Small and Medium-sized Enterprises (SMEs) are key players in driving economic growth, fostering innovation, and creating jobs. Recognized as firms with under 250 employees, their accurate valuation is highly important for many finance professionals. In this article, we’ll unravel how to value SMEs, including what you need to consider to do so accurately.

How do I value an SME? Valuing a Small and Medium-sized Enterprise (SME) involves assessing the company’s financial performance, assets, market position, and growth potential. Key methods include the Income Approach, which estimates future cash flows, the Market Approach, comparing with similar businesses, and the Asset Approach, valuing tangible and intangible assets. Since SMEs often have distinct characteristics like varying cash flows and limited resources, these factors must be carefully considered to arrive at an accurate valuation.

Key Takeaways:

- Valuing Small and Medium-sized Enterprises (SMEs) is crucial for various financial decisions like mergers and acquisitions, investments, and reporting. It determines the economic worth of a company and is essential for informed decision-making.

- SMEs have distinct challenges that impact their valuation, such as unpredictable cash flows, reliance on limited clients, and restricted access to capital. A tailored approach is needed to account for these complexities.

- Common steps in SME valuation include gathering financial data, understanding the industry, choosing a valuation method, and calculating the value using chosen methodology and financial data.

- The three main methods for SME valuation are the Income Approach (e.g. Discounted Cash Flow analysis), Market Approach (e.g. Comparable Companies Analysis), and Asset-based Approach (e.g. net asset value calculation).

- SME valuation also considers factors like owner dependence, client concentration, market position, competitive advantage, and the quality of financial statements.

- The Discounted Cash Flow (DCF) is a leading valuation method that calculates value based on future cash flows, considering time value of money. Free Cash Flow (FCF) and discount rate (often determined using CAPM) are crucial components of this approach.

- SMEs can present challenges with DCF due to limited historical financial data, unreliable information, inadequate financial forecasts, and difficulty in determining terminal value. Approximations, negotiations, and considering illiquidity premiums help mitigate these challenges.

- SME valuation involves understanding different valuation methods and their narratives, tailoring approaches to SME characteristics, and using various components to arrive at an accurate depiction of the business’s value.

What is the Basic Idea behind an SME Valuation?

In its essence, business valuation is the process of determining a company’s economic worth, crucial for various scenarios like mergers and acquisitions, investment analysis, capital budgeting, financial reporting, or even litigation matters.

Why Are SME Valuations So Unique and Challenging?

SMEs, with their unique structures, present specific challenges that can significantly influence their value. These challenges could be unpredictable cash flows, reliance on a limited client base, or restricted access to capital. Thus, SME valuation requires a customized approach, acknowledging these intricacies.

What are the Main Ways to Value an SME?

Broadly speaking, you can value an SME by using one of three methodological approaches.

One common approach is considering the profits it makes and the money it’s expected to make in the future. This is known as the Income Approach, the main method of which is known as a Discounted Cash Flow analysis, which we detail below.

Another approach is comparing it to similar businesses that have been sold recently, similar to how real estate is appraised. This is known as the Market Approach and a common method within this approach is called Comparable Companies Analysis, for example.

The third broad approach involves looking at the assets the SME possesses, like equipment and property, minus any debts it owes. This is known as the Asset Approach.

Sometimes, the business’s reputation or special qualities can also play a role in its value. Experts might even combine a few methods to get a more accurate valuation. One common way might be to run the DCF as the leading technique to value the company, but then support this by running a Comparable Companies Analysis as well.

As well as the three broad categories of valuation methods just described, there are a few steps that are usually required regardless of what type of approach you take. We outline these next.

Key Steps to Follow To Value an SME

As well as choosing the valuation method, there are some steps in valuing an SME that a valuation professional might take regardless of which valuation method they decide upon. These steps might look something like the following:

Gather Financial Information: Collect the company’s financial statements, tax records, cash flow statements, and any other relevant financial information. This will help you understand the company’s historical financial performance.

Understand the Industry: Research and gain a deep understanding of the industry in which the SME operates. Industry dynamics, trends, and growth prospects can impact the company’s valuation.

Choose a Valuation Method: There are several methods used to value SMEs, which we explore in more detail below.

Calculate Valuation: Apply the chosen valuation method to the normalized financial data. For example, in the income approach, calculate the present value of future cash flows, or in the market approach, compare the SME’s ratios to those of comparable companies.

What are the Key Valuation Methods Used for SMEs?

As touched upon above, there are three primary methodologies used to value SMEs: the Asset-based Approach, Income Approach, and Market Approach. These methods offer unique insights and serve different purposes.

- Income Approach: This method focuses on the future, seeking to determine the profit a company can generate moving forward. The most popular technique under this approach is the Discounted Cash Flow (DCF) analysis, which projects future cash flows and discounts them to their present value. This method can be compared to farming, where the worth is estimated based on potential future harvests.

- Market Approach: This approach embodies the principle that ‘something is worth what someone is willing to pay for it‘. It estimates a company’s value by comparing it to similar companies that have been sold in the market. Alongside the DCF described above, the Market Approach is a widely adopted approach used by valuation practitioners. When valuing SMEs one challenge with this approach can sometimes be finding comparable businesses due to the SMEs unique characteristics.

- Asset-based Approach: This method functions like an inventory check, summing up a company’s tangible and intangible assets and subtracting liabilities, resulting in the company’s net asset value. It’s akin to estimating a house’s value by calculating the cost of bricks, cement, paint, and then subtracting any existing mortgages or debts.

