This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Staying with the safety theme, I looked at US companies, broken down by debt burden (measured as debt to EBITDA): On this dimension, the numbers actually push against the flight to safety hypothesis, since the companies with the least debt performed worse than those with the most debt.

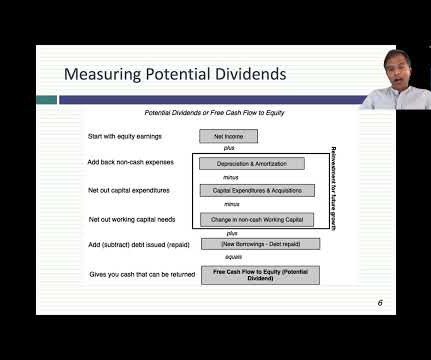

I have also developed a practice in the last decade of spending much of January exploring what the data tells us, and does not tell us, about the investing, financing and dividend choices that companies made during the most recent year. Dividends and Potential Dividends (FCFE) 1. Dividend yield & payout 3. Buybacks 2.

Even when you are successful in dissuading these companies from "bad" investments, but may not be able to stop them from returning the cash to shareholders as dividends and buybacks, rather than making "good" investments. trillion of cumulated enterprise value at fossil fuel companies. in the 1998-2010 time period to 5.95

The company already paid over CHF 100 million in settlement in this matter in 2020. . ABB performed particularly well in the COVID years 2020-2021, almost doubling its share price during this period. At this level the dividend yield is 2.8%. . IPO of E-Mobility Division. billion using a Cost of Equity of 7.1%.

The company already paid over CHF 100 million in settlement in this matter in 2020. . ABB performed particularly well in the COVID years 2020-2021, almost doubling its share price during this period. At this level the dividend yield is 2.8%. . IPO of E-Mobility Division. billion using a Cost of Equity of 7.1%.

net principal debt-to-annualized EBITDA ratio for 4Q‘22 (vs. per share cash dividend paid _ (1) A reconciliation of GAAP net income to Funds From Operations (FFO) is provided at the end of this press release. Additionally, ROIC's net principal debt-to-annualized EBITDA ratio for the fourth quarter of 2022 was 6.6

Activist Directors – Determinants Our research shows that activists are more likely to demand or acquire board representation if the firm has higher levels of institutional ownership, a smaller market capitalization, worse stock market performance, and, in particular, lower dividend payouts.

Your answer to that question will determine not just how you approach running the business, but also the details of how you pick investments, choose a financing mix and decide how much to return to shareholders, as dividend or buybacks. Does profitability vary across the globe?

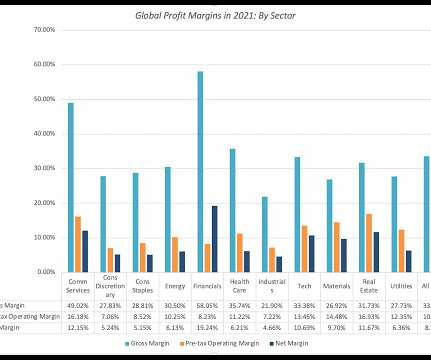

When profits are scaled to revenues, you get margins, and as with absolute earnings, margins come in various forms, as can be seen below: In addition to margins based upon income measures (gross, operating, after-tax operating and net), there are other margin variations, with EBITDA and after-tax operating margins coming into play.

The Transaction implies a multiple of less than 9x the projected forward Adjusted EBITDA and is immediately accretive, with DCF per share accretion in the mid-teens 4 , 5 , 6. The Terminal was officially placed in-service and loaded its first vessel in July 2020. million barrels of crude oil across 20 tanks.

Q1 2022 consolidated Adjusted EBITDA (as defined and reconciled below) of $87.0 The effect of the series of transactions in the last couple of quarters as well as continued focus on operational cost resulted in sequential Adjusted EBITDA 8% greater than Q4 2021. Adjusted EBITDA. Equity Method Investment EBITDA.

If your investment thesis is “undervalued industrial companies with between $5 and $15 million in EBITDA,” try again. At an average 10x EBITDA multiple, each company will have ~$5 million in EBITDA, putting you in “small / lower-middle-market” territory. A proven strategy in a specific , differentiated niche.

Combined Company targeting a low teen Adjusted EBITDA CAGR through 2023 from a 2021 base of $305 million 1. billion of Revenue and $305 million of Adjusted EBITDA in 2021 4. Combined Company Adjusted EBITDA. ($ in millions). Pro forma for the merger, Leonardo SpA and RADA shareholders will own approximately 80.5% 2,764. . .

This is the last of my data update posts for 2023, and in this one, I will focus on dividends and buybacks, perhaps the most most misunderstood and misplayed element of corporate finance. Viewed in that context, dividends as just as integral to a business, as the investing and financing decisions.

A good example is the 2020 – 2021 period, when SPAC activity went vertical, and plenty of renewable energy companies used SPACs to go public. If you look at the presentations and valuations below, you will still see standard valuation multiples like TEV / Revenue, TEV / EBITDA, and P / E.

Venture capitalist, raised on a diet of big stories and total addressable markets has little in common with bankers, trained to think in terms of EV to EBITDA multiples and accounting ROIC, and when put in a room together, it should come as no surprise that they find each other's language indecipherable.

In the last two decades, I have seen free cash flow measures stretched to cover adjusted EBITDA, where stock-based compensation is added back to EBITDA, and with WeWork, to community-adjusted EBITDA, where almost all expenses get added back to get to the adjusted value.

Performance and Valuations – PE and VC funds raised in the 2011 – 2020 period have performed decently over the past few years (median IRRs of 15 – 20%), but growth equity has been lower, with a median closer to 10%, likely because there was a much bigger valuation reset in the late-stage funding market and a big drop in exits.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content