Data Update 4 for 2022: Risk = Danger + Opportunity!

Musings on Markets

FEBRUARY 8, 2022

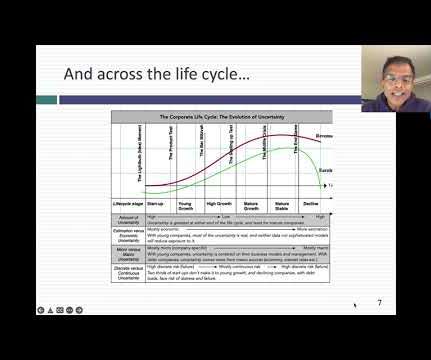

Relative Risk Measures Before we embark on how to measure relative risk, where there can be substantial disagreement, let me start with a statement on which there should be agreement. At the start of 2022, the ten sectors (US) with the highest and lowest relative risk (unlettered betas), are shown below.

Let's personalize your content