Print

PrintMichael Seigne is the Founder of Candor Partners Limited, and Joerg R. Osterrieder is Professor of Finance and Artificial Intelligence at the University of Twente. Related research from the Program on Corporate Governance includes Short-Termism and Capital Flows (discussed on the Forum here) by Jesse Fried and Charles C. Y. Wang; and Share Repurchases, Equity Issuances, and the Optimal Design of Executive Pay (discussed on the Forum here) by Jesse Fried.

In recent decades, share buybacks have emerged as a global corporate phenomenon, albeit one accompanied by escalating controversy. While companies put forth various reasons for pursuing share buybacks, it is the argument that frames them as an attractive alternative to dividends for returning capital to shareholders that generates the most contention. The flexibility for the company and potential tax advantages offered to investors in certain scenarios are among the touted benefits. In this article, we shed light on the potential pitfalls associated with the implementation of share buybacks, a topic that merits exploration in the realm of corporate governance.

Scale of Share Buybacks

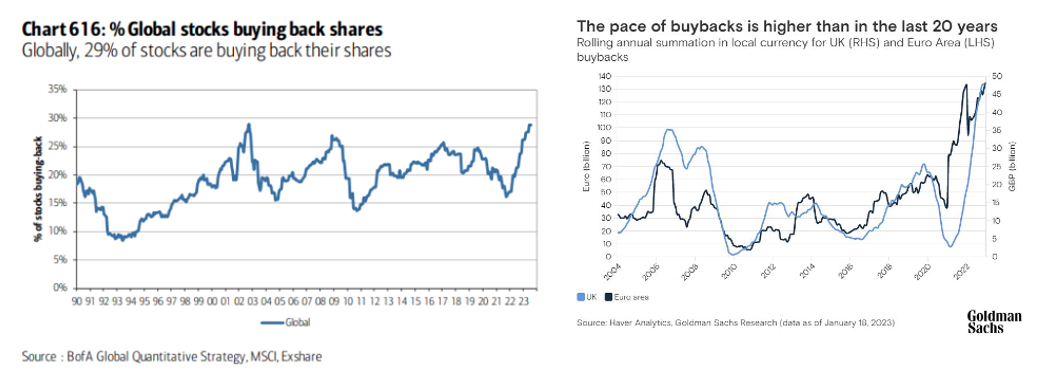

Over the last 5 years companies have bought back $5.6[1] trillion in the US, UK and Europe. Globally buybacks are getting increasingly popular, in ‘23 we are seeing a recent high of 29% of all listed companies buying back shares, especially in the UK, Europe and Japan.

Given the scale of buybacks, both in terms of value and popularity, if there are suggestions of Corporate Governance issues, then these deserve our attention.

Governance Overview

When contemplating a share buyback, the board and executive management bear a fiduciary responsibility to act in the best interests of the company and its shareholders. This duty explicitly extends to decisions regarding capital allocation and the choice to employ share buybacks as a means of returning cash to shareholders. One of the governance issues also relates to conflicts between the interests of different shareholder groups themselves. This conflict arises as it is widely accepted that executing a share buyback when the share price is overvalued results in value being transferred from long-term shareholders to those selling their shares. We will delve further into this valuation issue later in this article.

One argument in favour of more continuous share buybacks posits that investors desire management to prioritise the creation of long-term shareholder value through focusing on investing and growing the business and its strategy rather than trying to time share buybacks on a less regular basis. The logic behind this dividend-like use of share buybacks suggests that if investors believe the share price is inflated, they can opt to sell their proportionate increased ownership of the company’s shares into the share buyback, thereby crafting a “synthetic” dividend. The extension of this argument is that all investors should accept share buybacks at any valuation, rendering this debate seemingly resolved.

However, for a shareholder desiring to sell into the buyback, the mechanics of the share buyback process become crucial. A significant challenge arises because, to “harvest” this dividend, shareholders must possess sufficient information about the progress of the share buyback to calculate and sell the correct number of their own shares into the buyback. This raises pertinent questions: Do current market practices for share buybacks facilitate this? Are there implications for the corporate governance responsibilities of the board that relate to the mechanics of how a share buyback gets executed?