What Additional Factors are Considered in SME Valuation?

When it comes to SMEs, there are additional factors to consider:

- Owner Dependence: SMEs often heavily rely on their owners. Thus, assessing the impact of the owner’s departure on the business value is crucial.

- Client Concentration: If a significant portion of revenue is derived from a few clients, this introduces risk, which could decrease the company’s value.

- Market Position and Competitive Advantage: A strong market position or unique competitive advantage can increase an SME’s value.

- Quality of Financial Statements: High-quality, well-maintained financial records can increase confidence in an SME’s value.

A valuation professionals may well consider many more risk factors in addition to those above, when performing a thorough and carefully considered company valuation.

What is the Role of the Discounted Cash Flow (DCF) Method in SME Valuation?

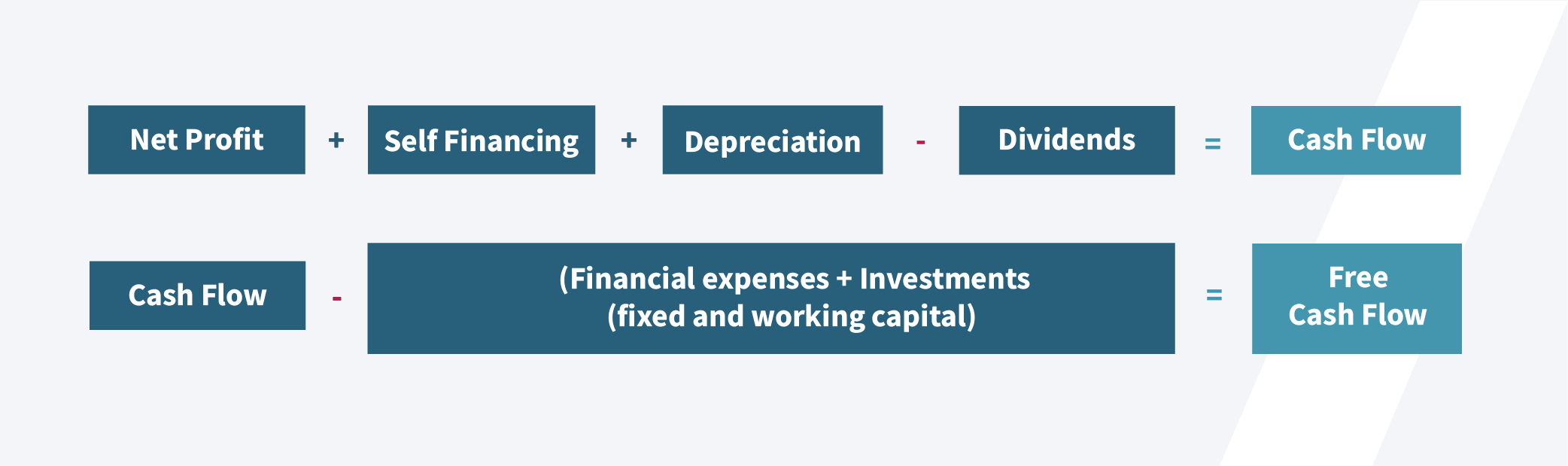

This method calculates the value of an SME based on its future cash flows, which are adjusted to account for the time value of money. To define both income and risk appropriately, we focus on Free Cash Flow (FCF) and the discount rate.

Free Cash Flow (FCF) is the liquidity available in the company that the owner can use without jeopardizing the company’s financial equilibrium. To calculate FCF, we follow these steps:

The discount rate integrates the risk and mirrors the opportunity cost of the operation. This rate is typically determined using the Capital Asset Pricing Model (CAPM) methodology.

The DCF valuation formula is as follows:

What difficulties arise when using the DCF method on SMEs?

While the DCF method is widely applicable, implementing it to value SMEs often presents some hurdles due to their unique characteristics. These challenges primarily lie in the following areas:

- Information availability: SMEs can lack historical financial information. When available, this data might have been prepared for legal obligations rather than economic analysis.

- Reliability of data: The information at hand might lack credibility due to the absence of external audits, which are typically not required for SMEs.

- Future projections: Financial forecasts are often inadequate, delayed, or even non-existent, making it tough to project future cash flows.

To counter these challenges, analysts must reconstruct past financial statements and make informed predictions about the future. This often involves separating personal and business assets, filtering personal expenses from company expenses, and distinguishing between company and owner investments.

The discount rate is another contentious area. It needs to incorporate both the project risk and the opportunity cost, typically done using the CAPM method. However, market information required for CAPM, such as beta coefficients and risk premiums, may not be available for SMEs. To solve this, approximations are used, and an illiquidity premium is added to the rate to account for the lack of market for SME shares.

Lastly, determining the continuity value (or terminal value) is a subjective process that often leads to disagreements. A common method is to use the company’s Price-to-Earnings Ratio (PER), but it can be challenging for SMEs due to the absence of a market. Therefore, negotiations often play a pivotal role in reaching a consensus.

Key Considerations

Valuing an SME isn’t about choosing one method over another. Instead, it’s about understanding the narrative each method tells about the business and blending these narratives to arrive at the most accurate depiction of the company’s worth.

While SME valuation might seem like a daunting task at first, breaking it down into understandable components makes it approachable. Whether you’re an entrepreneur preparing for the next funding round or a budding investor ready to dive into the dynamic SME market, we hope the above has opened a window into the intricate and important world of SME valuations.