This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

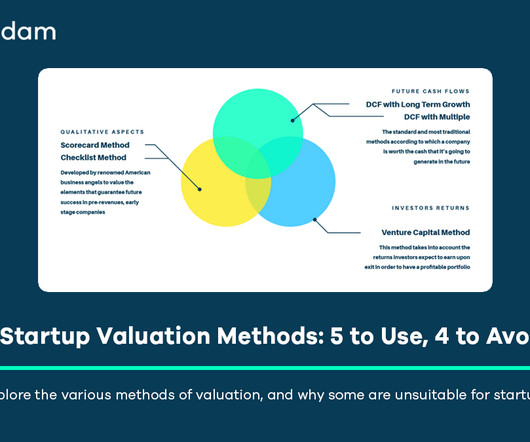

Their value proposition is typically rooted not in past performance but in future potential. Furthermore, any quantitative valuation method, particularly the Discounted Cash Flow (DCF) approach, is highly sensitive to the underlying assumptions about growth rates, discount rates, and terminalvalues.

To discover how blue sky valuation combined with the Discounted Cash Flow (DCF) method helps assess intangibleassets like brand equity, intellectual property, and goodwill. Defining "Blue Sky" in Valuation The term “blue sky” refers to the intangiblevalue of a business. Calculating terminalvalue.

Use DCF analysis to estimate the present value of future cash flows, considering growth rates, discount rates, and terminalvalues. Valuingintangibleassets, like intellectual property, is inherently subjective and variable. Finding comparable companies with similar models and prospects is a challenge.

Under the “Discounted Future Earnings” approach, the appraiser will estimate value primarily from future income probability, or forecasts, over a fixed period of time, to a terminalvalue, and discount this back to the present. This is generally preferred for fully operational companies with a lot of tangible assets.

Key methods include the Income Approach, which estimates future cash flows, the Market Approach, comparing with similar businesses, and the Asset Approach, valuing tangible and intangibleassets. Lastly, determining the continuity value (or terminalvalue) is a subjective process that often leads to disagreements.

Dive into the nuances of industry-specific multiples, grasp the challenges of valuingintangibleassets, and discover the evolving landscape of incorporating Environmental, Social, and Governance (ESG) factors into the valuation framework. Can TerminalValue be Negative? When Not to Use DCF in Valuation?

Since cash flow projections cannot be made indefinitely, a terminalvalue is often calculated to account for the value of cash flows extending beyond the forecast period. The terminalvalue can be estimated using the perpetuity growth model or the exit multiple approach.

The challenge with this approach when valuing SMEs is finding comparable businesses due to their unique characteristics. Asset-based Approach : This method functions like an inventory check, summing up a company’s tangible and intangibleassets and subtracting liabilities, resulting in the company’s net assetvalue.

10] , [23] , [2] Discount Rate: The rate used to discount future cash flows is typically the cost of equity, calculated via the Capital Asset Pricing Model (CAPM): Cost of Equity = Risk-Free Rate + Beta * Market Risk Premium. [23] 1] , [21] , [23] , [29] The terminalvalue is estimated by applying a relevant market multiple (e.g.,

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content