Imagine a shareholder who owns 1% of outstanding shares, and the company announces an intention to execute a share buyback with a value equivalent to 10% of outstanding shares. If the shareholder takes no action, their holding will increase to approximately 1.1% when the buyback concludes. For shareholders who prefer cash, they can sell the additional 0.1% ownership of shares. This means that as the buyback progresses, this shareholder will continuously own a 1% stake in the company while progressively selling the precise number of shares, thereby generating additional cash, hence the term “synthetic” dividend.

How does this work in practice?

Regulations dictate that a company must declare its intention to conduct a buyback before commencing the process, usually companies state this in terms of a monetary value. At this point, shareholders have no assurance that the company will indeed repurchase any shares, as it remains an intention. Furthermore, the company may have undisclosed specific conditions, such as share price caps that might affect the progress of the buyback. Shareholders also remain unaware of the number of shares the buyback might ultimately acquire, as this depends on the market prices at the time of purchase. Consequently, shareholders lack precise knowledge of the number of shares, if any, they should sell and when to sell to generate this “synthetic” dividend.

As the company progresses with its buyback, it must provide periodic disclosures to shareholders, with specific rules varying by jurisdiction. In the United States, for instance, these disclosures are now required on a quarterly basis. This means that shareholders can only calculate their increased ownership on a significant delay. These delays, while potentially frustrating for shareholders, are designed to safeguard their interests in various aspects of the execution process.

However, this delay introduces share price risk for the portion of shares representing the “synthetic” dividend for the investor. The key point here is that shareholders cannot sell to the company as it buys shares while simultaneously knowing the exact number of shares they should sell.

Most companies repurchase their shares using Open Market Repurchase (OMR) methods or similar processes that fall within safe harbour provisions, such as the 10b-18 rules in the United States. These provisions shield the company from liability under certain market manipulation rules. Nevertheless, these provisions, combined with some guaranteed buyback execution products, often lead the company and its brokers making all their purchases on the lit order books of public stock exchanges like the NYSE and Nasdaq, and none directly from shareholders.

Consequently, even if shareholders were aware of the precise number of shares they should sell, they would be unable to sell directly into the company’s buyback program. Furthermore, due to the delay in obtaining enough information to calculate the correct number of shares to sell, they potentially remain exposed to 3 months of share price risk. This may seem counterintuitive, as existing shareholders are already willingly exposed to this risk. However, the issue at hand is not trivial.

Consider how much the share price can fluctuate during that time frame. If a company experiences an annual share price volatility of 30%[2], it implies a 1 standard deviation move of +/- 15% over 3 months. In the UK and the EU, the time delay is less burdensome. UK shareholders receive relevant information with an overnight delay, while in the EU, it takes a week. For the same example, the equivalent 1 standard deviation share price move is approximately 2% for 1 day and 5% for a week. The crux of the matter is that this additional risk needs to be considered.

Governance and Safeguarding Shareholder Interests

How should a board approach its responsibility to shareholders when approving a share buyback in light of the intricacies surrounding both valuations and the mechanics of implementation?

Governance relating to rationale based on valuation

Firstly, if the board and management endorse the share buyback based on the premise that the share price is undervalued, several considerations must be accounted for. Arguably, none is more critical than imposing a share price cap or limit on the buyback. This suggestion arises because research indicates that there is a series of execution products used by companies to implement share buy-backs that are not share price constrained. One such set of products are Accelerated Share Repurchases (ASRs), which are guaranteed buyback products, and reportedly 68%[3] are purchased without a cap or collar on the share price. This structure means that the company will buy shares at any price regardless of share price fluctuations. In this scenario how does the governance process ensure that the company’s rationale for the buyback, rooted in a perceived undervaluation, remains intact across all share prices?

