On August 16, 2022, the Inflation Reduction Act was signed into law by President Biden. Included in this legislation is a section aimed at improving affordability and reducing premium costs of health insurance for consumers.

Within this provision, a refundable premium tax credit (PTC) is available on a sliding-scale basis for individuals and families who are enrolled in a qualified health plan purchased on the state or federal exchange Marketplace, and who aren’t eligible for other qualifying coverage or affordable employer-sponsored health insurance plans providing minimum value [IRC Sec. 36B(a)].

Background on the enhanced premium tax credit extension

When the Affordable Care Act (ACA) was signed into law back in 2010, it included enhanced PTCs to help individuals and families with incomes between 100% and 400% of the Federal Poverty Line (FPL) purchase health insurance on the Marketplace.

As part of the American Rescue Plan Act (ARPA) of 2021, the Biden administration’s first tax base bill, the premium tax credit was opened up to far more taxpayers via a temporary extension for individuals with incomes above 400% of the FPL and a more generous subsidy for those below 400%. For 2021 and 2022, ARPA also expanded the ACA requirement that a health plan premium not be more than 8.5% of an individual’s income to those with incomes above 400% of the FPL.

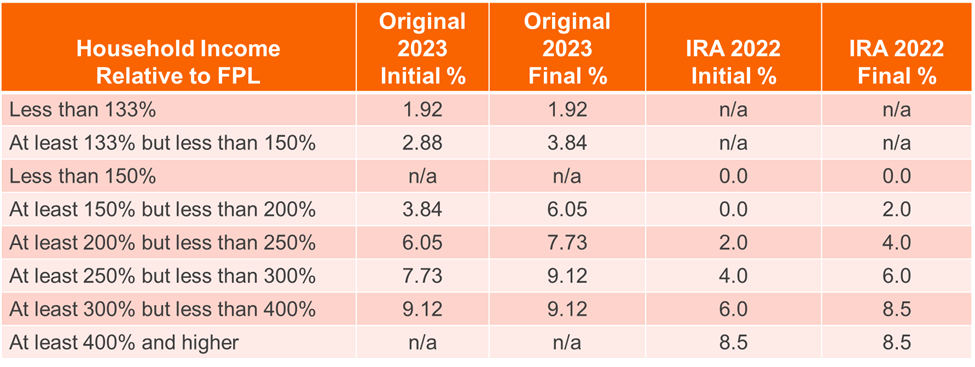

These tax credits were originally set to expire on January 1, 2023. The new provision within the Inflation Reduction Act extends them through 2025.

Explaining the enhanced PTC extension to clients

For taxpayers and their families who are enrolled in a qualified Marketplace health plan, the premium tax credit is limited to the excess of the premiums for the applicable second lowest cost silver plan (the applicable benchmark plan) over the taxpayer’s contribution amount (required share). The taxpayer’s required share equals the taxpayer’s household income multiplied by an applicable percentage for the tax year.

The applicable percentage for a tax year is based on the taxpayer’s income level relative to the FPL for the year. Within each income tier, a taxpayer’s applicable percentage increases in a linear manner from the initial to the final premium percentage [IRC Sec. 36B(b)(3)].

So, for more modest income taxpayers, once the percentage of household income applied towards their premium exceeds a certain percentage, the fully refundable PTC kicks in on the 1040 Schedule 3.

The temporary percentages that apply for 2021 through 2025 are detailed in the chart below.

Two big takeaways on the premium tax credit extension

There are two significant takeaways on this piece of the Inflation Reduction Act. First, taxpayers with household income under 400% of the FPL are going to have to spend less of their household income in 2021 through 2025 towards the cost of their qualified Marketplace health plan premium before the PTC kicks in.

Another aspect that so far has not received much attention is the fact that if a taxpayer’s income is above 400% of the FPL, they may now qualify for premium tax credits that lower their monthly premium for a Marketplace health insurance plan.

For example, let’s say a client is at 435% of the FPL. They’re going to take 8.5% of their household income and compare that to the cost of those Marketplace premiums. If the 8.5 garners them a credit, then for four years, they’re going to get it. Previously, they were not entitled to the PTC at all.

Learn more about the Inflation Reduction Act

For a more detailed analysis of recent IRS-related funding, join our CPE webinar Inflation Reduction Act of 2022: Key Federal Tax Provisions. This session will give you the information you need to summarize the new legislation’s tax developments affecting business and individual taxpayers and analyze how the developments affect your clients.