Click to Download: How to Avoid Chapter 22 in Restructuring Work for Energy Companies

Executive Summary

Issue

It takes time and money to go through a Chapter 11 restructuring, so going through it twice in a couple of years is unwise and inefficient. Recently, it has been an issue with companies operating in the energy complex. The challenges and complexities of energy markets make reorganization plans hard to properly formulate.

Challenge

The challenge for counsel and financial advisors has to with the often-severe price volatility common to oil and gas markets. Restructuring practitioners are usually generalists, and often do not understand commodity markets or their impact on cash flow and debt capacity well enough to make plans feasible.

Solution

Generalists will make mistakes. The solution calls for advisors who have deep and broad energy complex expertise. Regardless of “customary” practices, using simple deterministic models is a poor idea. The cash flow analysis that is done to support the feasibility of a plan of reorganization should not be deterministic. Rather, it should be probabilistic, or stochastic. Decisionmakers, including the courts, should be provided with a stress-tested model.

“Chapter 22” is not a technical legal term. And it is not really a new term. In fact, there was a roundtable at the Harvard Law School in 20141 that focused on this very thing. Chapter 22 refers to a situation in which a company that had gone through a Chapter 11 filing, and emerged, has gone back into Chapter 11 again in short order. What are the causes? The Harvard Law School panel featured some of the nation’s finest bankruptcy attorneys. Harvey Miller, of Weil, Gotshal & Manges, said that increased “recidivism” in Chapter 11 filings was mainly due to distressed debt and securities investors, who effectively gained control of the debtor and its plan formulation process. This means they do all that they can to get the plan of reorganization confirmed. Sometimes the plan’s actually feasibility is not well scrubbed.2 Marshall Huebner, of Davis Polk & Wardwell LLP, pointed to other factors that can cause a subsequent Chapter 11 filing, such as the underestimation of an industry’s more permanent decline, or creditor pressure on the debtor to keep too much debt.3 Mark Roe, a professor at Harvard Law School, articulated that Chapter 22 filings are not that common, and represent less than 20% of Chapter 11 debtors. He also suggested that it might not be a poor trade-off, if most of the firms that file again do well.4 We are not as sanguine. Why not do it right once? And for companies that operate in the Energy Complex, doing it right the first time means you need to pay attention to the fundamental drivers of commodity price volatility.

What Does the Law Say?

In looking in the U.S. Bankruptcy Code, Section 1129(a)(11) provides, “The court shall confirm a plan only if all of the following requirements are met: Confirmation of the plan is not likely to be followed by the liquidation, or the need for further financial reorganization, of the debtor or any successor to the debtor under the plan, unless such liquidation or reorganization is proposed in the plan.”5 So how does Chapter 22 happen? In the context of energy companies, it happens when the debt load post-restructuring is based on wishful thinking as to how oil and natural gas prices will behave in the months and years after emergence. Very few workout practitioners run detailed analysis of pricing trends and the actual debt capacity of the restructured firm if and when commodity prices fall.

Why is Energy Different?

Commodities, including oil and gas, are far more volatile than other asset classes like fixed-income and equities. We have discussed this in a separate article recently published on our site.6 WTI oil has an average annual volatility of more than 40%, and the NYMEX Henry Hub natural gas contract is even higher.

