This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

revenue multiple, ARR multiple, EBITDA multiple) derived from recent acquisitions or funding rounds of supposedly similar companies. This incorporates the risk-free rate, a market risk premium specific to the company’s country, and Beta ($beta$). Beta measures the volatility of the company relative to the market.

Beta & Risk 1. EBIT & EBITDA multiple s 5. Since I update the data only once a year, it will age as we go through 2025, but that aging will be most felt, if you use my pricing multiples (PE, PBV, EV to EBITDA etc.) Return on Equity 1. Debt Ratios & Fundamentals 1. Debt Details 1. Buybacks 2. Equity Risk Premiums 2.

In a final assessment, I break down companies based upon operating cash flows (EBITDA as a percent of enterprise value) and dividend yield (dividends as a percent of market capitalization). On bond ratings, there is no discernible link between ratings and returns, until you get to the lowest rated bonds (CCC & below).

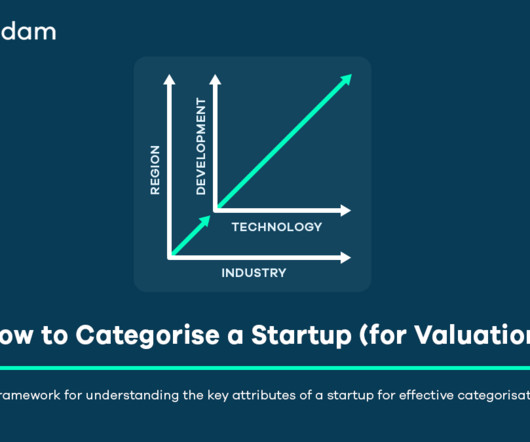

This potential is typically evaluated through assumptions about future growth trajectories, often modeled via projected revenue growth or, in more mature markets, EBITDA projections. However, in the practical, often more uncertain world of venture capital, the focus shifts towards assessing a startup’s exit potential.

Its financial profile now looks like this: Its Debt / EBITDA is now 10x, its EBITDA / Interest has fallen below 1x, the Secured Debt is trading at 90% of its face value, and the Unsecured Debt is down to 60%. A few years later, the company’s industry declined, and it was slow to cut costs and enter new markets.

Beta & Risk 1. EBIT & EBITDA multiple s 5. Working capital needs Thus, I compute pricing multiples based on revenues (EV to Sales, Price to Sales), earnings (PE, PEG), book value (PBV, EV to Invested Capital) or cash flow proxies (EV to EBITDA). Return on Equity 1. Debt Ratios & Fundamentals 1. Debt Details 1.

By the same token, it is impossible to use a pricing metric (PE or EV to EBITDA), without a sense of the cross sectional distribution of that metric at the time. For example, I have seen it asserted that a stock that trades at less than book value is cheap or that a stock that trades at more than twenty times EBITDA is expensive.

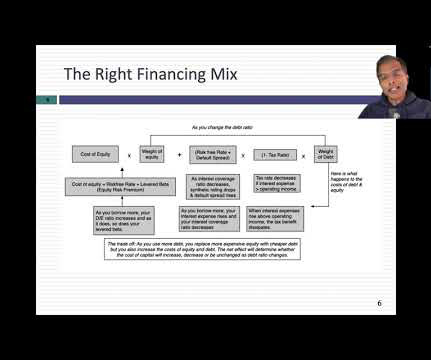

In our forecast, Cash rises too much, and Debt / EBITDA goes from 5.0x Dividend Discount Model, Part 4: Present Value of Terminal Value and Dividends Since the Dividend Discount Model is based on Equity Value, not Enterprise Value, the Discount Rate is the Cost of Equity: Risk-Free Rate + Equity Risk Premium * Levered Beta.

Practitioners assume the business is sold as a multiple of some financial metric like EBITDA, based on what they can see today for other businesses that were sold, and what these comparable trading multiples are. . B = Beta. (Rm EV/EBITDA Multiple. Exit Multiple (EV/EBITDA). Ce = Cost of Equity. Rf = Risk-free Rate.

In maturity, with debt entering the financing mix, net margins become good measures of profitability, and in decline, as earnings decline and capital expenditures ease, EBITDA margins dominate.

EBITDA multiple , matching its own. EBITDA since it’s only growing at 2-3% per year vs. 5-10% per year for Jacobs. A Sample Event-Driven Hedge Fund Trade To illustrate how these hedge funds work, I’ll walk through an announced spin-off here – Jacobs Solutions’ plan to divest its Critical Mission Solutions (CMS) division.

For both paid and shared AMIs, developers must meet the following criteria : Sell publicly available, full-feature production-ready software (not a beta product). Typically, the benchmark of Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA) is applied.

In short, if you don't like betas and have disdain for modern portfolio theory, your choice should not be to abandon risk measurement all together, but to come up with an alternative risk measure that is more in sync with your view of the world.

If Midstream companies want to grow beyond the fee increases written into their contracts and possible volume growth, they need to spend on Growth CapEx and estimate the incremental EBITDA from that spending: Further adding to the complexity is the GP (General Partner) / LP (Limited Partner) structure used at most MLPs.

One simplistic proxy for this cash generating capacity is EBITDA as a percent of enterprise value (EV), with higher (lower) values indicating greater (lesser) cash flow generating capacity. Debt to EBITDA, Interest Coverage Ratios If debt to capital is not a good measure for judging over or under leverage, what is?

With Valutico’s new development, practitioners can quickly perform a VC valuation based on EV/Sales, EV/EBITDA, EV/EBIT and P/E multiples as a useful addition to other research on the company and the industry. The calculation of these discount rates are based on the observed betas of similar listed peer companies.

Equidam leverages industry-specific parameters such as EBITDA multiples, long-term growth rates, industry betas, and market risk premiums, aligning valuations with real-world market conditions and competitive dynamics.

4] , [3] , [5] Unlike mature, publicly listed companies which are easier to compare using multiples of current earnings (like EBITDA) [3] , startups must be valued based on their projected future; moats, margins and the perceived strength of their future growth trajectory. [3] in 3-7 years). 23] A higher MRP increases the discount rate.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content