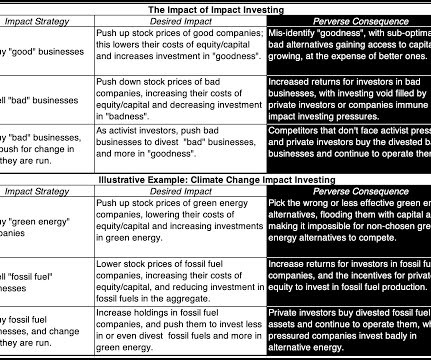

The effect of impact investing in the inclusionary and exclusionary paths is through the stock price , with the buying (selling) in inclusionary (exclusionary) investing pushing stock prices up (down), which, in turn, decreases (increases) the costs of equity and capital at these firms.

broadband subscribers, which is an 85% increase compared to 2019. In 3Q21, it recorded 51m users, up 10x compared to 2019. In 2019 and 2020, Globe recognized more than PHP4bn equity loss from its investment in Mynt. Dividend payout is high which means it could continue to deliver a solid dividend yield of 3%+.

After paying taxes on this income, the residual amount represents net income, the final measure of equity earnings, and the basis for computing earnings per share and other widely used measures of profitability used by equity investors.

Furthermore, the company increased dividends by 10% and announced that it will buy back GBP 2.3 (USD In 2019, the company announced that it plans to reduce its oil and gas output by 40% by 2030. by using the Discounted Cash Flow method, specifically our Flow-to-Equity approach, as well as a Trading Comparables analysis.

Equity dilution is another common method by which those in control of a corporation or LLC attempt to squeeze out a minority owner. Dilution and Excessive Compensation Challenges to dilutive equity awards commonly focus on equity that the company elects to award its employees or officers as compensation.

This strong share price performance was further bolstered by an average gross annual dividend yield of roughly 6% over the past 10 years. We analyzed TotalEnergies by using the Flow to Equity method and a Trading Comparables analysis. The Flow to Equity analysis produced a value of €272 billion, with a Cost of Equity of 8.9%.

This strong share price performance was further bolstered by an average gross annual dividend yield of roughly 6% over the past 10 years. We analyzed TotalEnergies by using the Flow to Equity method and a Trading Comparables analysis. The Flow to Equity analysis produced a value of €272 billion, with a Cost of Equity of 8.9%.

It raises $1bn new capital through the private equity fund TPG Rise Climate for a 11% stake. Given its losses over the past years, it did not pay out any dividends since 2016. We assume that there will be no dividends at least for the next 3 years. CAPEX is likely to stay much lower than 2017 to 2019 level. Conclusions.

One of the most common disputes that a poorly documented investment in a closely held company will produce is one of characterization: is the investment a loan or an equity purchase? If the company feels It does not need the second $50,000, the company has the right to do so and my equity will be diluted accordingly.

million shares for 14 cents per share in addition to interest and dividends. The contract usually has a high debt-to-equity ratio for which a high share of the purchase price is paid by borrowing against what is paid outright. The usual ratio is 90 percent debt and 10 percent equity. GE Credit Corporation purchased 2.3

That would have left you lagging the 181% price appreciation that you would have earned on the S&P 500 during the period, and even more so, if you consider the fact that you would have earned no dividends on Facebook, while generating about a 2% dividend yield, every year on the index.

Similarly, if a 10% US shareholder sells stock in a CFC, gain that would be treated as a dividend under Section 1248 of the Code may benefit from the 100% dividends received deduction. Comment: The pre-CAMT FSNOL carryover applies only to FSNOLs arising in taxable years ending after December 31, 2019. trade or business.

Debt-to-equity ratio in 2020 stood at 2.9x compared to 1x in 2019. Future cash flow proceeds serve debt repayments; don’t expect any dividends in near term. Refinery companies face high working cap requirements and fluctuating inventories. The company heavily increased its leverage during the pandemic. Ratios – PBF Energy.

3 per Osino Share and a total equity value of C$287 million on a fully-diluted in-the-money basis. million ounces of Proven and Probable Reserves, which was discovered by Osino in 2019 and fast-tracked to the pre-construction stage within four years. Immediate yield by way of participation in DPM's current dividend.

The second was that, starting mid-year in 2020, equity markets and the real economy moved in different directions, with the former rising on the expectations a post-virus future, and the latter languishing, as most of the world continued to operate with significant constraints.

smoothly shortened the settlement cycle for equities, corporate bonds, and municipal securities to one day after the transaction date (T+1). A nice benefit of going to T+1 is in the area of corporate actions, in that ex-dividend dates and record dates now are aligned on the same day. Last month, the U.S. This includes parts of U.S.

rise in return on equity (ROE) to 14.2%; and gains in tier 1 equity capital and assets of 5% and 4%, respectively. This was primarily based on revenue growth, which registered a heady 30% rise, allowing the bank to distribute its highest full-year dividend since 2008. billion; a 2.3% billion after-tax profit versus $8.3

Return on average tangible common equity (1). . . The return on average tangible assets was 1.07%, compared to 1.30%, and the return on average tangible common equity was 10.31%, compared to 12.37%. million lower unrealized gains from equity method investments included in the prior quarter and $0.7 0.60. . $. 0.74. . $.

