This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

This approach encourages dialogue focused on the business fundamentals the team, the market opportunity, the product, the financial projections rather than anchoring the conversation to arbitrary figures potentially derived from selectively chosen, and often inappropriate, market comparisons.

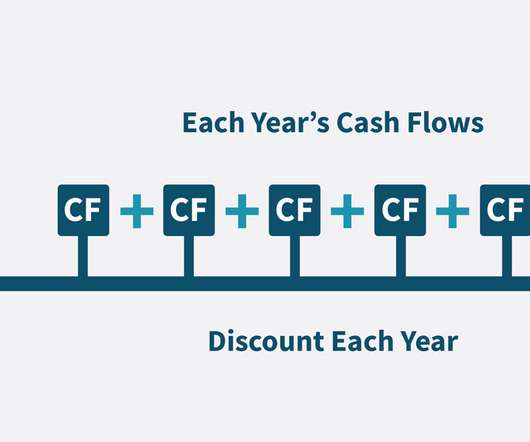

In particular, the Terminal Growth Rate is used in a DCF analysis to help calculate the TerminalValue. The Terminal Growth Rate and the TerminalValue are important figures in valuations, because they usually represent a significant contributor to the final valuation estimate.

The DDM is more grounded because it’s based on the company’s actual distributions and potential future value. And it values the company today based on the present value of its dividends and that potential future value (either the stock price or the EquityValue via the TerminalValue calculation).

But here, we use what interest we could get from an alternative investment in the market, called the Market Rate. Discount Factor (using Market Rate: r=10%). But first, a quick aside, which you can feel free to skip if you want to jump ahead: Why Do We Use the Market Rate to Calculate the Discount Factor? You get: Year.

While a growing number of appraisers use a discounted cash flow model to value illiquid minority interests of businesses ( 22% according to a recent Business Valuation Resources Survey ), the majority of appraisers continue to rely on restricted stock studies and pre-IPO studies in their marketability discount determinations.

This post provides a discussion of several implications of the definition of the standard of value known as fair marketvalue. We focus first on the definition of fair marketvalue. We then look at the implications for the so-called “marketability discount for controlling interests.”

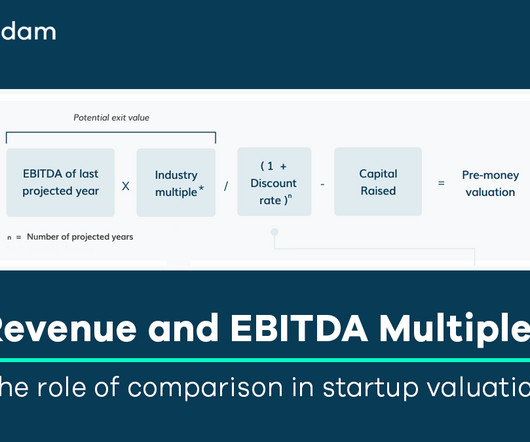

Imagine comparing products in the supermarket, where different box sizes and a range of pricing may make it hard to determine the value; labels that give you the price per kg of product can greatly simplify that process. A shortcut that many investors attempt to use is to apply a multiple.

Project Finance Definition: “Project Finance” refers to acquisitions, debt/equity financings, and new developments of capital-intensive infrastructure assets that provide essential utilities and services. However, many people also use the term more broadly to refer to equity, debt, and advisory for infrastructure assets.

These examples cover a range of topics, including discounted cash flow (DCF) analysis, comparable company analysis (CCA), and market multiples. Continuous Learning in Valuation Given the dynamic nature of financial markets, continuous learning is essential for professionals in valuation. What is Free Cash Flow to Equity?

Introduction and Conclusion My musings on the use of restricted stock discounts to estimate marketability discounts (or DLOMs) have led me to the conclusion: Restricted stock studies/discounts cannot be used to estimate DLOMs in any credible, standards-compliant manner. Three of the first four Mercer’s Musings posts address this issue.

