This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

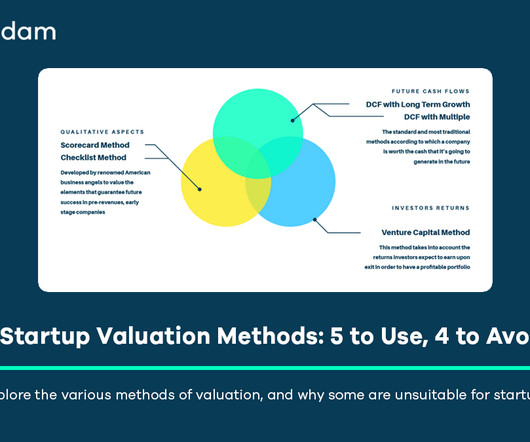

This approach encourages dialogue focused on the business fundamentals the team, the market opportunity, the product, the financial projections rather than anchoring the conversation to arbitrary figures potentially derived from selectively chosen, and often inappropriate, market comparisons.

In particular, the Terminal Growth Rate is used in a DCF analysis to help calculate the TerminalValue. The Terminal Growth Rate and the TerminalValue are important figures in valuations, because they usually represent a significant contributor to the final valuation estimate.

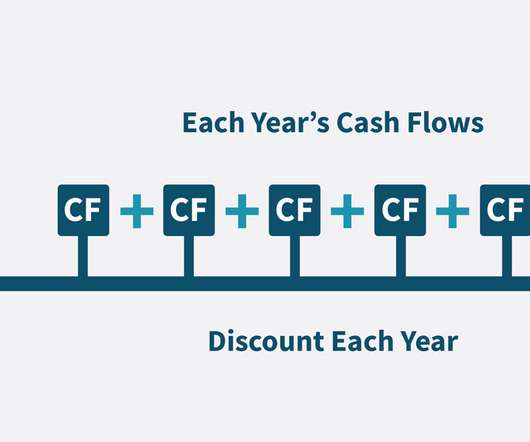

But here, we use what interest we could get from an alternative investment in the market, called the Market Rate. Discount Factor (using Market Rate: r=10%). But first, a quick aside, which you can feel free to skip if you want to jump ahead: Why Do We Use the Market Rate to Calculate the Discount Factor? You get: Year.

S ection 3: What Influence Do Markets Have on Startup Valuation? Valuing startups relies heavily on assumptions about future performance, interpretations of market trends, and the specific perspectives and risk appetites of the involved parties. [3] This exploration will cover: Section 1: What is Startup Valuation?

Communicating Future Potential Section 3: Riding the Waves: The Influence of Markets Section 4: The Goal of Valuation: Building Investor Confidence Section 5: The Founder’s Valuation Playbook Section 6: Bridging the Gap: Founder, Investor, and Advisor Perspectives Section 1: What is Startup Valuation? 11] [13] Internal/Compliance (e.g.,

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content