Governance relating to rationale not based on valuation

If the board simultaneously approves the buyback without expressing an opinion on valuation, should the board inform shareholders? We contend that it is sound governance to consider whether there exists a responsibility to apprise shareholders. This stance aligns with the widespread understanding, as mentioned at the article’s outset, that if a share buyback is executed when the share price is overvalued, value shifts from long-term shareholders to those selling their shares. Not all shareholders may possess views on the current share price versus valuation metrics, and they may expect the board to make this determination on their behalf. This expectation is not unreasonable, given that shareholders entrust the board with decision-making authority and conflict management in their long-term interests. If the board has not considered the potential value transfer in the event of an expensive purchase price, shareholders ought to be informed. This would empower shareholders to make their own evaluations. Anecdotal evidence suggests that such communication is rarely found in share buyback disclosures.

Governance relating to buyback progress update delays

How does the governance process assess the share price risk for shareholders seeking to “harvest” a dividend if the board’s rationale for the buyback revolves solely around returning excess capital? Does this evaluation include how this added risk is factored into the overall benefits for shareholders compared to dividend alternatives which involve riskless cash?

Lastly, does the governance process possess a comprehensive understanding of the mechanics underlying various share buyback implementation methods? Such understanding is crucial to enable shareholders willing to sell shares back to the company to do so effectively.

Conclusion

In our exploration of the intricate landscape of share buybacks and their implementation challenges, we have unveiled a complex terrain that demands thorough consideration within the realm of corporate governance. These governance topics are the source of increasing controversy, particularly when buybacks are positioned as the favoured alternative to dividends when returning capital to shareholders.

The fiduciary duty of boards and executive management to act in the best interests of the company and its shareholders is a foundational principle of corporate governance. Decisions surrounding capital allocation and the use of share buybacks as a means to return cash to shareholders hold significant importance in this context.

The argument in favour of ongoing share buybacks, designed to efficiently return excess capital rather than create long-term shareholder value, presents a distinctive perspective. It proposes that shareholders should have the option to participate in a “synthetic” dividend by selling their shares into the buyback when they perceive the share price as overvalued. However, achieving this pose significant challenges due to limited information available to shareholders about the buyback’s progress.

The regulatory framework surrounding share buybacks necessitates transparency but also introduces complexities. Shareholders must navigate uncertain intentions, undisclosed conditions, and varying disclosure rules across jurisdictions, all of which affect their ability to make informed decisions regarding the sale of shares into a buyback. Furthermore, the delay in information flow introduces share price risk, a consideration that cannot be overlooked.

Within the domain of governance, critical questions arise. When buybacks are approved based on the belief that share prices are undervalued, boards must consider mechanisms to ensure that this rationale remains consistent across various share price scenarios. Shareholders should be informed if the board approves buybacks without expressing an opinion on valuation, empowering them to evaluate potential value transfers.

Moreover, the governance process must address the share price risk faced by shareholders seeking to “harvest” a dividend through share buybacks, particularly when the buyback rationale revolves around returning excess capital. Balancing this risk against the perceived benefits of buybacks versus dividends becomes a paramount concern.

Ultimately, the governance process itself must possess a deep understanding of the mechanics behind various share buyback implementation methods. This understanding is crucial to empower shareholders willing to sell their shares back to the company effectively.

In conclusion, share buybacks remain a critical aspect of modern corporate finance, but their implementation complexities pose significant governance challenges. By addressing these challenges, boards and executive management can enhance transparency, protect shareholder interests, and ensure that share buybacks serve as a valuable tool for returning capital to investors while fostering long-term shareholder value.

Endnotes

1Yardeni and Goldman Sachs(go back)

2At the time that the data was sourced for this article the median 90 day volatility of stocks in both the S&P 500 and EuroStoxx 600 was around 30%. Not to be confused with the VIX and V2X which at the time were in the mid to high teens.(go back)

3Chen, Kai, Press release management around accelerated share repurchases (April 7, 2020). European Accounting Review (2021) 30(1): 197–222, Available at SSRN: https://ssrn.com/abstract=3572543(go back)