Sky Blog

Sky Blog

Financial disclosure is critical for the efficient allocation and reallocation of capital. However, the debate on the costs and benefits of disclosure mandates is unresolved, and the empirical evidence is mixed. In a new paper, we contribute to this debate by investigating the role of disclosure mandates in the takeover market for banks.

Mergers and acquisitions are essential means of capital reallocation, helping to direct assets towards their best use by reallocating control rights over companies. In 2021 alone, the announced global M&A transaction volume exceeded $5 trillion. Financial disclosures play a critical role in M&A, allowing acquirers to evaluate alternative investment opportunities. Acquirers conduct extensive comparative analyses using public financial disclosures to identify and value potential targets. Disclosure mandates can facilitate M&A by providing acquirers with richer and more precise information about potential targets and thereby improving the acquirers’ estimate of the targets’ intrinsic value and expected synergies.

Yet enhanced mandatory disclosure can also prompt acquirers to cut back on acquiring costly private information and reduce their incentives to discover proprietary information about potential targets. Acquirers may engage in less information discovery about alternate uses of the targets’ resources and, as a result, make fewer takeover bids. Thus, the impact of disclosure mandates on M&A activity is unclear.

We investigate the impact of mandatory financial disclosure on the takeover activity of privately held U.S. bank holding companies (BHCs), focusing on a regulatory reporting change that raised the asset-size threshold for reporting quarterly consolidated financial information. To ease the regulatory reporting burden on relatively small BHCs, effective March 2015, the Federal Reserve Board (FRB) eliminated quarterly consolidated financial reporting requirements (FR Y-9C reports) for BHCs with less than $1 billion in total consolidated assets. Instead, these BHCs, with few exceptions, were required to file semiannual parent-only financial statements (FR Y-9SP reports). Previously, only BHCs with less than $500 million in total consolidated assets were qualified to file the FR Y-9SP reports.

In general, banks are among the most opaque corporate entities. Privately held banks, though, are especially opaque. They are not registered with the SEC and so not subject to quarterly financial reporting requirements. Moreover, few, if any, information intermediaries (e.g., analysts, credit rating agencies, etc.) generate information or reports on private banks. Therefore, regulatory financial filings are the primary source of publicly available information for privately held banks.

The 2015 regulatory disclosure mandate further reduced the frequency of small BHCs’ regulatory filings and required the reporting of less-detailed information. For instance, in March 2015, the FR Y-9C report included 22 more schedules than the FR Y-9SP report. One can also discern how much more information is in the FR Y-9C report than in the FR Y-9SP report from their lengths—a typical FR Y-9C report has 65 pages, while an FR Y-9SP report has eight pages.

Federally supervised commercial banks must also file Call Reports quarterly. The Call Reports are bank-level financial statement-based reports containing information similar to that of the holding company-level FR Y-9C reports. However, significant information critical for assessing the risk and overall profitability of a bank available in the FR Y-9C reports is missing from the Call Reports. For instance, the Call Reports lack information about (1) intracompany transactions, (2) nonbank subsidiaries, (3) interest-rate sensitivity, (4) insurance-related underwriting activities, and (5) financial statement effects of acquisitions during the quarter.

