This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Thus, as you peruse my historical data on implied equity riskpremiums or PE ratios for the S&P 500 over time, you may be tempted to compute averages and use them in your investment strategies, or use my industry averages for debt ratios and pricing multiples as the target for every company in the peer group, but you should hold back.

Breaking down just US equities, by sector, we can see the damage across sectors: The technology sector lost the most in value last week, both in dollar terms, shedding almost $1.8 In the language of risk, they are demanding higher prices for risk, translating into higher riskpremiums.

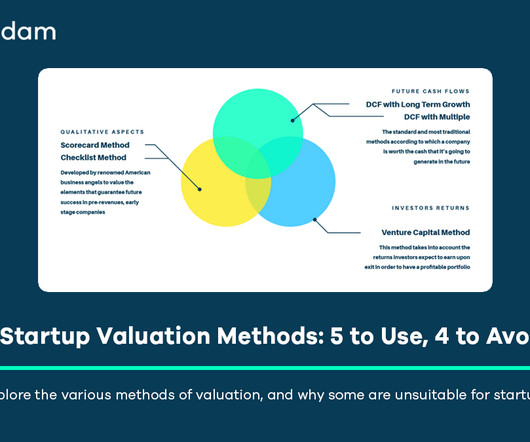

Critiquing Unsuitable Methods for High-Growth Startups Several traditional or overly simplistic methods fail to adequately capture the unique characteristics of technology startups. butcher, barber) where assets are tangible and customer acquisition straightforward, it breaks down for technology startups.

By the same token, it is impossible to use a pricing metric (PE or EV to EBITDA), without a sense of the cross sectional distribution of that metric at the time. For example, I have seen it asserted that a stock that trades at less than book value is cheap or that a stock that trades at more than twenty times EBITDA is expensive.

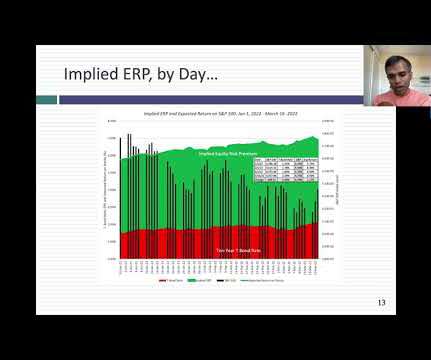

In my last three posts, I looked at the macro (equity riskpremiums, default spreads, risk free rates) and micro (company risk measures) that feed into the expected returns we demand on investments, and argued that these expected returns become hurdle rates for businesses, in the form of costs of equity and capital.

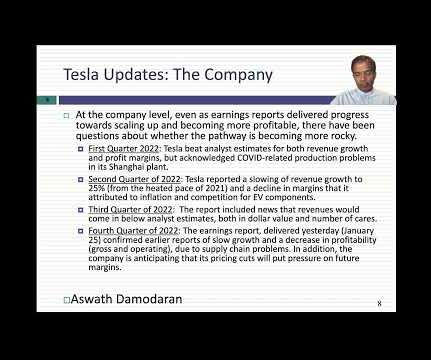

Tesla's rise is summarized in the graph below, where we look at the company's revenues and earnings over time, with earnings measured in gross and operating terms, and EBITDA capturing operating cash flows: 2022 numbers updated to reflect 4th quarter earnings call on 1/25/23 Between 2010 and 2020, Tesla grew revenues from $117 million to $31.5

One is to compute the taxes you would have paid on operating income, if it had been fully taxable, to get after-tax operating income and margin , and the other is to add back depreciation to operating income to get EBITDA and EBITDA margin.

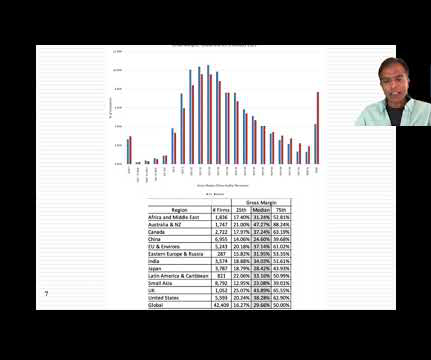

I use the data through the end of 2023 to compute all three measures for every company, and in my first breakdown, I look at these risk measures, by sector (globally): Utilities are the safest or close to the safest , on all three price-based measures, but there are divergences on the other risk measures.

