This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Posted by the Harvard Law School Forum on Corporate Governance, on Friday, April 21, 2023 Editor's Note: This roundup contains a collection of the posts published on the Forum during the week of April 14-20, 2023. Cunningham, Jerry R. Marlatt and Felix R. Liekefett, Derek Zaba, and Eric S.

Posted by Jared Ellias (Harvard Law School) and Elisabeth De Fontenay (Duke University) , on Thursday, April 20, 2023 Editor's Note: Jared Ellias is a Professor of Law at Harvard Law School; Elisabeth de Fontenay is a Professor of Law at Duke University. Highly leveraged firms are now commonplace in many U.S. industries.

Widely held concerns about inflation, rising interest rates, and a possible recession combined to slow debtfinancing and deal activity in the first half of 2023. Borrowers deferred new debt deals, delayed planned refinancings, and paused major corporate transactions while waiting for interest rates to top out.

in a mix of equity and debtfinancing. In April 2022, HBox , raised a $700,000 seed funding round, led by Arali Ventures; another $1M in equity and debt in August of 2022, and, most recently, $400,000 in non-dilutive financing from Lighter Capital in early 2023. HBox has raised $2.1M

By the end of 2022, add-on acquisitions represented more than 76% of all private-equity-backed buyouts, which was a significant increase compared to a decade earlier. The percentage of add-ons dipped by 1% in 2023 — a year when volume and value of buyouts dropped significantly — and reached 76% in the first three months of 2024.

Over recent decades, and especially since the 2007-2008 global financial crisis (GFC), the corporate finance markets have changed considerably. First, there is more corporate debt now than ever. 2023 has recorded the two biggest private credit deals to date: $4.8 billion financing for Finastra and €4.5

Here are some key takeaways in the state of the market for IT services firms for 2023 and beyond : Demand is there but buyers are nervous. Private equity interest in buying tech firms hasn’t waned much. Private equity interest in buying tech firms hasn’t waned much.

trillion globally in 2023. Debtfinancing is particularly important for M&A because interest payments are deductible. However, interest limitation rules reduce their deductibility, raising the cost of debtfinancing and acquisitions. Finally, we investigate how interest limitations affect the quality of deals.

Since the global financial crisis of 2007-2008, the corporate finance markets have been dramatically transformed. Most notable has been the rise of non-traditional providers of debtfinance such as private credit funds, which now aggressively compete with traditional finance providers like commercial banks.

Castle Creek”), the buyer, and Paragon Biosciences, LLC (“Paragon”), the buyer’s private equity sponsor. In fact, one such Castle Creek debtfinancing document, a February 2020 loan agreement, did not permit Castle Creek to redeem its equity securities. to Castle Creek for cash and Castle Creek preferred stock.

28, 2023 (GLOBE NEWSWIRE) -- Methode Electronics, Inc. per share, for a total equity value of approximately EUR 132 million. per share, for a total equity value of approximately EUR 132 million. Methode expects to fund the purchase with a combination of cash on hand and debtfinancing under its existing credit facility.

There are two main categories of convertible instrument: Convertible Notes, a form of debt with interest payments until the point of conversion, and SAFEs which are quite literally simple agreements for future equity. A valuation cap is a ceiling on the price at which the investment will convert to equity. What is a cap?

CHATSWORTH, CA, June 15, 2023 (GLOBE NEWSWIRE) -- via NewMediaWire – Cavitation Technologies, Inc.("CTi" Eagle Ford owns approximately 180 acres of land near San Antonio and a producer of silica sand which is an essential component used in fracking operations in the oil and gas extraction industry.

DEBRA Proposal (« Debt-Equity Bias Reduction Allowance). In early May, the European Commission unveiled its proposal for a "DEBRA" (Debt-equity bias reduction allowance) Directive, aimed at encouraging companies to finance their investments with equity and capital contributions, instead of resorting to loans (bank or other).

