This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

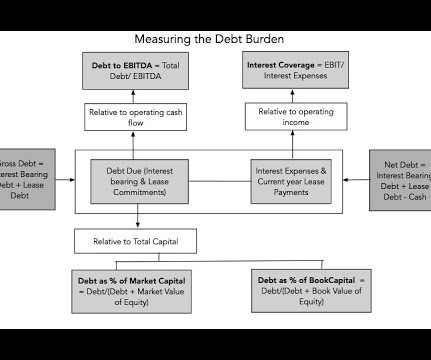

It was only in 2019 that the accounting rule-writers (IFRS and GAAP) finally did the right thing, albeit with a myriad of rules and exceptions. That is where the cost of capital, the Swiss Army Knife of finance that I wrote about in my sixth data update update , comes into play as a debt optimizing tool.

If a large shareholder or a group of investors becomes concerned with the firm’s operations and management, and takes legal steps to assert their claims, it may affect a firm’s outlook, competitive position, its riskpremium, and hence discounted value. This post is based on their recent paper.

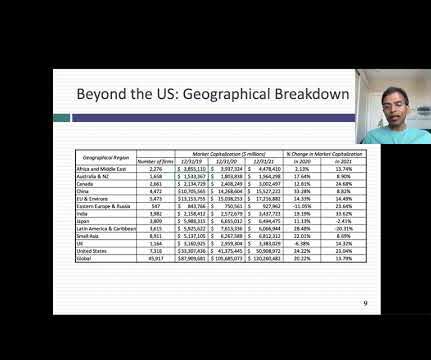

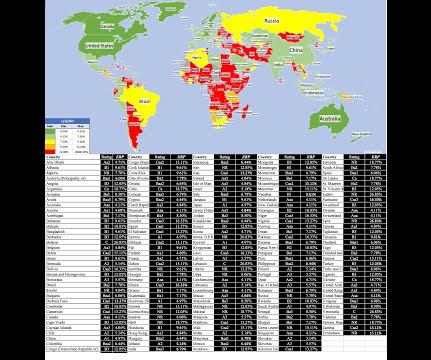

trillion on their market capitalization at the end of 2019. Historical Equity RiskPremium The conventional wisdom, at least as taught in business schools and practiced by appraisers, is that the only practice way to estimate equity riskpremiums for the future is to use equity riskpremiums earned in the past.

I have also developed a practice in the last decade of spending much of January exploring what the data tells us, and does not tell us, about the investing, financing and dividend choices that companies made during the most recent year. Beta & Risk 1. Equity RiskPremiums 2. Financing Flows 5. Debt Details 1.

The cash flows from an entire business include inflows and outflows from investing, financing, and operating activities (such as sales, collections on receivables, expenditures, and settling accounts payable). The adjustment added to the risk-free rate to arrive at the risk-adjusted rate is often referred to as the “riskpremium.”

For instance, I have always computed the present value of lease commitments in future years and treated that value as debt, a practice that IFRS and GAAP have adopted in 2019, but that computation requires explicit disclosures of lease commitments in future years. Macro Data I do not report much macroeconomic data for two reasons.

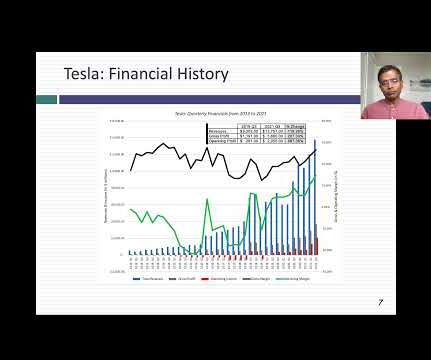

My two most recent valuations were in June 2019 and January 2020, and I am going to go back to them, not just because they are recent, but because they led to investment decisions on my part. In June 2019, Tesla had hit a rough spot, partly due to concerns about production bottlenecks and debt, and partly due to self inflicted wounds.

Kevin holds an MBA in finance from Georgia State University and a Bachelors in Chemical Engineering from the Georgia Institute of Technology. Finance Professor | Pepperdine Graziadio Business School Craig R. Everett is a finance professor at the Pepperdine Graziadio Business School. a Software as a Service company.

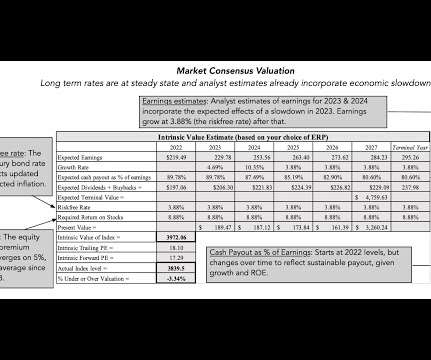

Note, though, that 2021 is the third consecutive year of very good returns on the index, with 2019 delivering 31.21%, and 2020 generating 18.02%, and that the cumulative return over the three years (2019-21) is 98.95%. the 2019-21 time period would rank 8th on the list of 92 3-year time periods.

After the 2008 market crisis, I resolved that I would be far more organized in my assessments and updating of equity riskpremiums, in the United States and abroad, as I looked at the damage that can be inflicted on intrinsic value by significant shifts in riskpremiums, i.e., my definition of a crisis.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content