The overriding message in all of this data is that Russia/Ukraine war has unleashed fears in the bond market, and once unleashed that fear has pushed up worries about default and default risk premia across the board.

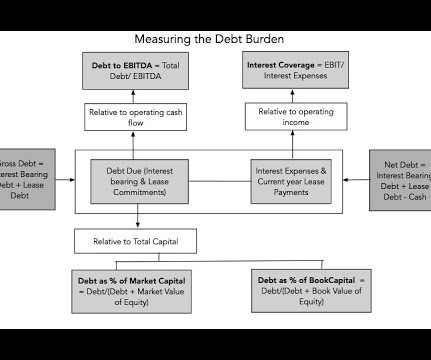

An Optimizing Tool In my second and third data posts for this year, I chronicled the effects of rising interest rates and riskpremiums on costs of equity and capital. Debt to EBITDA, Interest Coverage Ratios If debt to capital is not a good measure for judging over or under leverage, what is?

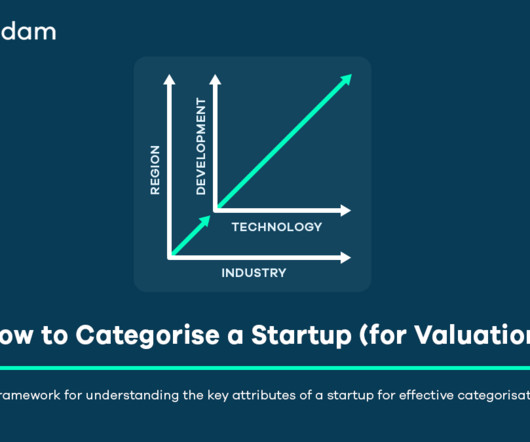

Categorisation poses a significant challenge in startup valuation, with investors and founders frequently mixing up markets, business models, industries, and underlying technologies. Equidam Category List ) Development Stage (Intrinsic Risk Factors) Development Stage focuses on intrinsic risk factors tied to the startups maturity.

Breaking down the remaining sectors, real estate and utilities are the heaviest users of debt, and technology and health care the lightest. In the table below, I look at debt to EBITDA and interest coverage ratios, by region and sector: The results in this table largely reaffirm our findings with the debt to capital ratio.

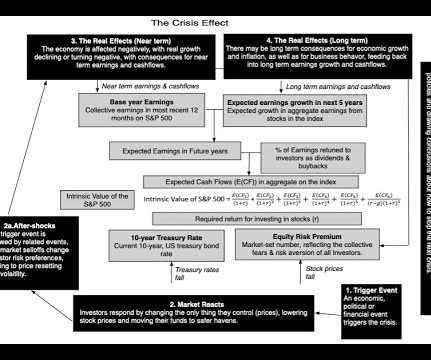

Instead, you will have to revalue the company, with adjustments to expected cash flows and riskpremiums, given the crisis, and if that value exceeds the price, you should buy the stock. Contrarian Investing: The Psychological Tests! In the abstract, it is easy to understand the appeal of contrarian investing.

4] , [3] , [5] Unlike mature, publicly listed companies which are easier to compare using multiples of current earnings (like EBITDA) [3] , startups must be valued based on their projected future; moats, margins and the perceived strength of their future growth trajectory. [3] 23] Risk-Free Rate: Tied to government bond yields (e.g.,

2] Startups typically lack significant historical financial data, often operate with negative profits initially, rely heavily on private equity or venture capital rather than traditional bank loans, and face a much higher risk of failure. [1] This de-risks the execution aspect of the future plan. 1] [4] [6] [14] [18]. 2] [15] [17].

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content