This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

This ratio offers insight into a companys profitability and relative value by comparing its total worth (EnterpriseValue, encompassing debt and equity) to its operational earnings (EBITDA). The multiple is calculated as EnterpriseValue (EV) divided by EBITDA. What is EnterpriseValue?

Historical Data: 1930-2019 To see how this framework works in practice, let's start by looking at the performance of US stocks, across the decades, and look at the returns on stocks, broadly categorized based on marketcapitalization and price to book ratios.

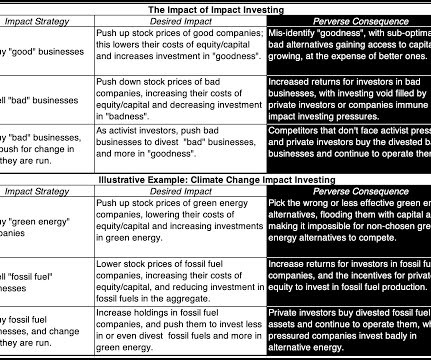

Even when you are successful in dissuading these companies from "bad" investments, but may not be able to stop them from returning the cash to shareholders as dividends and buybacks, rather than making "good" investments. trillion of cumulated enterprisevalue at fossil fuel companies. in the 1998-2010 time period to 5.95

By analyzing factors like the price-to-earnings (P/E) ratio, price-to-book (P/B) ratio, and enterprisevalue-to-EBITDA (EV/EBITDA) ratio, companies can determine if their shares are undervalued or overvalued compared to peers. Dividend Discount Model DDM estimates the present value of expected future dividends from owning a stock.

How does negative equity affect dividends? Is negative equity value common in startups? Can a company still raise capital with negative equity? This pivotal metric is typically calculated by summing the marketcapitalization and net debt of the organization. What are some famous companies that had negative equity?

The income-based approach determines a company’s value by assessing its anticipated future income-generating potential, employing methodologies such as Discounted Cash Flow (DCF) Analysis, Capitalization of Earnings, the Income Multiplier Method, Dividend Discount Model (DDM), and Earnings-Based Valuation.

Data universe : In my sample, I include all publicly traded firms with marketcapitalizations that exceed zero, traded anywhere in the world. At the company-level, I provide data on risk, profitability, leverage and dividends, broken down by industry-groups, to be used in both corporate finance and valuation. Return on Equity 1.

("Urstadt Biddle" or "UBP") (NYSE: UBA ) today announced that the two companies have entered into a definitive merger agreement (the "Agreement") by which Regency will acquire Urstadt Biddle in an all-stock transaction, valued at approximately $1.4 billion, including the assumption of debt and preferred stock.

While the universe of companies is diverse, with approximately half of all firms from emerging markets, it is more concentrated in marketcapitalization, with the US accounting for 40% of global marketcapitalization at the start of the year.

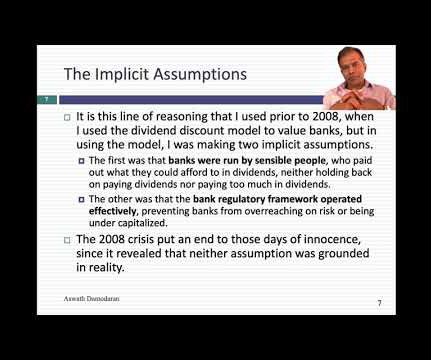

Consequently, you can only value the equity in a bank, and by extension, the only pricing multiples you can use to price banks are equity multiples (PE, Price to Book etc.). The notion of computing a cost of capital for a bank is fanciful and fruitless, and any attempt to compute an enterprisevalue for a bank is destined to end in failure.

An intuitive reading of the FCFE is that it is cash available to be returned to equity investors, either in the form of dividends or as cash buybacks. It is the rare firm that follows a residual cash policy, returning its FCFE every year as dividends and/or buybacks.

Given the historical roots of the biggest Indian family groups, the Adani Group has been a recent entrant, not making the top ten list (in terms of either operating metrics like revenues or market-based numbers like marketcapitalization or enterprisevalue) as recently as ten years ago, and barely making the top ten list five or six years ago.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content