Print

Print![]() In June 2025, I participated in a panel hosted by the U.S. Securities and Exchange Commission’s Investor Advisory Committee to discuss the growing momentum behind pass-through voting and what it means for investor empowerment.

In June 2025, I participated in a panel hosted by the U.S. Securities and Exchange Commission’s Investor Advisory Committee to discuss the growing momentum behind pass-through voting and what it means for investor empowerment.

The conversation brought together experts from across the governance ecosystem, including Vanguard, EQ Shareowner Services, the Society for Corporate Governance, and a renowned academic from the University of Pennsylvania. Each of us explored how the proxy voting system is evolving, and why giving clients a direct say in corporate governance is no longer a fringe idea, but a fiduciary necessity.

Why investor choice matters

More than 50% of U.S. households own pooled investment vehicles — mutual funds, ETFs, or closed-end funds.(1) That’s around 74 million households or approximately 130 million individual investors.

If we believe corporate governance plays a critical role in how companies operate today, then we must also believe that clients should have a say in how that governance is executed.

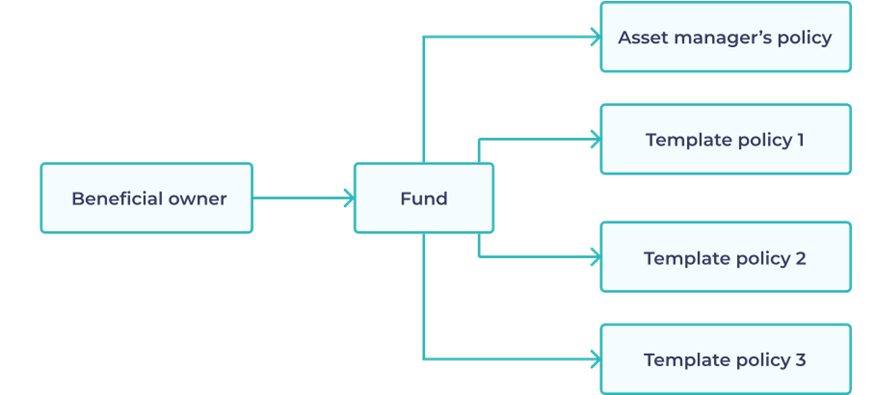

The current state of proxy voting

Traditional flow:![]()

Today, the typical process looks like this:

- A beneficial owner invests in a fund.

- That fund votes on behalf of all its clients.

- The asset manager makes voting decisions according to its own policy.

This creates significant issues:

- It’s hard for investors to understand how their shares will be voted.

- It’s hard to discover how the shares were voted after the fact.

What pass-through voting changes

Pass-through voting introduces choice at the point of proxy decision-making.

We move from:

Client ➝ Fund ➝ Fund votes on behalf of client

To:

Client ➝ Fund ➝ Client chooses how their shares are voted

At Tumelo, as a technology provider, we’ve seen several implementation models tailored to different types of clients:

- Policy selection:

Clients choose from a menu of voting policies, including the fund manager’s default.

Example: Vanguard’s approach. - Custom-policy creation:

Clients build their own proxy-voting policies based on personal or organisational principles. - Proposal-by-proposal voting:

Typically used by institutional clients who want to vote on specific ballot items they care most about.

The principle is straightforward: It’s the client’s money, therefore it is the client’s choice.

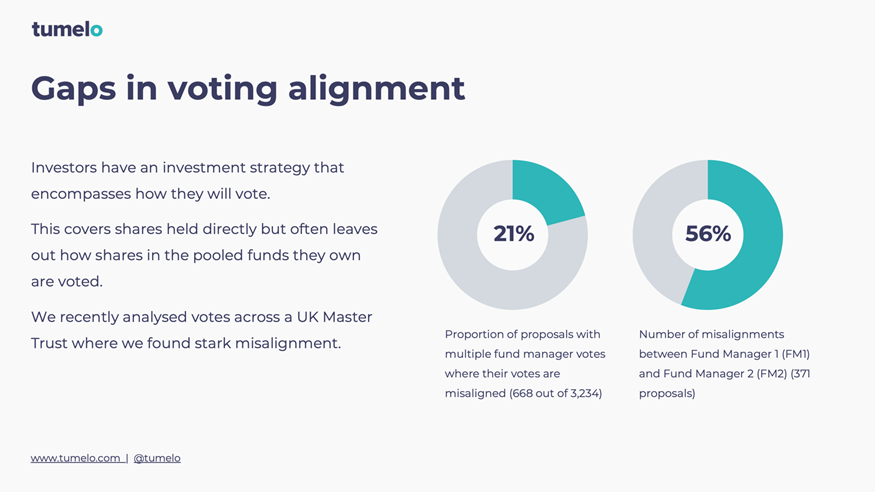

Solving real problems for institutional clients

From an institutional perspective, we’ve observed significant misalignment between an asset owner’s investment strategy and how its votes are cast in the pooled funds they use.

To address this, Tumelo offers a reporting solution that allows clients to compare:

- How shares held in separately managed accounts (which they vote themselves) are voted

- Versus how the pooled funds they use are voted (under the manager’s policy)

This often reveals discrepancies, which dilutes the impact of the client’s investment strategy.