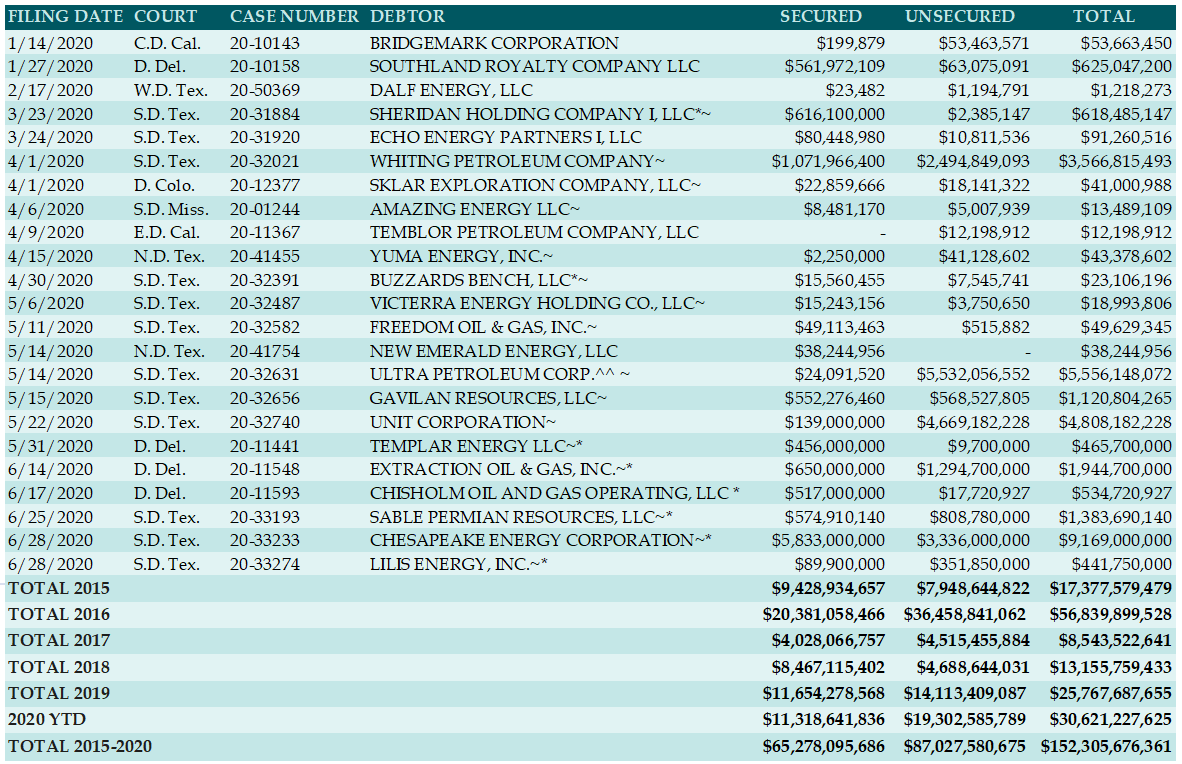

This chart, below, was prepared by the Texas law firm Haynes Boone,7 which has been doing outstanding work in recent years tracking oil patch bankruptcies. Note that Ultra Petroleum is listed. Ultra Petroleum filed for bankruptcy back in May of 2016, so this is its second filing in four years. It came out of Chapter 11 in 2017 with nearly $3 billion in new debt. We wonder what natural gas price assumptions were used at that time when the plan was approved. Energy commodities usually do not follow lognormal random walks and should be modeled via simulation. The processes they follow have similarities to ARMA–GARCH models. The reason for this is that oil and gas prices move with the volatility of their physical and financial markets, as well as complex density functions of future prices that incorporate price jumps or “shocks.”8

Simulation Models

Attorneys, and judges, often call simulation models “speculative.” Given the anniversary that just happened, of the atomic bombings of Hiroshima and Nagasaki, it is well worth noting that Monte Carlo Simulation was used at Los Alamos, New Mexico as part of the Manhattan Project. Arguably, its modern form using randomness with discipline and rigor, in computational analysis, was developed there. There was no other way for the experts at Los Alamos to estimate how far a neutron will go before it hits something that will cause energy to be released. There is nothing speculative about this technique. It was a tested mathematical process used then, to model fast neutron chain reactions. And it is especially common now in the energy, economics, physics, and pharmaceutical professions.

The term “stochastic” has its roots in the Greek word στόχος, which can be “stókhos” or “stóchastikos” in English.9 One definition of the word is “to guess,” which is why some lawyers think it is speculative. However, it also means “to aim or target.” This is how we use it in finance, economics, etc. The modeling that is done as part of any restructuring process, and reorganization plan, should consider more sophisticated approaches. In our view, practitioners need to:

- Take the 13 week rolling cash flow model used during the workout process and expand it to five years.

- Use sensible input assumptions, especially with distributions and probabilities that are based on reality.

- Run commodity prices that consider mean reversion and actual volatility assumptions, not wishful thinking

- Stress test the forward-looking cash flows and debt capacity; and make them as sober as possible.

The cash flows we isolate are tested for their ability to support debt, the new capital structure of the restructured firm. The critical inputs, especially commodity prices, can be matched to levels of debt that can be supported given the range of potential outcomes. This type of modelling allows for price jumps or shocks to be tested carefully as well. It is important to note that we do not use this technique to reach one specific answer. Probabilistic modelling provides real decision makers with a range in which they can negotiate and design a better capital structure for the most likely economic forecast.

Conclusion

There is no reason for any energy company to go through a “Chapter 22” process. The tools, techniques, experience, and data are all available such that any plan of reorganization can be constructed to model risk adjusted cash flows. Lawyers, the Courts, and financial participants will develop more comfort with simulation techniques the more they are used by advisory practitioners. The results for the various stakeholders will be far improved.

ValueScope: Measuring, Defending and Creating Value for Our Clients

ValueScope is a leader in the application of fair value measurement applying the Mandatory Performance Framework for better compliance with the Public Company Accounting Oversight Board.

Sources:

[1] https://blogs.harvard.edu/bankruptcyroundtable/tag/chapter-22/, Stephanie Massman (J.D. 2015).

[2] Ibid.

[3] Ibid.

[4] Ibid.

[5] 11 U.S.C. §1129(a)(11)

[6] “ESG-A Valuation Framework”

[7] HAYNES AND BOONE, LLP OIL PATCH BANKRUPTCY MONITOR, June 30, 2020, www.haynesboone.com

[8] “Oil prices — Brownian motion or mean reversion? A study using a one year ahead density forecast criterion,” Nigel Meade, Energy Economics, Energy Economics, Volume 32, Issue 6, November 2010, Pages 1485-1498.

[8] https://www.merriam-webster.com/dictionary/stochastic

For more information, contact:

Thomas J. McNulty CQF, FRM, MBA

PRINCIPAL AND MANAGING DIRECTOR, HOUSTON

The information presented here is not nor should it be treated as investment, financial, or tax advice and is not intended to be used to make investment decisions.

If you liked this blog you may enjoy reading some of our other blogs here.