The Dividend Discount Model (DDM): The Black Sheep of Valuation?

Brian DeChesare

MAY 3, 2023

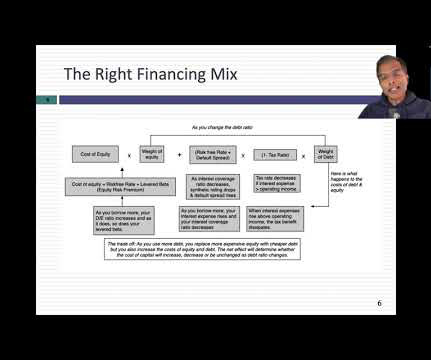

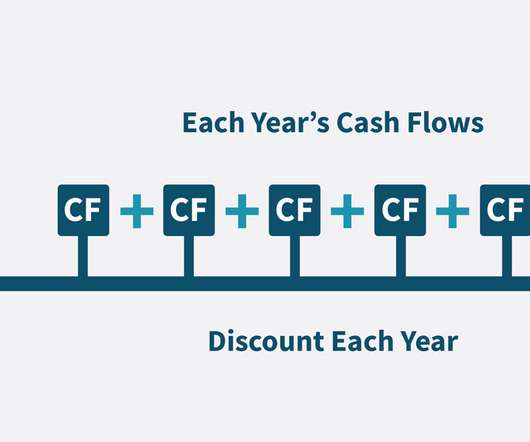

Step 4: Discount the Dividends and Terminal Value to Present Value and Add Them This is like the final step of a DCF, but you use the Cost of Equity since the Dividend Discount Model is based on Equity Value, not Enterprise Value. DTM’s Levered Beta at this time was only 0.80, but I increased it to 1.00

Let's personalize your content