This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

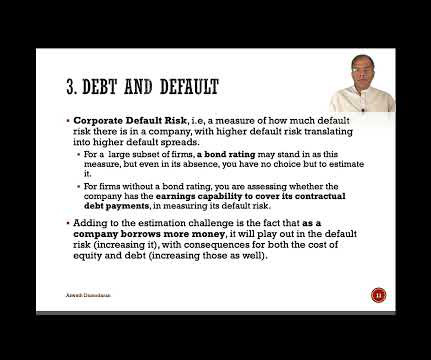

In the first five posts, I have looked at the macro numbers that drive global markets, from interest rates to riskpremiums, but it is not my preferred habitat. The second set of inputs are prices of risk, in both the equity and debt markets, with the former measured by equity riskpremiums , and the latter by default spreads.

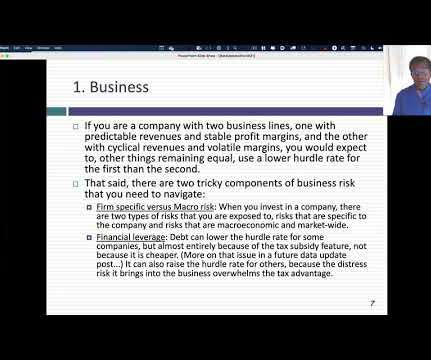

In this post, I will start by looking at the role that hurdle rates play in running a business, with the consequences of setting them too high or too low, and then look at the fundamentals that should cause hurdle rates to vary across companies.

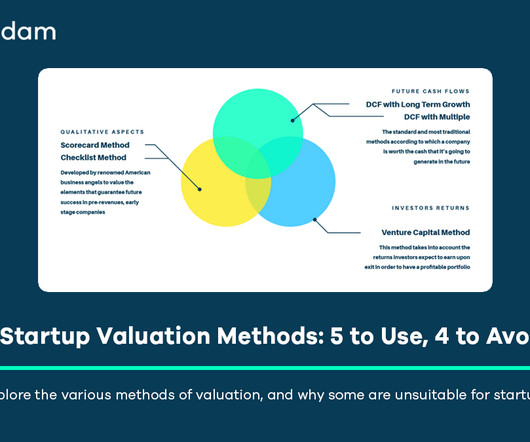

Instead of comparing to an average, it typically starts with a maximum potential pre-money valuation deemed achievable for a startup of that type in its region. Unlike the Scorecard, it doesn’t explicitly benchmark against competitors but focuses on the startup’s internal milestones and risk mitigation.

Third, by making investing a choice between good (higher returns) and bad (higher risk), a message is sent, perhaps unwittingly, that risk is something to be avoided or hedged. micro uncertainties, into discount rates, and in the process, they end up incorporating risk that investors can eliminate, often at no cost.

2] Startups typically lack significant historical financial data, often operate with negative profits initially, rely heavily on private equity or venture capital rather than traditional bank loans, and face a much higher risk of failure. [1] This premium rises when perceived marketrisk increases. [27] 2] [15] [17].

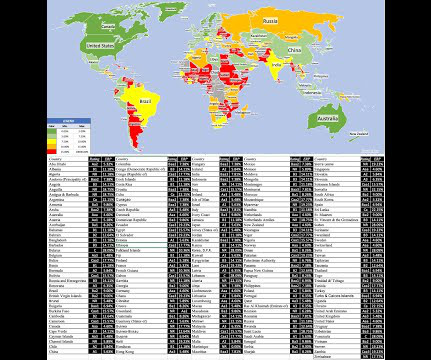

23] , [24] , [25] This average serves as a starting point, which is then adjusted upwards or downwards based on the specific startup’s relative strengths and weaknesses across several key criteria. [21] 23] Equidam uses country-specific risk-free rates (10-year government bonds) and marketriskpremiums (sourced from Damodaran). [23]

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content