DBS Best Bank for Sustainable Finance Best Bank for ESG-Related Loans Best Bank for Transition/Sustainability-Linked Loans DBS portfolio of sustainable finance products is vast, ranging from green loans and sustainability-linked loans to social loans and green trade finance.

Highlights: Outbrain will acquire Teads in an approximately $1 billion transaction, consisting of $725 million upfront cash and $25 million deferred cash, 35 million shares of common stock of Outbrain, and $105 million of convertible preferred equity. subject to customary funding conditions. The initial conversion price is $10.00

debt capital markets facilitate 75 percent of debtfinancing of non-financial corporations. 13] Transaction volume in listed equities has doubled in the last five years and tripled in the last 17 years. [14] at the end of FY 2023, resulting in approximately $14 million per year in savings. Further, U.S.

times estimated 2023 adjusted EBITDA multiple. Fully cash and debt-financed transaction; expect pro forma year-end 2022 leverage ratio around 3.5 We congratulate Mike Latchem and the entire Lucid team on today's milestone," said Baran Tekkora, a Partner at Riverstone and Co-Head of Private Equity.

On October 27, 2023, the UK’s Panel on Takeovers and Mergers (the “ Panel ”) published the results of a consultation started in May 2023 to review the City Code on Takeovers and Mergers (the “ Code ”), together with proposed amendments to the Code. The amendments to the Code will take effect from December 11, 2023.

This post takes a deeper dive into what we see as the pivotal events and deals that propelled the life sciences industry in 2022, and our view on what to expect looking ahead to 2023. While parties may opt to test these new theories in court, companies should be ready for extended review periods and a skeptical FTC.

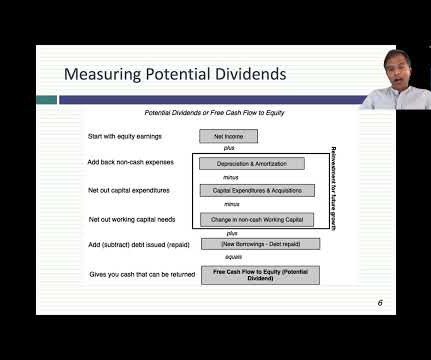

This is the last of my data update posts for 2023, and in this one, I will focus on dividends and buybacks, perhaps the most most misunderstood and misplayed element of corporate finance. To illustrate the heat that buybacks evoke, consider two stories in the last two weeks where they have been in the news.

Cross-border M&A activity in 2023 was impacted by heightened geopolitical conflicts, high inflation and interest rates, and increased regulatory pressures as the global economy remained clouded by looming recession fears. Deal financing became more difficult and expensive, placing more emphasis on alternative funding and value creation.

In support of that objective, in August 2023, President Biden issued EO 14105. [5] person’s direct or indirect: Acquisition of an equity interest or contingent equity interest; Certain debtfinancing that affords or will afford the U.S. That failure, however, spurred support for executive action. 850.202(a)(1).

However, deal activity fizzled in the second half of 2022, as high inflation, aggressive anti-inflation monetary policies, geopolitical instability, assertive antitrust regulators and tightening financing markets depressed target valuations, reduced strategic acquirer confidence and sidelined private equity sponsor buyers. trillion. [2]

Market participants entered the year hoping for a robust revival in M&A, IPO, and debtfinancing activities. After a dip in 2023, M&A activity showed signs of recovery in 2024. Over the previous 24 months, private equity firms sought bankers to handle divestituresto a corporate or maybe another firm like their own.

Under the revised terms, there is no deferred cash payment or convertible preferred equity component. The revised terms have meaningfully reduced the level of required debtfinancing and simplified the transaction structure. subject to customary funding conditions.

After a rough 2023 , tech M&A in 2024 was slow to start but ended the year strong, with deal values up 32% from 2023 , well outpacing the overall M&A markets 10% growth in 2024. As a result, even as aggregate tech deal values increased year over year, overall deal volume was at an eight-year low and down 14% from 2023.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content