This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

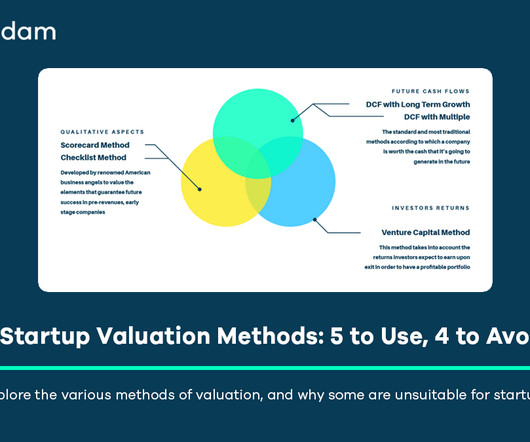

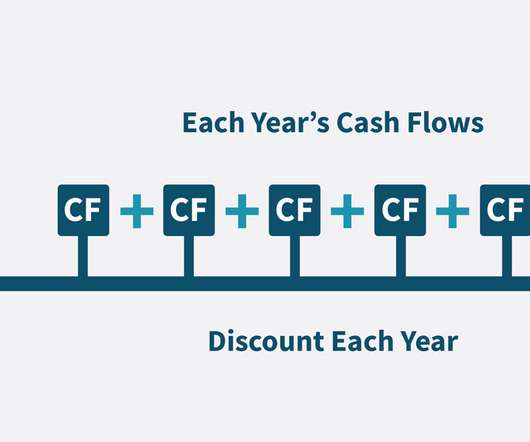

Furthermore, any quantitative valuation method, particularly the Discounted Cash Flow (DCF) approach, is highly sensitive to the underlying assumptions about growth rates, discount rates, and terminalvalues. The book value typically represents only a fraction of the perceived worth and fails entirely to account for future prospects.

the multiple based or ‘ comps ’ (comparable company analysis) approach. Well, the short answer is after that forecast period where we estimate each year’s cash flows then discount them, we add a single number at the end to account for all the theoretical years in the future, called the TerminalValue (TV). The first is 1.

Understanding the Concept: In essence, FCFF encapsulates the cash that can be distributed to both debt and equity holders after meeting operational needs and capital expenditures. The resulting value represents the cash available to all contributors of capital—both debt and equity. What is Free Cash Flow to Equity?

These methods provide a relative measure of a company’s value and are widely used due to their market-based nature. The most common market-based valuation methods are the Comparable Companies Analysis (Comps) and the Precedent Transactions Analysis. This high leverage is why it’s called a “leveraged” buyout.

It determines the price per share, dictating how much equity founders concede in exchange for the capital raised. [3] The formula is Present Value (Post-Money Valuation) = Potential Exit Value / (1 + Required ROI)^n , where ‘n’ is the number of years to exit. [8]

1] Unlike valuing established public companies with long track records and stable earnings, startup valuation operates in a realm of high uncertainty. [2] 1] Unlike valuing established public companies with long track records and stable earnings, startup valuation operates in a realm of high uncertainty. [2] 2] [15] [17].

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content