This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The core idea behind relative valuation is to estimate a company’s value by comparing it to similar companies based on how the market prices their financial metrics. EV/EBITDA is a widely used multiple in this relative valuation approach. What is EV/EBITDA? Breaking down the multiple What is EBITDA?

Not surprisingly, the company listings are across the world, and I look at the breakdown of companies, by number and market cap, by geography: As you can see, the market cap of US companies at the start of 2025 accounted for roughly 49% of the market cap of global stocks, up from 44% at the start of 2024 and 42% at the start of 2023.

Historical Data: 1930-2019 To see how this framework works in practice, let's start by looking at the performance of US stocks, across the decades, and look at the returns on stocks, broadly categorized based on marketcapitalization and price to book ratios.

By analyzing factors like the price-to-earnings (P/E) ratio, price-to-book (P/B) ratio, and enterprise value-to-EBITDA (EV/EBITDA) ratio, companies can determine if their shares are undervalued or overvalued compared to peers. Dividend Discount Model DDM estimates the present value of expected future dividends from owning a stock.

I have also developed a practice in the last decade of spending much of January exploring what the data tells us, and does not tell us, about the investing, financing and dividend choices that companies made during the most recent year. Dividends and Potential Dividends (FCFE) 1. Return on (invested) capital 2.

Even when you are successful in dissuading these companies from "bad" investments, but may not be able to stop them from returning the cash to shareholders as dividends and buybacks, rather than making "good" investments. in the 1998-2010 time period to 5.95 in the 2011-2023 time period.

In percentage terms, energy stocks have lost the most in value, with marketcapitalizations dropping by 14.2%, dragged down by declining oil prices. There was undoubtedly some panic selling on Friday, but the flight to safety, whether it be in moving into treasuries or high dividend paying stocks, was muted.

It sustains its FY 2023 production and capital spending outlook. Based on the first-quarter financial performance, Devon declared a fixed-plus-variable dividend of $0.72 Share Price Performance The company has a marketcapitalization of more than $32 billion, however, its share price is still down roughly 30% from highs set last year.

The income-based approach determines a company’s value by assessing its anticipated future income-generating potential, employing methodologies such as Discounted Cash Flow (DCF) Analysis, Capitalization of Earnings, the Income Multiplier Method, Dividend Discount Model (DDM), and Earnings-Based Valuation.

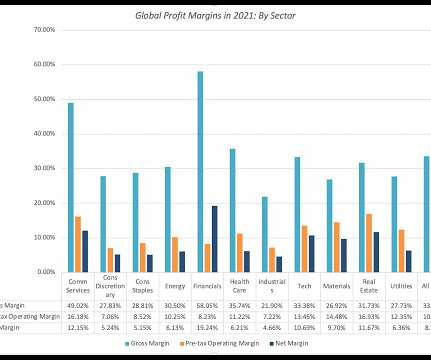

Thus, without a sense of what comprises a high or low profit margin for a firm, or what the cost of capital is for the typical company, it is easy to create "fairy tale" valuations and analyses. Data universe : In my sample, I include all publicly traded firms with marketcapitalizations that exceed zero, traded anywhere in the world.

Additionally, NVIDIA returned USD 99 million in cash dividends to shareholders, exemplifying its financial robustness. Emphasizing the company’s robust market performance, Nvidia’s marketcapitalization has hit the USD 1 trillion milestone, joining the elite league of tech behemoths such as Apple and Amazon.

Currently the company is trading at CHF 30 per share with a marketcapitalization of CHF 56.1 At this level the dividend yield is 2.8%. . The Trading Comparables analysis resulted in a valuation range of CHF 47 to 83 billion, by applying the observed trading multiples EV/EBITDA, EV/EBIT and P/E. Valutico Analysis.

Currently the company is trading at CHF 30 per share with a marketcapitalization of CHF 56.1 At this level the dividend yield is 2.8%. . The Trading Comparables analysis resulted in a valuation range of CHF 47 to 83 billion, by applying the observed trading multiples EV/EBITDA, EV/EBIT and P/E. Valutico Analysis.

Furthermore, there are concerns regarding IBM’s uncertain dividend and recent acquisition spree. The Trading Comparables analysis resulted in a valuation range of USD 106 billion to USD 235 billion by applying the observed trading multiples EV/Sales, EV/EBITDA, EV/EBIT and P/E. and Alphabet Inc.

Furthermore, the company increased dividends by 10% and announced that it will buy back GBP 2.3 (USD The Trading Comparables analysis resulted in a valuation range of GBP 98 (USD 199) billion to GBP 137 (USD 166) billion by applying the observed trading multiples EV/EBITDA, EV/EBIT, P/E and P/B. billion worth of shares.

This strong financial performance is also reflected in the stock market as TotalEnergies is currently trading at €57 per share, which is a year-on-year increase of roughly 30%. This strong share price performance was further bolstered by an average gross annual dividend yield of roughly 6% over the past 10 years.

This strong financial performance is also reflected in the stock market as TotalEnergies is currently trading at €57 per share, which is a year-on-year increase of roughly 30%. This strong share price performance was further bolstered by an average gross annual dividend yield of roughly 6% over the past 10 years.

Activist Directors – Determinants Our research shows that activists are more likely to demand or acquire board representation if the firm has higher levels of institutional ownership, a smaller marketcapitalization, worse stock market performance, and, in particular, lower dividend payouts.

In this post, I want to focus on that point, starting with a discussion of why stories matter to investors and traders and the story that propelled the company to a trillion-dollar marketcapitalization not that long ago. billion in revenues in 2021.

When profits are scaled to revenues, you get margins, and as with absolute earnings, margins come in various forms, as can be seen below: In addition to margins based upon income measures (gross, operating, after-tax operating and net), there are other margin variations, with EBITDA and after-tax operating margins coming into play.

He acquires a literal “stock certificate” representing a very, very small but pro-rata claim on all the cash flows of the company, and is the pro-rata beneficiary of any future dividends or stock repurchases. The current market price of $210 per share represents the current consensus pricing (per share) for all of META in the market today.

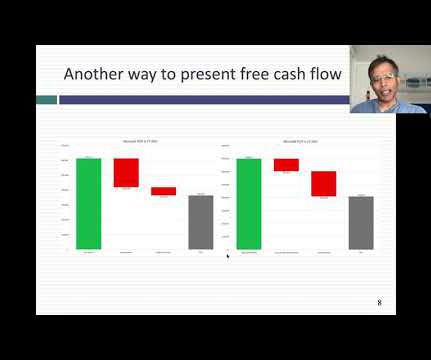

In the last two decades, I have seen free cash flow measures stretched to cover adjusted EBITDA, where stock-based compensation is added back to EBITDA, and with WeWork, to community-adjusted EBITDA, where almost all expenses get added back to get to the adjusted value.

Given the historical roots of the biggest Indian family groups, the Adani Group has been a recent entrant, not making the top ten list (in terms of either operating metrics like revenues or market-based numbers like marketcapitalization or enterprise value) as recently as ten years ago, and barely making the top ten list five or six years ago.

With individual stocks, that danger gets multiplied, with investors buying stocks that are being sold off to for legitimate reasons (a broken business model, dysfunctional management, financial distress) and waiting for a market correction that never comes.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content