This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

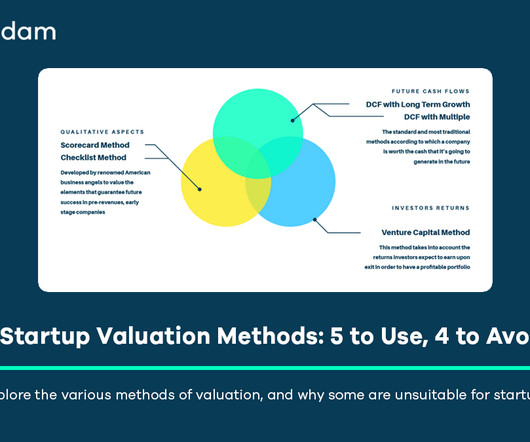

Comparable Transactions (as a Primary Method): This method, often referred to as “comps,” involves applying valuation multiples (e.g., This incorporates the risk-free rate, a market riskpremium specific to the company’s country, and Beta ($beta$).

The court refused to put any weight on petitioners’ comparable companies analysis, finding that the comp set diverged too much from SWS in terms of size, business lines, and performance to be meaningful. The court undertook its own DCF analysis, on which it relied exclusively.

the multiple based or ‘ comps ’ (comparable company analysis) approach. Rf = Risk-free Rate. Rm – Rf) = Equity Market RiskPremium. Cp = Cost of Equity Premium. The first is 1. the intrinsic or income-based approach, also known as an entity approach, then there is also 2. Ce = Cost of Equity. B = Beta. (Rm

Updated Market Conditions Inputs – Risk-free rates: Now 4-5% vs. near-zero during ZIRP – Market riskpremiums: Adjusted for current volatility and country-specific factors – Survival rates: Updated data reflecting current market conditions 2. Here’s how Equidam approaches this: 1.

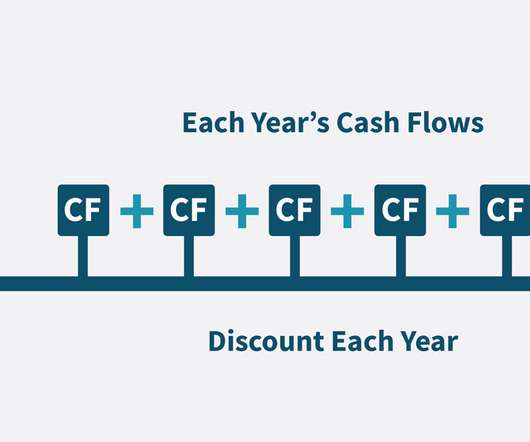

Discount Rates / RiskPremiums: The discount rate used in DCF analysis (often the WACC) incorporates elements sensitive to market conditions. [21] 21] [22] [24] [27] The cost of equity component includes the market riskpremium the excess return investors expect for investing in the broader market over a risk-free rate.

10] , [23] , [2] Discount Rate: The rate used to discount future cash flows is typically the cost of equity, calculated via the Capital Asset Pricing Model (CAPM): Cost of Equity = Risk-Free Rate + Beta * Market RiskPremium. [23] 23] Risk-Free Rate: Tied to government bond yields (e.g.,

That is finally starting to stabilize as we’ve lapped higher rates and have easier comps there. There are certain sectors that we think are offering better risk/reward. So, credit spreads have gotten so tight and so compressed that there’s not much of a cyclical riskpremium.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content