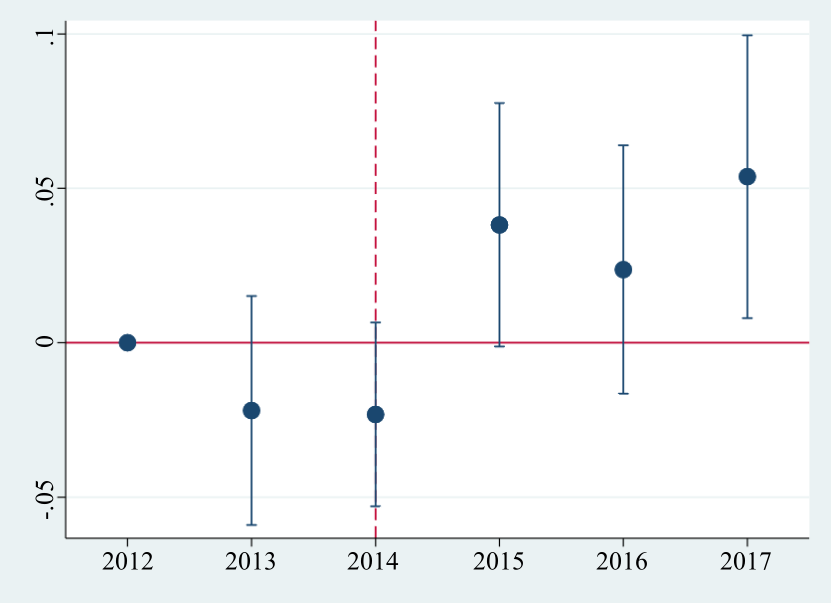

In our study, we use a difference-in-differences research design and find that BHCs with total consolidated assets of $1 billion or more are more likely to receive acquisition bids than BHCs with less than $1 billion of total consolidated assets after the March 2015 disclosure mandate. The graph below shows how the likelihood of BHCs being targeted for a takeover changes as a result of the March 2015 regulatory disclosure change. Specifically, after March 2015, a BHC with total consolidated assets of $1 billion or more was 2.3 percent more likely to be an M&A target than was a BHC with total consolidated assets of less than $1 billion. For comparison, the unconditional probability of receiving an acquisition bid in our sample is 3.2 percent.

Furthermore, the impact of the disclosure mandate is more severe for BHCs that suffer a more significant loss in publicly available information. We find that BHCs with total consolidated assets of $1 billion or more with nonbank activities are more likely to be targets than other BHCs with nonbank activities after March 2015.

We also show that acquirers earn relatively higher bid-announcement returns when targeting BHCs with more detailed and frequent mandatory disclosure. These results suggest that the availability of public information about BHCs decreases both the acquirers’ search costs and the uncertainty regarding potential value creation through M&A. Finally, we find that the time to complete the acquisition following identification of a target does not differ significantly between banks above and below the $1 billion asset-size threshold. This finding is consistent with acquirers having access to private information about targets following the signing of confidentiality agreements or letters of intent, which reduces their reliance on public financial information.

Overall, our findings suggest that, while small BHCs may benefit from the reduction in reporting and proprietary costs associated with reduced mandatory financial disclosure, they bear the cost of less interest from potential acquirers. To market themselves as a target, small BHCs now need to incur additional costs and may not be able to reach all potential buyers.

Our study makes several contributions. First, we show the direct impact of mandatory financial disclosure on the takeover market. Financial disclosures are a crucial source of information in acquirers’ search for targets with higher synergies and can facilitate more accurate estimates of targets’ intrinsic value and expected synergies. Yet, the implications of mandating financial disclosures in the takeover market have received scant attention.

Second, our findings should interest bank regulators as they implement and evaluate asset size-based mandatory disclosure regulations. Small BHCs are exempted from filing the more detailed FR Y-9C reports quarterly to reduce their regulatory burden. We document an unintended consequence of this regulation: a reduction in the liquidity and market discipline of small BHCs because of a decrease in the likelihood of small BHCs being targets of acquisitions.

On July 9, 2021, President Joseph Biden signed an executive order calling for greater scrutiny of bank mergers to promote competition in financial services.[1] Our findings suggest that bank regulators should consider the impact of bright-line asset threshold-based disclosure mandates on M&A activity and competition in the banking industry.

ENDNOTE

[1] https://www.whitehouse.gov/briefing-room/presidential-actions/2021/07/09/executive-order-on-promoting-competition-in-the-american-economy/

This post comes to us from professors Urooj Khan at the University of Texas at Austin’s McCombs School of Business, Doron Nissim at Columbia Business School, and Jing Wen at the City University of Hong Kong’s College of Business, It is based on their recent paper, “Mandatory Disclosure and Takeovers: Evidence from Private Banks,” available here.