This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

per year Annual dividend on DIV's common shares to be increased 10% from 25 cents per share to 27.5 cents per share, effective July 1 , 2025 DIV's strong balance sheet enabled it to fund the Transaction without the need to raise equity 1. and the U.S. Consumer Price Index (" U.S. CPI ") + 1.5% cents per share to 27.5

share annual common dividend (13.5% expected dividend yield at $10.00/share) share annual common dividend (13.5% expected dividend yield at $10.00/share) share annual common dividend (13.5% expected dividend yield at $10.00/share) share annual common dividend, vi implying a peer-leading 13.5%

When I started offering financial modeling training , I never expected to get questions about a methodology like the Dividend Discount Model (DDM). Otherwise, the written version follows: Why Use a Dividend Discount Model? The main argument in favor of the DDM is that it best represents what happens in real life when you buy a stock.

billion of cross-shareholdings by the end of March 2027, Mizuho Financial Group expects to sell $1.9 Japanese companies historically have held onto cash rather than doing buybacks or paying out dividends,” he says, “so a lot of companies have a large stockpile of cash on their books. billion by March 2025.

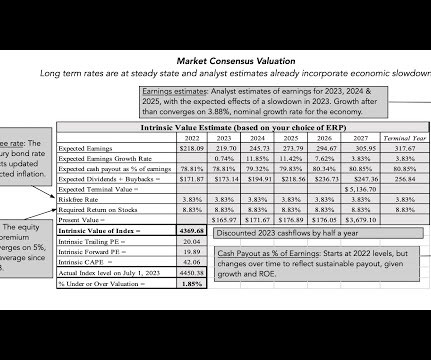

In my second data update post from the start of this year , I looked at US equities in 2022, with the S&P 500 down almost 20% during the year and the NASDAQ, overweighted in technology, feeling even more pain, down about a third, during the year. US Equities in 2023: Into the Weeds! that was lost last year.

Capital Power will finance the transaction using cash on hand and its credit facilities and will not need to access the equity markets to finance the transaction. On the strength of the contracted cash flows from this acquisition, we are increasing our annual dividend growth guidance to 6% through 2025 from the previous 5%.

Last year, the SEC issued guidance with respect to PvP disclosure requirements in the form of Compensation and Disclosure Interpretations and staff comment letters, including the following key items: Average compensation paid does not include unvested equity awards that vest upon retirement, even if the award holder is retirement-eligible.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content