Different methods are used, like looking at market prices, predicting future profits, and evaluating assets. Some techniques include comparing companies in the market, estimating future cash flows, and assessing the value of tangible assets. to its marketvalue.

To discover how blue sky valuation combined with the Discounted Cash Flow (DCF) method helps assess intangible assets like brand equity, intellectual property, and goodwill. It estimates a company’s intrinsic value based on future cash flows, discounted back to their present value. Calculating terminalvalue.

The second and third musings address the issue of marketability discounts and conclude that it is not possible to comply with any valuation standards, whether USPAP or not, using only averages of restricted stock studies as a basis for “guessing” marketability discounts. The relevant pool of potential buyers, if any.

Invested Capital Growth (ICG), as defined by The Economic Times, is “the appreciation in the value of an asset over a period of time.” It is calculated by comparing the current value of a stock, sometimes known as the marketvalue of an asset or investment, to the amount paid when you originally bought it. References.

No Right or Wrong Answers – Some technical questions have correct answers, but many market and investment ones do not. Market and Investment Questions – Which startup would you invest in? Which market is attractive? Which markets should we avoid? Q: Why not private equity, growth equity, hedge funds, or entrepreneurship?

Key Concepts to Know: Before diving into the valuation techniques, it's important to understand concepts like the time value of money, risk and return trade-off, and the significance of growth rates. Various Approaches to Valuation: Valuation can be approached through three main methods - market-based, asset-based, and income-based valuation.

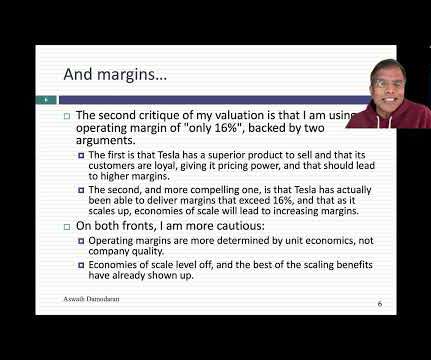

Finally, my starting cost of capital of 10.15% reflects the reality that the riskfree rate and equity risk premiums have risen over 2022, and my ending number of 9% is an indication that I expect Tesla to become less risky over time. It was the reason that I argued at a $1.2

Metals & Mining Investment Banking Definition: In metals & mining investment banking, professionals advise companies that find, produce, and distribute base metals, bulk commodities, and precious metals on debt and equity issuances and mergers and acquisitions. and Industrias Peñoles (Mexico). silver and platinum).

Were also bigger and had higher market capitalizations and better operating performance, on average. Market Pricing and Restricted Stock Discounts. The next figure examines the offer amounts, size of the transactions, and market pricing of the dividend-paying restricted stock issuers. We make observations from the second figure.

Oil & Gas Investment Banking Definition: In oil & gas investment banking, professionals advise companies that search for, produce, store, transport, refine, and market energy on raising debt and equity and completing mergers and acquisitions. Downstream: 31 (mix of everything, but no private equity activity).

Atticus Frank will present tomorrow and talk about why market multiples differ between and among industries. It is essential to normalize the earnings of operating companies when providing appraisals either at the financial control/marketable minority level or the nonmarketable minority level. These sessions are always lots of fun.

S ection 3: What Influence Do Markets Have on Startup Valuation? Valuing startups relies heavily on assumptions about future performance, interpretations of market trends, and the specific perspectives and risk appetites of the involved parties. [3] This exploration will cover: Section 1: What is Startup Valuation?

Communicating Future Potential Section 3: Riding the Waves: The Influence of Markets Section 4: The Goal of Valuation: Building Investor Confidence Section 5: The Founder’s Valuation Playbook Section 6: Bridging the Gap: Founder, Investor, and Advisor Perspectives Section 1: What is Startup Valuation? 11] [13] Internal/Compliance (e.g.,

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content