Methods of Business Valuation by Their Profitability

Equilest

MARCH 17, 2022

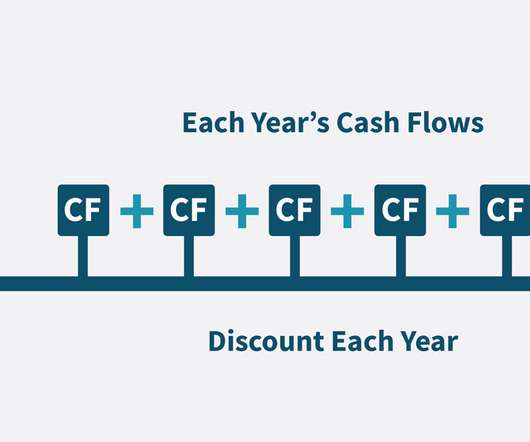

We note that the higher the expected rate (in other words, the greater the risk is perceived as necessary, to the point of requiring a substantial "risk premium"), the lower the multiple that will apply and therefore the lower valuation: we buy cheaper which is less safe. Net Operating Surplus Multiples (ENE or EBIT).

Let's personalize your content