This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In the world of finance and investing, the concept of beta plays a vital role in assessing an investment’s risk and volatility. Whether you’re a seasoned investor or new to the market, understanding beta can empower you to make informed decisions. What is beta and how do you calculate beta?

When an investor buys a particular security, they consider the risk of that security relative to the riskiness of the overall market and adjust the equity risk premium up or down by using Beta. Investments are exposed to two types of risk: systematic and unsystematic. beta of a stock). E(r) = Rf + ??(Rm

To refine the selection of the discount rate, it’s important to draw on inputs from credible sources regarding economic, industry and company specificrisk factors. It is often referred to as the “marketrisk premium.” Small-cap stocks are often considered riskier and may command a size premium.

This incorporates the risk-free rate, a marketrisk premium specific to the company’s country, and Beta ($beta$). Beta measures the volatility of the company relative to the market. This bridges the gap between theoretical valuation principles and the specificrisk profile of startups.

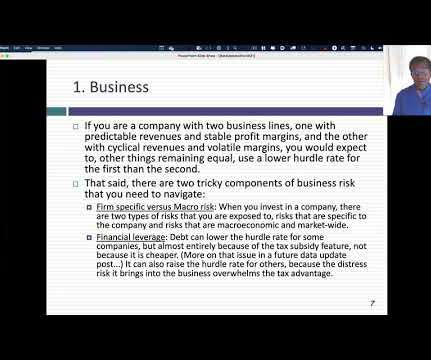

If you put all your money in one or the other of these companies, you are exposed to all these risks, but if you spread your bets across a dozen or more companies, you will find that company-specificrisk gets averaged out. More on that issue in a future data update post.) Cost of equity in US $ for German project = 1% + 1.1

This calibration directly impacts expected returns, required ROI, survival rates, and appropriate liquidity discounts, significantly refining risk assessment. Country: Argentina Operating from Argentina influences extrinsic risk factors due to regional economic conditions, market size, regulatory environment, and currency stability.

10] , [23] , [2] Discount Rate: The rate used to discount future cash flows is typically the cost of equity, calculated via the Capital Asset Pricing Model (CAPM): Cost of Equity = Risk-Free Rate + Beta * MarketRisk Premium. [23] 23] Risk-Free Rate: Tied to government bond yields (e.g.,

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content