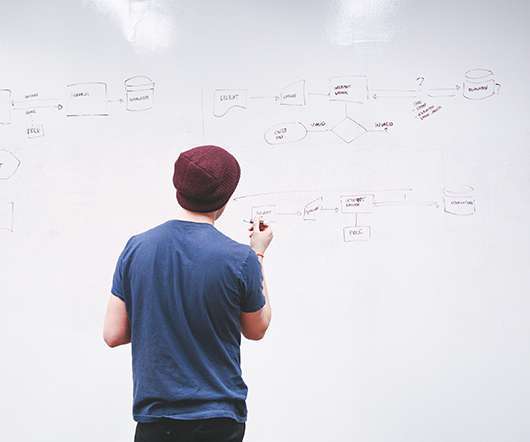

Brooklyn Nets NBA 2019 $2.40 That appeal may be only to a subset of individuals, but these buyers want to own the asset more for the emotional dividends, not the cashflows. Chelsea Premier League 2022 $5.30 Denver Broncos NFL 2022 $4.70 Phoenix Suns NBA 2023 $4.00 Milwaukee Bucks NBA 2023 $3.50 New York Mets MLB 2020 $2.40

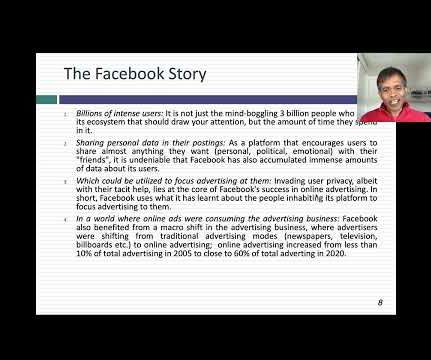

Until TikTok recently supplanted it at the top, Facebook had the most intense user base of any social media platform, with users staying on the platform roughly an hour a day in 2019. Amazon has also invested tens of billions in its other businesses, with its biggest payoff coming in the cloud business (notice a pattern here).

A nominating stockholder with a limited investment horizon may not be shy about cutting R&D expenses or long-term capital expenditures in favor of shorter-term payouts, or may be less adverse to incurring debt to finance a large dividend in the near term, even if financing costs will rise as a result. [20] See John C. Coffee et al.,

"The transaction also provides flexibility for the Combined Company to add capabilities in Leonardo DRS' core markets through targeted acquisitions and strategic investments as we expect to supplement strong organic growth with M&A and dividend distributions as part of our overall strategy going forward.". Combined Revenue.

If equity markets surprised us with their resilience in 2020, not just weathering a pandemic for the ages, but prospering in its midst, US equity markets, in particular, managed to find light even in the darkest news stories, and continued their rise through 2021. The year that was.

So-called “hedge clauses” were last addressed in the SEC Staff’s 2019 Fiduciary Duty Guidance (discussed here ), which expressed skepticism that hedge clauses are consistent with the antifraud provisions. A “ portfolio investment ” is any entity or issuer in which the private fund has invested directly or indirectly.

Financing Mix : Companies can raise capital either from equity or debt, and the costs of equity and debt can be altered when the tax rate changes. In a more telling statistic, the dollar value of taxes paid increased between 2017 and 2019 by 1.4% and the cash tax rate by 2.75%.

Under its provisions: 2/3 shareholder approval is required for any changes to salaries or “any matters which may in anywise affect, endanger or interfere with rights of the minority shareholders”; any surplus “may” be declared as dividends and distributed to shareholders; and. Course of Conduct Matters.

It is worth remembering that the Chinese government decided to crack down on its tech giants (Alibaba, Tencent, JD) in 2019, motivated more by control than by any consumer or competitive interests, and in the process not only set them back in the global markets by a significant amount, but hurt the Chinese economy and markets.

The number of no-action requests submitted to the Staff during the 2022 proxy season decreased 10% from 2021, but nevertheless was higher compared to prior years, up 5% from 2020 and 7% from 2019. Report on civil rights/racial equity audit. Report on civil rights/racial equity audit. Board declassification. 87.5% (13).

Musk [6] looked beyond a bright-line test of equity ownership percentage in deciding whether a CEO had control; and W. Because the dividends were paid out pro rata one share, one dollar the Delaware Supreme Court held that the dividend payout decision was not self-dealing and was subject to permissive business judgment review.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content