This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The One Big Beautiful Bill Act (the “OBBBA”) was signed into law on Friday, and, while not the paradigm shift of 2017’s Tax Cuts and Jobs Act (the “TCJA”), it introduces important changes affecting both domestic and cross-border transactions, many of which are effective for tax years beginning after December 31, 2025.

An interesting question, largely unanswered or answered incompletely, is whether the US tax code change in 2017 changed how much US companies borrowed, since the lowering of tax rates should have lowered the tax benefits of borrowing.

It will be a challenge for the company to drive its EBIT margin to the industry average of 7-9%. CAPEX is likely to stay much lower than 2017 to 2019 level. Tata has been among the worst profitable car companies in the past years. The company has relatively high leverage. Free cash flow – Tata Motors. Value estimate – Tata Motors.

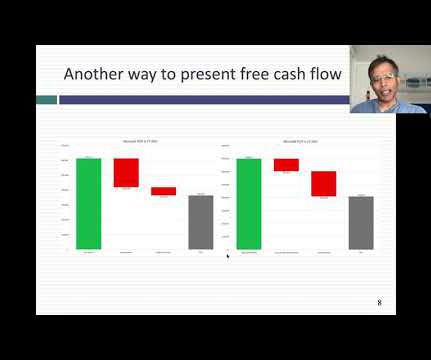

Thus, we start with operating income or earnings before interest and taxes (EBIT) replacing net income. (I In the Microsoft FCFF calculation, this would imply replacing the effective tax rate of 13.83% with an average effective tax rate of 22%, using the 2017-2021 time period, which would lower free cash flows to the firm.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content