This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

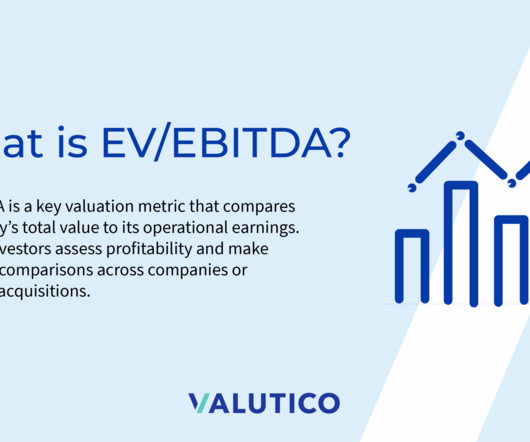

The core idea behind relative valuation is to estimate a company’s value by comparing it to similar companies based on how the market prices their financial metrics. EV/EBITDA is a widely used multiple in this relative valuation approach. What is EV/EBITDA? Breaking down the multiple What is EBITDA?

If you search for “how to start a privateequityfirm” online, you’ll find results that range from useless to tangentially useful to occasional nuggets of real wisdom. Starting a privateequityfirm is a bad decision for ~95% of people who work in the finance industry. Degrees such as an MBA or a Ph.D.

The lower middle market typically encompasses businesses with $2-10 million in EBITDA or enterprisevalues between $10-100 million. REAG s target market includes the United States and businesses between $2M and $25M in EBITDA and up to $250M in revenue. A key distinction in this space is the buyer profile.

But the real question is this: If you accept an industrials privateequity job, will you end up more like Andrew Carnegie or Henry Phipps, or will your career trajectory resemble a distressed tire manufacturing company that later declared bankruptcy?

According to some, you do almost no modeling or technical work in this group, and it’s one of the easier jobs in IB, similar equity or debt capital markets. But if you read other accounts, FSG runs models, Analysts get hands-on technical work, and the hours could be longer and more stressful because your clients are privateequityfirms.

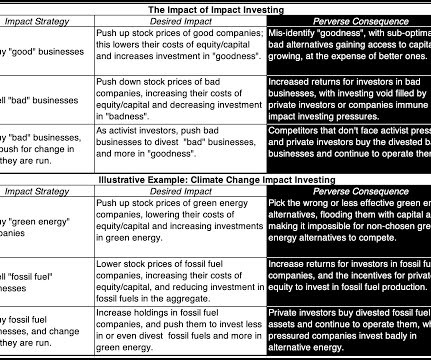

On the alternative energy front, as money has flowed into these companies, there has been a surge in enterprisevalue (equity and net debt) and market capitalization (equityvalue); I report both because impact investing can also take the form of green bonds, or debt, at these companies.

Leveraged Buyouts (LBOs) are powerful tools in the financial world, used by privateequityfirms and savvy investors to maximize returns. They involve acquiring a company using a mix of debt and equity, where the acquired company’s cash flows are used to service the debt. Ready to master the art of LBOs?

MCM Capital Partners (MCM) is a lower-middle market privateequity fund. Founded in 1992, MCM is a Cleveland-based privateequityfirm focused on acquiring niche manufacturers, value-added distributors and service companies generating up to $75 million in annual revenues and having enterprisevalues of less than $50 million.

Debt Service = Interest + Scheduled Principal Repayment; CFADS = EBITDA – Cash Taxes +/- Change in Working Capital – Maintenance CapEx +/- various Reserve line items.) the value of the target company’s core business operations in the deal). an equity IRR of 7% to 13%). Wait, How Does Project Finance Math Work?

These ratios, like the EBITDA multiple, compare a company’s financial performance (EBITDA, revenue, etc.) to its market value. These multiples are applied to target company’s latest financials such as revenue, earnings and book value of equity to arrive at an estimate of enterprisevalue or equityvalue.

GF: Are you seeing more mergers and acquisitions involving self-funded public companies and privateequityfirms? Eventually, privateequity will lead coming out of this. We’re in a relatively stable environment, and it provides an opportunity for privateequityfirms to step back into the deal arena.

It is 100% possible to use standard valuation multiples, such as P / E and TEV / EBITDA , to value power/utility companies, and you’ll see many examples in the Fairness Opinions below. EnterpriseValue / Capacity ($ per MW): Finally, for power generation companies, capacity is the key top-line driver that determines revenue.

Discounted Cash Flow Value Discounted Cash Flow Value refers to the calculation of a company’s EnterpriseValue on the basis of its ability to generate free cash flow over time. EBITDA Multiple EBITDA Multiple refers to the multiple of EBITDA used to determine a company’s enterprisevalue.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content