This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Equity is cheaper than debt: There are businesspeople (including some CFOs) who argue that debt is cheaper than equity, basing that conclusion on a comparison of the explicit costs associated with each interest payments on debt and dividends on equity.

The first is the role that cash holdings play in a business , an extension of the dividend policy question, with an examination of why businesses often should not pay out what they have available to shareholders. In this post, I will bring together two disparate and very different topics that I have written about in the past.

Massive dividend yield secured by strong cash generation. Cash machine ensures consistent massive dividend yield. It consistently delivered strong FCFF that were more than sufficient to cover high dividends. The FCF yield shows ROEC’s dividend-paying potential. LG) shift to OLED technology.

Value play with strong dividend growth potential. However, increased CAPEX for capacity expansion and battery development lead to increase in net fixed assets again. In 2020, its net-debt to equity ratio stood at 0.9x. I expect dividend yield over the near-term to range between 2.5-3.5%. Ratios – Volvo.

The income-based approach determines a company’s value by assessing its anticipated future income-generating potential, employing methodologies such as Discounted Cash Flow (DCF) Analysis, Capitalization of Earnings, the Income Multiplier Method, Dividend Discount Model (DDM), and Earnings-Based Valuation.

billion, and the assumption of netdebt of approximately $600 million, subject to required court, LifeWorks shareholder, stock exchange and regulatory approvals (the " Transaction "). Within TELUS Health, we are leveraging the power of our globally leading technology and our caring culture, to build a healthier future.

Just as important, this combination results in a financially stronger company with no netdebt, significant cash on the balance sheet and the size and scale to better fund and execute on a robust set of organic opportunities while delivering accretive long-term growth objectives.

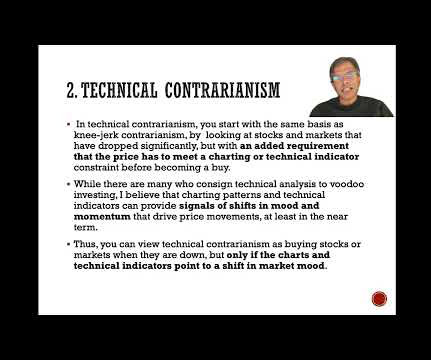

Technical Contrarianism In technical contrarianism, you start with the same basis as knee-jerk contrarianism, by looking at stocks and markets that have dropped significantly, but with an added requirement that the price has to meet a charting or technical indicator constraint before becoming a buy.

billion of netdebt. The transaction is projected to result in a pro forma net leverage ratio at closing of approximately 2.3x, well within the company's target range of 1.5-2.5x. Upon closing, the company intends to reduce its leverage with a goal of reaching net-debt to EBITDA of approximately 2.0x

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content