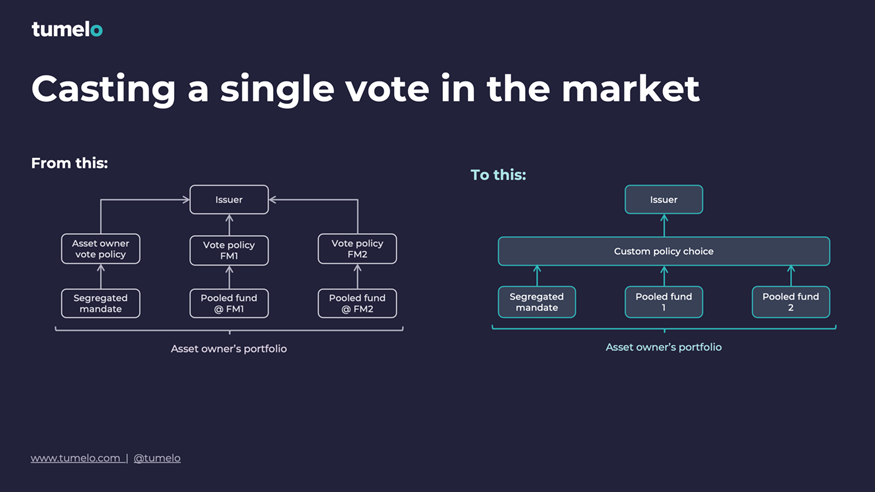

Enabling policy alignment across all assets

Pass-through voting solves this misalignment for asset owners.

Consider this simplified comparison:

- Before: An asset owner has a separate account (voted with their own policy) and several pooled funds (voted by fund managers).

- After: With pass-through voting, the client’s preferred policy can apply to all holdings —including pooled funds.

This alignment is essential. Without it, the client’s influence in corporate governance is fragmented, undermining their ability to act on their investment principles.

Customisation in practice

We’ve seen broad customisation among institutional and retail clients that have adopted pass-through voting. Examples include:

- Wealth managers seeking alignment across pooled funds used in client portfolios.

- Local Government Pension Schemes (LGPS) in the UK such as LGPS Central, which votes over £12 billion under a unified policy

- Defined Benefit (DB) and Defined Contribution (DC) Corporate Pension Schemes

which often take an issuer-focused approach, selecting target companies based on size or strategic priority. - Retail investors making a voting policy choice at the point of fund purchase.

Technology-enabled experiences

For institutional investors:

Tumelo offers a stewardship platform that enables:

- Policy selection.

- Visibility of upcoming votes.

- Direct vote casting.

- Full reporting for internal and external disclosures.

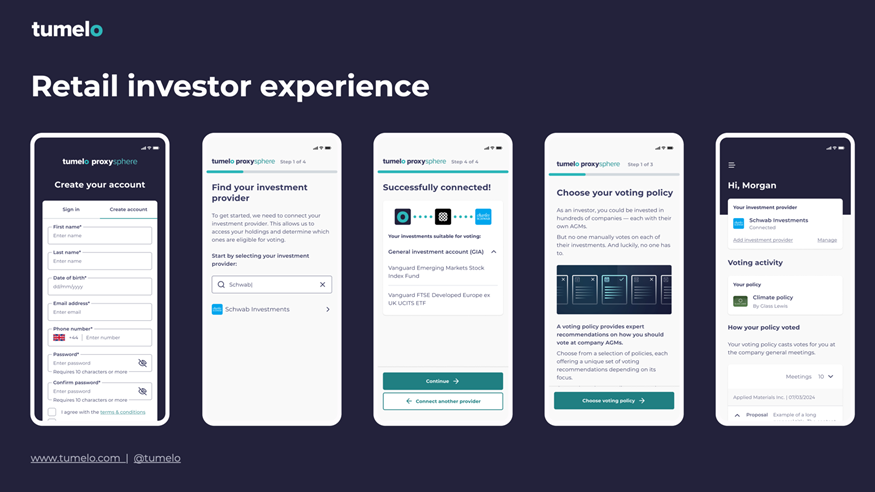

For retail investors:

The focus is on transparency and education. The experience includes:

- Connecting brokerage accounts.

- Viewing how shares are voted under the selected policy.

- Holding policy providers accountable for how votes are actually cast.

Growth of pass-through voting

We’re seeing strong and accelerating demand across the market:

- We support multiple fund managers.

- Over £200 billion in client assets currently vote through our platform.

- An additional £30 billion is in onboarding.

- We’ve identified over £1 trillion in institutional assets interested in adopting pass-through voting, but unable to access it — often because their fund managers do not yet support the functionality.

Importantly, demand is not limited to passive funds. Clients expect voting alignment across both passive and active portfolios.

Looking ahead

We believe pass-through voting will become a standard feature across all pooled investment vehicles. Why? Because clients want customisation, they believe voting control strengthens their investment strategy, and for many, it’s now considered table stakes.

We envision a future where investors buying a fund through a brokerage platform are immediately offered the chance to choose how their shares are voted all from within the same user interface.

References:

1. Investment Company Institute. (2023, October). Ownership of mutual funds, shareholder sentiment, and use of professional financial advisers, 2023 (ICI Research Perspective, Vol. 29, No. 10). https://www.ici.org/system/files/2023-10/per29-10.pdf