This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

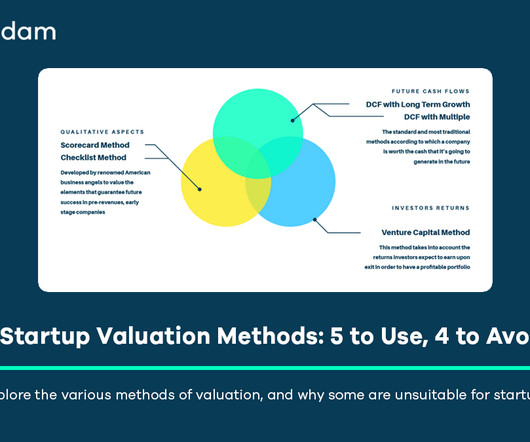

Valuation as a Process, Not Just a Number A common misconception is that startup valuation aims to pinpoint a single, definitive “right” number representing the company’s price. Comparable Transactions (as a Primary Method): This method, often referred to as “comps,” involves applying valuation multiples (e.g.,

Beta-Neutral Portfolios: For example, if the S&P 500 goes up or down by 5%, your team’s portfolio should move by ~0%. So, expect a lot of quarterly financial projections , quick public comps , and simple DCF models linked to specific catalysts. Do Multi-Manager Hedge Funds Deliver?

Fixed definitions are hard to come by, and the scattering of websites, scorecards, speeches, podcasts, and white papers that mention ESG in many different ways do not help. Adjustments to Beta can accomplish this. For example, in a recent valuation we completed, the mean unlevered Beta of a group of 10 comps was 0.58.

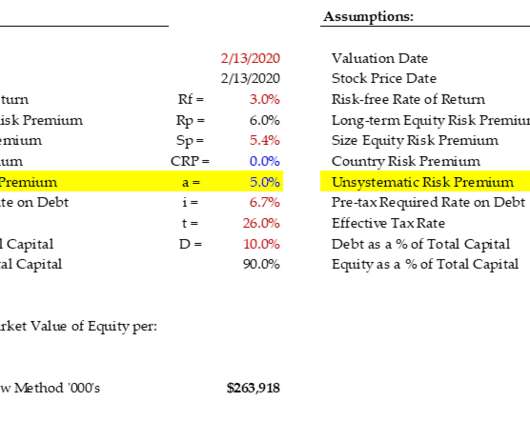

10] , [23] , [2] Discount Rate: The rate used to discount future cash flows is typically the cost of equity, calculated via the Capital Asset Pricing Model (CAPM): Cost of Equity = Risk-Free Rate + Beta * Market Risk Premium. [23] Equidam utilizes country-specific MRP data calculated by Professor Damodaran. [23]

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content