Data Update 4 for 2024: Danger and Opportunity - Bringing Risk into the Equation!

Musings on Markets

JANUARY 28, 2024

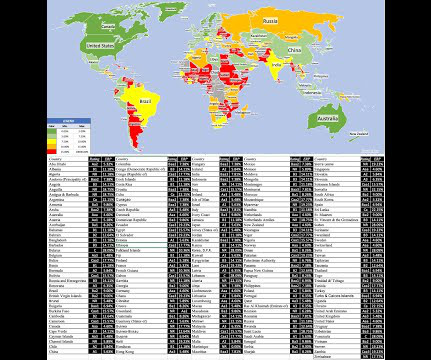

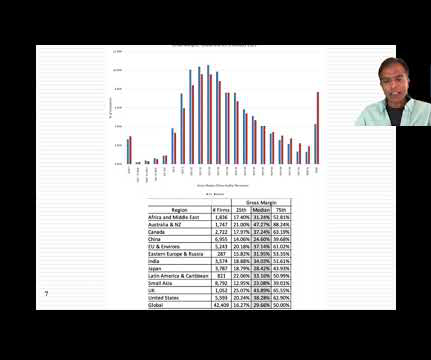

In my last data updates for this year, I looked first at how equity markets rebounded in 2023 , driven by a stronger-than-expected economy and inflation coming down, and then at how interest rates mirrored this rebound. Globally, health care has the highest percentage of money-losing companies and utilities have the lowest.

Let's personalize your content