This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Valuation as a Process, Not Just a Number A common misconception is that startup valuation aims to pinpoint a single, definitive “right” number representing the company’s price. This incorporates the risk-free rate, a market riskpremium specific to the company’s country, and Beta ($beta$).

Thus, as you peruse my historical data on implied equity riskpremiums or PE ratios for the S&P 500 over time, you may be tempted to compute averages and use them in your investment strategies, or use my industry averages for debt ratios and pricing multiples as the target for every company in the peer group, but you should hold back.

Investors all talk about risk, but there seems to be little consensus on what it is, how it should be measured, and how it plays out in the short and long term. In closing, I will talk about some of the more dangerous delusions that undercut good risk taking.

Capital Asset Pricing Model (CAPM): According to CAPM, the expected return on a stock has two main components: the risk-free rate and a riskpremium. The risk-free rate represents the return an investor can get without taking on any risk, typically derived from government bonds.

Definition of Capital Asset Pricing Model. It helps an investor understand what to expect to earn in relation to the risk-free rate and the market return. CAPM assumes that the minimum a rational investor would earn is the risk-free rate by buying the risk-free asset. beta of a stock). E(r) = Rf + ??(Rm

Definition of the Arbitrage Pricing Theory. It is a model based on the linear relationship between an asset’s expected risk and return. The return on assets is determined by systematic factors such as changes in inflation , riskpremiums, interest rates, etc. What Impacts the Arbitrage Pricing Theory? ER(x) = Rf + ??1

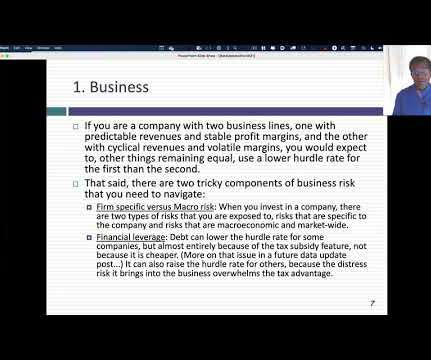

There are multiple definitions that you will see offered, from it being the cost of raising capital for that business to an opportunity cost , i.e., a return that you can make investing elsewhere, to a required return for investors in that business. What is a hurdle rate for a business? More on that issue in a future data update post.)

When valuing or analyzing a company, I find myself looking for and using macro data (riskpremiums, default spreads, tax rates) and industry-level data on profitability, risk and leverage. I do report on a few market-wide data items especially on riskpremiums for both equity and debt. Cost of Equity 1.

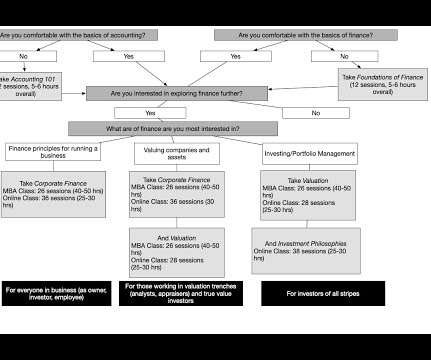

If it looks like I am over reaching, I start my corporate finance class with the simple proposition that any decision that involves money is a corporate finance decision, and by that definition everything that businesses do falls under its umbrella. The links to all of these classes are at the end of this post.

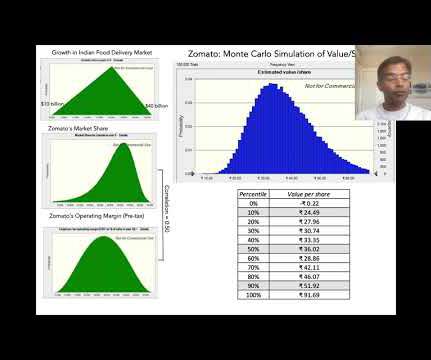

Raising or lowering the cost of capital has an effect on value, but changing my assumptions about riskpremiums, betas or debt ratios has a much smaller effect that changing assumptions that alter cash flows. The Zomato IPO clocks in at 420 pages , much of it designed to bore readers into submission.

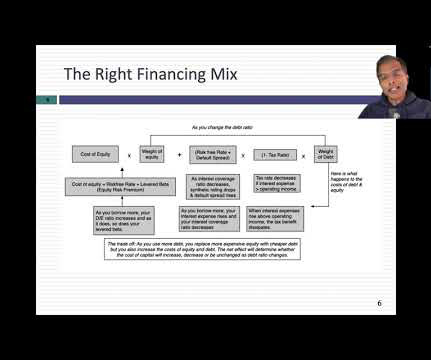

An Optimizing Tool In my second and third data posts for this year, I chronicled the effects of rising interest rates and riskpremiums on costs of equity and capital. In computing the latter, I used the current debt ratios for firms, but made no attempt to evaluate whether these mixes were "right" or not.

10] , [23] , [2] Discount Rate: The rate used to discount future cash flows is typically the cost of equity, calculated via the Capital Asset Pricing Model (CAPM): Cost of Equity = Risk-Free Rate + Beta * Market RiskPremium. [23] 23] Risk-Free Rate: Tied to government bond yields (e.g.,

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content