This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

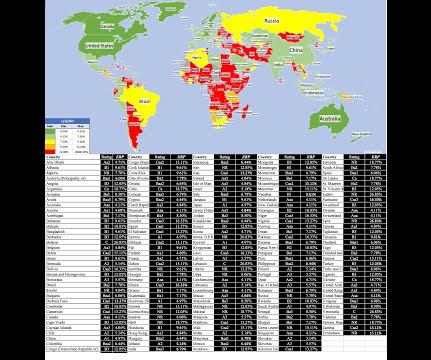

At the start of July, I updated my estimates of equity riskpremiums for countries, in an semiannual ritual that goes back almost three decades. As with some of my other data updates, I have mixed feelings about publishing these numbers.

In corporatefinance and investing, which are areas that I work in, I find myself doing double takes as I listen to politicians, market experts and economists making statements about company and market behavior that are fairy tales, and data is often my weapon for discerning the truth. Beta & Risk 1. Equity RiskPremiums 2.

In the first five posts, I have looked at the macro numbers that drive global markets, from interest rates to riskpremiums, but it is not my preferred habitat. A few years ago, I wrote a paper for practitioners on the cost of capital , where I described the cost of capital as the Swiss Army knife of finance, because of its many uses.

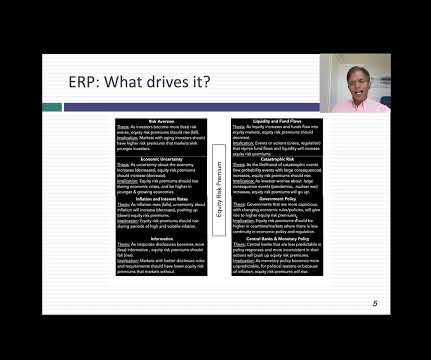

If you have been reading my posts, you know that I have an obsession with equity riskpremiums, which I believe lie at the center of almost every substantive debate in markets and investing. That said, I don't blame you, if are confused not only about how I estimate this premium, but what it measures.

The US treasury market, considered by some still as a safe haven, was anything but safe or a haven, especially at the long maturities, as long term rates soared, with inflation (not the Fed) being the key driver. That is good advice in most years, but 2022 was not one of those years.

After the rating downgrade, my mailbox was inundated with questions of what this action meant for investing, in general, and for corporatefinance and valuation practice, in particular, and this post is my attempt to answer them all with one post. What is a risk free investment? Why does the risk-free rate matter?

Government Bond/Bill Rates in 2023 I will start by looking at government bond rates across the world, with the emphasis on US treasuries, which suffered their worst year in history in 2022, down close to 20% for the year, as interest rates surged. The Fed Effect: Where's the beef? The Fed Effect: Where's the beef?

The first is that I do not have a macro focus, and my interests in macro variables occur only in the context of corporatefinance or valuation issues. In the same dataset where I compute historical equity riskpremiums, I report historical returns on corporate bonds in two ratings classes (Moody’s Aaa and Baa ratings).

A few of these variables are macro variables, but only those that I find useful in corporatefinance and valuation, and not easily accessible in public data bases. Rather than replicate that data, my macroeconomic datasets relate to four key variables that I use in corporatefinance and valuation.

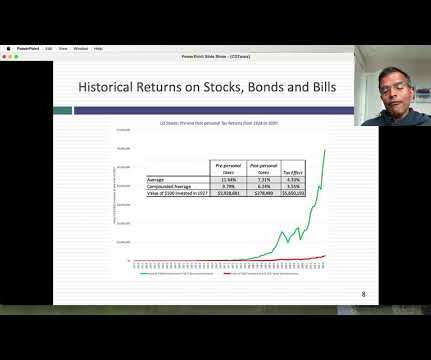

Historical Stock Returns: Pre and Post-tax At the start of every year, I update a dataset , where I look at historical returns on stocks over time, and compare these returns to returns on treasury bonds/bills, corporate bonds and gold.

After the 2008 market crisis, I resolved that I would be far more organized in my assessments and updating of equity riskpremiums, in the United States and abroad, as I looked at the damage that can be inflicted on intrinsic value by significant shifts in riskpremiums, i.e., my definition of a crisis.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content